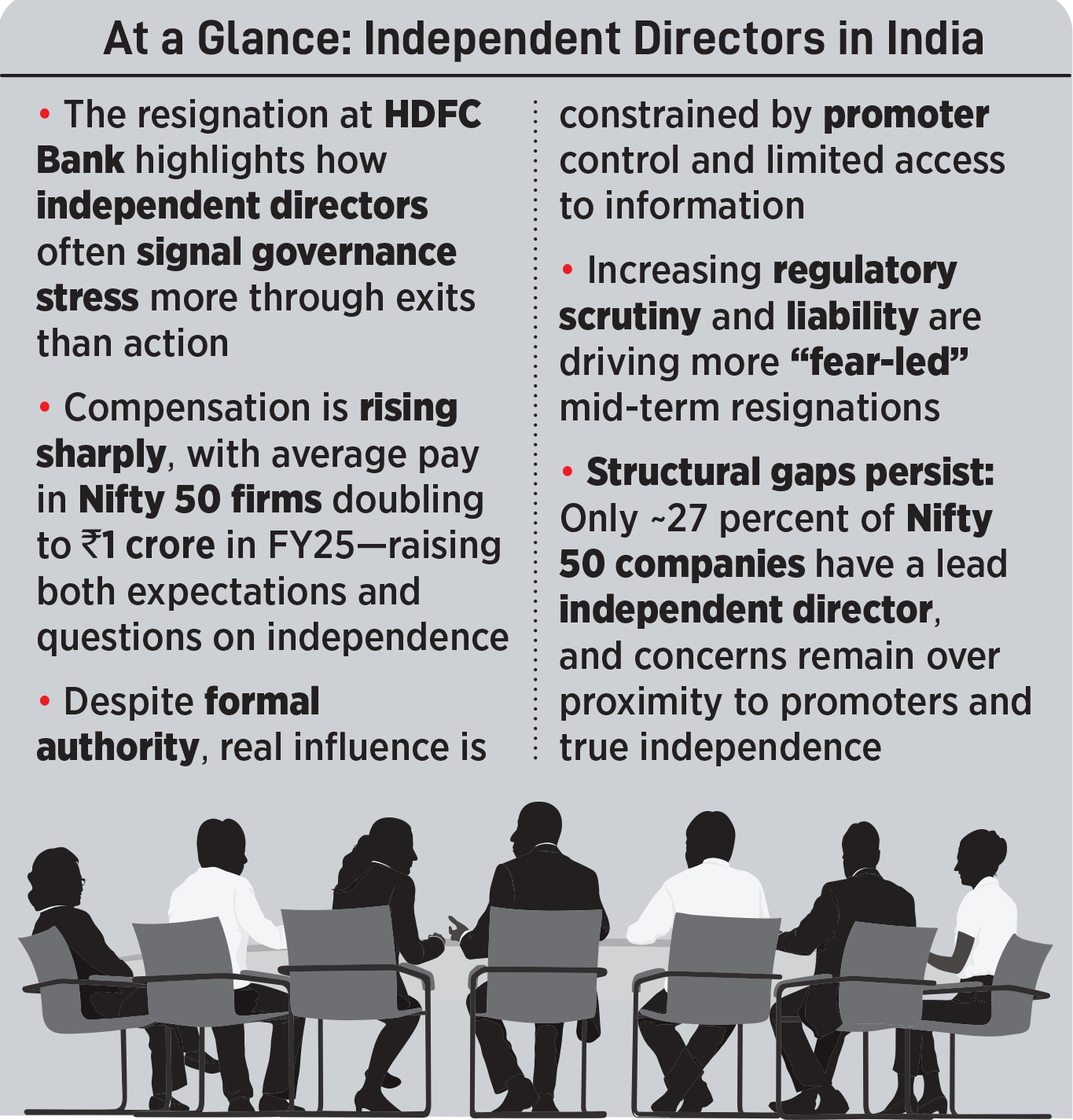

The resignation of Atanu Chakraborty as part-time chairman and independent director of HDFC Bank in March has done more than unsettle investors in India’s most valuable lender. It has reopened a persistent question in corporate India: What exactly is the power and the remit of an independent director?

Chakraborty, a former finance secretary, did not exit quietly. His reference to differences over “values and ethics” followed by comments hinting at deeper governance concerns ensured the resignation was read as a signal rather than an event. Markets reacted, regulators took note and boardroom dynamics usually shielded from public view came into sharp focus.

That, in many ways, is the paradox of independent directors in India. Their presence is meant to reassure investors that governance is robust. Yet, it is often their exit that reveals the fault lines. And increasingly, it is a role that is both more visible and more lucrative than before.

Independent directors were strengthened in India’s corporate framework in the aftermath of early-2000s governance failures. The idea was straightforward: Bring in credible outsiders who could challenge management, protect minority shareholders and ensure that boards did not become extensions of promoter interests.

Today, they occupy critical positions across audit, risk and remuneration committees. On paper, their mandate is expansive—they can question strategy, demand disclosures and even record dissent. In sectors like banking, their role is even more consequential, given the systemic risks involved.

But influence in the boardroom is rarely about formal authority alone. Independent directors operate in an ecosystem where information flows are controlled by management, and where promoters, despite regulatory safeguards, often retain decisive influence. The result is a delicate balancing act: Push too hard and risk isolation; stay silent, and risk irrelevance.

“One has to ask two questions—do promoters want independent directors and are they willing to give them access to information?” says Nitin Potdar, an independent counsel and former partner at J Sagar Associates. “If the answer to these questions is yes, then one has to see whether they have the time and capability to scrutinise the information.”

What has changed, however, is the economic value attached to the role. According to a study by Deloitte India, the average remuneration for independent directors at Nifty 50 companies has nearly doubled—from about Rs52 lakh in FY20 to roughly Rs1 crore in FY25. This sharp rise reflects not just higher profitability at large companies, but also the growing expectations and liabilities associated with board oversight.

There are also early signs of structural evolution within boards. Around 27 percent of Nifty 50 companies now have a designated lead independent director, a role intended to strengthen the voice of non-executive oversight, especially in situations where the chairperson is not fully independent. While still not widespread, the trend points to a gradual institutionalisation of independent authority within Indian boardrooms.

![]()

When exits become signals

Chakraborty’s departure fits into a broader, if understated, pattern. Over the past decade, several independent directors across Indian companies have stepped down mid-tenure. The stated reasons are usually anodyne—“personal commitments” or “other engagements”, but market participants have learnt to read between the lines. This is similar to the 2018-19 period that witnessed a slew of auditor resignations.

In some cases, these exits have preceded regulatory scrutiny or financial stress. In others, they have pointed to disagreements over governance practices, including related-party transactions, accounting treatments or risk management lapses. Even in high-growth new-age companies, where governance frameworks are still evolving, independent directors have occasionally found themselves at odds with founders over the pace and direction of expansion.

“Stricter enforcement has made independent directors liable for corporate governance failures. This has triggered fear-driven mid-term exits, as the role demands far more time and carries significantly greater pressure. Independent directors are under greater scrutiny from regulators, investors, and stakeholders alike, and the expectation to deliver has never been higher,” says Pranav Haldea, managing director at Prime Database.

What makes these resignations significant is not just their frequency, but also their opacity. Disclosure norms require directors to state reasons for stepping down, but the language often remains guarded. Legal risks, confidentiality obligations and reputational considerations all play a role in limiting what can be said.

The result is a curious equilibrium. Investors treat such exits as red flags, regulators sometimes initiate probes, but the underlying issues are rarely fully articulated in the public domain. Governance, in effect, is signalled but not explained.

The credibility question

For regulators like the Securities and Exchange Board of India (Sebi), this presents a continuing challenge. Over the years, Sebi has tightened norms around independence, tenure and disclosure. It has also pushed for greater accountability, making independent directors more answerable for lapses in oversight.

These moves have strengthened the framework, but also raised the stakes for those taking on such roles. The liability associated with board positions has increased, even as the ability to influence outcomes remains uneven. For many professionals, the risk-reward equation of being an independent director is no longer straightforward—even with compensation rising.

At the same time, expectations from the role have expanded. Independent directors are now expected to bring not just oversight, but also insight—on strategy, technology, capital allocation and ESG risks. In a market where companies are scaling rapidly and capital flows are increasingly global, the boardroom is no longer a ceremonial space.

“In my view, the very institution of independent directors needs to be re-examined. In most companies, independent directors are often friends or close acquaintances of promoters, making it unlikely they will raise red flags on governance issues. Compounding this is the fact that several of them are remunerated extremely well, leading to a conflict of interest,” adds Haldea.

This is where the credibility of the institution is tested. Independence cannot be reduced to regulatory compliance; it has to be reflected in behaviour. Are directors willing to ask uncomfortable questions? Do they have access to independent sources of information? Can they influence outcomes, rather than merely record objections?

“Their role also needs to be debated. In my view, their role should be limited to only look after interests of minority shareholders. Expertise such as ESG, cybersecurity etc can always be hired,” Haldea says.

The Chakraborty episode underscores both the progress and the limitations of India’s governance framework. That his resignation triggered debate is, in itself, a sign that independent directors matter. But the lack of clarity around the issues he flagged also highlights how much remains opaque.

For India Inc, the message is becoming harder to ignore. Independent directors cannot be treated as reputational capital to be deployed when needed. Their effectiveness depends on how boards are structured, how information is shared and how dissent is handled.