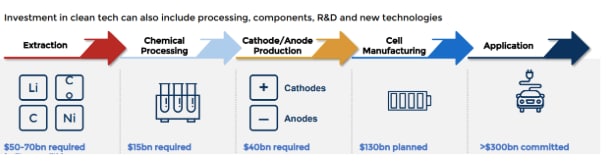

In the last five years, many national strategy or industry policy documents have mentioned Lithium-ion batteries across the world. Despite its newfound stardom, most countries seldom plan for the most strategic part of the Li-ion value chain: the midstream.China enjoys a near-monopoly in this midstream, despite having few mining reserves. Without midstream development, battery mineral-rich regions such as Australia and Latin American countries exercise little to no control over the strategic Li-ion value chain.The lithium-ion battery will go down in history as one of the most important platform technologies of our century. Platform technologies are not like others. They are the technologies that result from decades of innovation, that build entire industries, that secure a country’s long-term geopolitical advantage, that further national security, and those that create large economic value multipliers and localise critical future skills and jobs.One platform technology sector that is being transformed by incorporating all the elements we just mentioned is the automotive industry. Mobility will drive the global battery demand with its sheer size, dwarfing other demand applications. It is already well known that battery is the most valuable part of an e-vehicle, often differentiating the frontrunners from the rest. Most national plans rightly focus on the battery cell giga-factories to anchor the battery and the e-mobility industry.However, these giga-factories will not be competitive in a thoroughly globalised battery value-chain, without a core midstream industry (chemical processing and cathode/anode manufacturing) being built gradually around the battery cell giga-factories. This is a classic case of chicken-egg problem, where the midstream needing the assured demand of giga-factories and the giga-factories needing the closely located midstream to optimise costs in a low margin business. This is where the ‘state’ should step in with its clear policies and ambitious interventions.![screenshot-2020-11-13-at-7-32-14-pm]() Source: Benchmark Mineral IntelligenceIt can be seen from the above figure, that just core-battery midstream (cathodes and anodes) requires almost third of the battery cell giga-factory investment and will create enormous economic value.Another focus area should be ancillaries: The copper and aluminium current collectors, the polymer separators, and even the aluminium casings (or coated polymer pouches). These might look like minor components of the ecosystem, but on close examination, a standard Li-ion NMC622 cell will require around 700 tonnes of battery-grade copper and 300 tons of battery-grade aluminium current collectors, as opposed to 80 tonnes of Lithium. The polymer separators are often the second most expensive component of a battery cell after the cathodes. The ancillaries and midstream processing will together add as much value and certainly more jobs than the highly automated cell giga-factories.Way forwardIt is neither possible nor feasible for any country to house every single part of the Li-ion value chain. But it is essential to gradually build and grow the ancillaries and midstream industry wherever possible.For building a globally competitive midstream and ancillary industry, the following must be done:

Source: Benchmark Mineral IntelligenceIt can be seen from the above figure, that just core-battery midstream (cathodes and anodes) requires almost third of the battery cell giga-factory investment and will create enormous economic value.Another focus area should be ancillaries: The copper and aluminium current collectors, the polymer separators, and even the aluminium casings (or coated polymer pouches). These might look like minor components of the ecosystem, but on close examination, a standard Li-ion NMC622 cell will require around 700 tonnes of battery-grade copper and 300 tons of battery-grade aluminium current collectors, as opposed to 80 tonnes of Lithium. The polymer separators are often the second most expensive component of a battery cell after the cathodes. The ancillaries and midstream processing will together add as much value and certainly more jobs than the highly automated cell giga-factories.Way forwardIt is neither possible nor feasible for any country to house every single part of the Li-ion value chain. But it is essential to gradually build and grow the ancillaries and midstream industry wherever possible.For building a globally competitive midstream and ancillary industry, the following must be done:

- Enabling environment: Friendlier equipment and raw material import regime, tax holidays, affordable finance, and including battery ancillary products as part of EV supply chain to avail the proposed benefits to the EV ecosystem.

- Global partnerships: With the under-currents of trade wars, the Indian midstream and ancillaries industry can be a key strategic and commercial solution for the much-talked-about supply chain resilience of allies, and will provide complimentary scales to India.

- Capacity building: Indians working anywhere in the world who have built-up unique skills in the sector should be attracted via explicit campaigns, not only to build and run giga-factories but also to mentor the next generation of specialists. Efforts to build the sectoral understanding among the states, the central departments, and financial institutions will be key in understanding risks and set smarter regional agendas.

All three are interconnected. All three are necessary. All three result in an important capitalistic outcome: Incentivising the private sector to innovate, commercialise and lead.With no significant Li-ion battery capacity in the country, it might seem premature to talk about the midstream of a non-existent industry. But, due to the unique nature of the industry and extraordinary passion for the sector in the country, it is important understand the strategic value of different segments of the value chain to build the right ecosystem and invest or incentivise accordingly. Battery midstream is not only a supply chain but also a national capability. Even with new technology disruptions, by then, the midstream will have the skills and expertise to adapt. Li-ion midstream will mark the beginning of the precision engineering ecosystem and when fully built, this industry will position India to move higher and higher up in the mineral-heavy clean-tech value chain.

About the authors: Kowthamraj VS is a young professional at NITI Aayog; Vivas Kumar is principal at Benchmark Mineral Intelligence (formerly Tesla)