With the escalation of geopolitical tension in West Asia, economists are looking for monetary policy action to cushion the disruptive impact on growth, investments, capital markets, and more particularly, on business sentiment. The rising geopolitical tension in West Asia has increased risks for India’s trade with West Asian countries, as net importing countries like India depend on the Strait of Hormuz for crude oil and LNG.

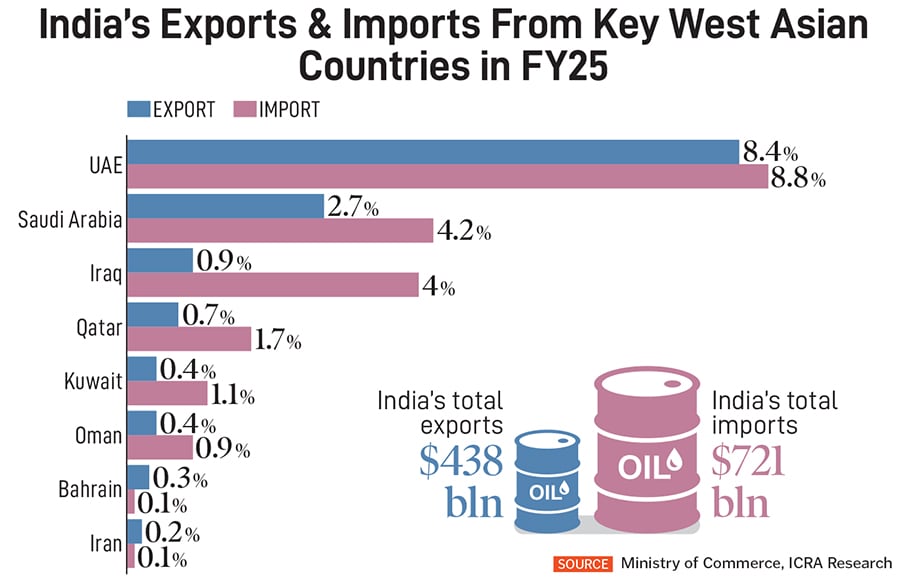

“West Asia accounts for a significant share of India’s trade, with around 14 percent of exports and 20 percent of imports linked to the region. As a result, the conflict poses meaningful risks to India’s trade flows, particularly in the form of higher freight costs, supply delays, and uncertainty over energy supplies,” says Aditi Nayar, chief economist, ICRA Ratings.

The surge in crude oil prices is also feared to widen India’s current account deficit (CAD), hit inflation, and upset fiscal calculations. The initial strikes by the US and Israel against Iran prompted retaliatory actions by Iran, targeting US assets in several West Asian countries, including Saudi Arabia, the UAE, Kuwait, Qatar, Iraq, Bahrain, and Oman. As per the International Energy Agency (IEA), collectively these nations account for 30 percent of the world’s crude oil production and 17 percent of global gas output.

Iran’s response also resulted in the closure of the Strait of Hormuz (SoH)—a critical passage that manages 25 percent of global seaborne oil shipments and 20 percent of LNG exports.

“As India is a net oil importer with inelastic demand, movements in crude oil prices have an important bearing on macro stability and hence economic growth. Higher energy prices would weigh on consumer sentiment, real incomes and spending, while squeezing industrial margins for some sectors,” says Tanvee Gupta Jain, chief India economist, UBS India.

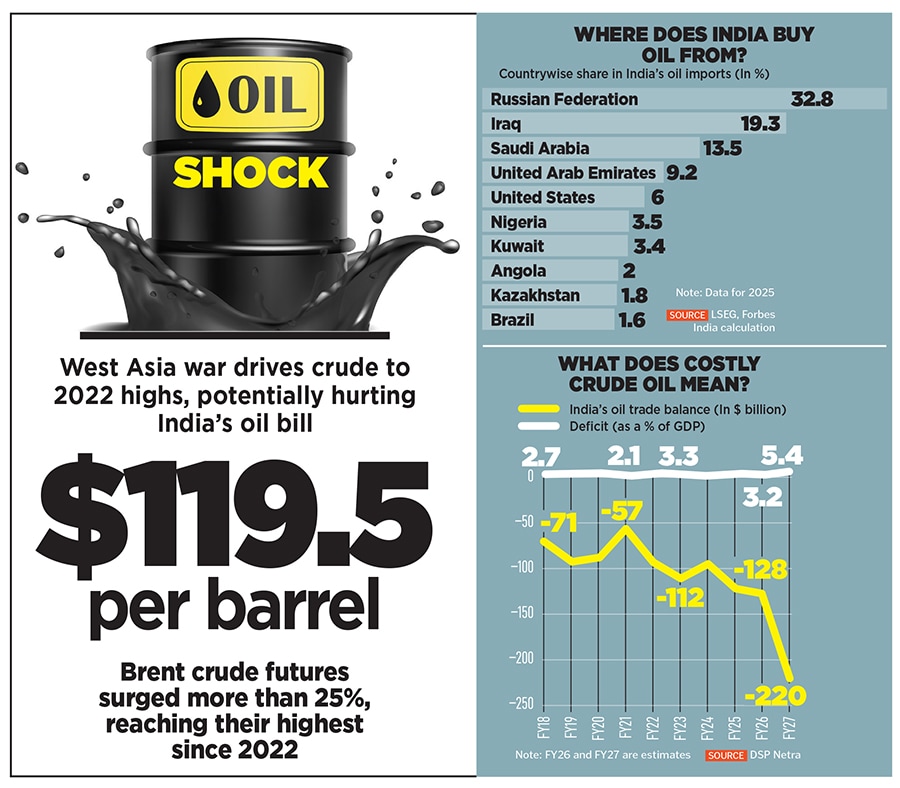

On March 9, Brent crude futures climbed to a high of $119.50 per barrel, surging around 25 percent in a day, the highest since the Russia-Ukraine war in 2022. Soon after, crude oil prices cooled off to below $90 per barrel driven by indications from the US administration that the conflict in Iran may end soon.

![]()

Brian Tan, economist, Barclays, feels the volatility in crude oil prices may not immediately trigger a monetary policy action towards tightening. “While global crude oil prices remain elevated and will likely still exert pressure on central bank inflation targets in the region, we continue to expect policymakers to remain cautious about prematurely tightening monetary policy,” says Tan.

The SoH is the only marine entryway into the Persian Gulf, with Iran on one side and Oman and the UAE on the other. It also links the Persian Gulf to the Gulf of Oman and the Arabian Sea in the Indian Ocean. The closure of this critical oil corridor will lead to a steep increase in oil prices, affecting all countries, even if oil is not imported from the Gulf region, as prices tend to be linked across markets.

“We see three channels of impact for India—risk sentiment, energy pricing, and economic activity,” says Radhika Rao, senior economist, DBS Bank.

How Crude May Upset Fisc

According to Gupta’s estimate, a $100/bbl oil price may widen India’s net oil imports and goods trade deficit by 1 percent of gross domestic product (GDP), all else being equal. A secondary impact would also be felt via remittances, given Gulf countries account for a 36 percent share of the total.

![]()

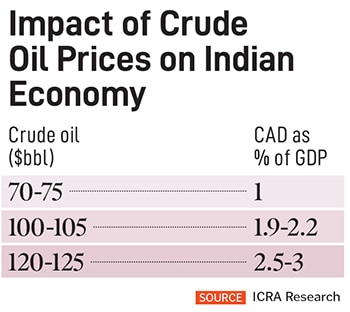

“Elevated oil prices could widen India’s current account deficit by 110–120 basis points of GDP to 2.7 percent in FY27, much higher than the sustainable level of 2 percent of GDP,” Gupta says.

India is the third-largest oil consumer globally, with a heavy reliance on crude imports. The country imports more than 85 percent of crude oil supplies, of which more than 55–57 percent comes from Middle Eastern countries. Around half of crude supplies, amounting to 2.5–2.7 million barrels per day, travels through the Strait of Hormuz, largely from Iraq, Saudi Arabia, the UAE, and Kuwait.

“While global crude oil prices remain elevated and will likely still exert pressure on central bank inflation targets in the region, we continue to expect policymakers to remain cautious about prematurely tightening monetary policy,” Rao says.

She expects the Reserve Bank of India to stay on a prolonged pause on policy rates, while undertaking specific steps to ease market tensions. “Outside of the geopolitical tensions, we continue to expect the rupee to underperform the regional pack, even as the broader dollar might stabilise,” she adds.

![]()

ICRA estimates that for every 10 percent increase in crude oil prices, WPI inflation rises by 80-100 bps, compared with a 40-60 bps uptick in CPI inflation, assuming that full transmission to retail selling prices (RSPs) of fuels takes place. “The quantum of the impact on the CPI inflation trajectory will particularly depend on the extent of the change in RSPs of petrol, diesel and LPG, in terms of the immediate transmission,” Nayar says.

As per estimates by Gupta, there is a 30 bps upside risk to India’s fiscal deficit if higher oil prices continue. For example, to protect Indian households from the impact of rising global oil prices, the government could increase fuel subsidies or reduce excise duties on gasoline and diesel—both of which would affect the country’s fiscal position.

“We estimate that a ₹2-per-litre cut in excise duty for petrol and diesel implies an annualised fiscal impact of about ₹32,000 crore (0.1 percent of GDP),” Gupta explains.

Equities on Tenterhooks

Stock markets across the globe have been on tenterhooks, while in India the VIX has remained elevated, implying weak underlying risk sentiment. Domestic financial markets, including equity price action, bonds and the rupee, have felt the heat from the ongoing hostilities in the West Asia region. The currency had depreciated to a fresh low against the dollar, alongside a tentative stabilisation in the benchmark equity indices after a sharp sell-off.

![]()

“Crude oil prices, at this juncture, are encapsulating the ‘sum of all fears’ arising out of the significant escalation of the conflict in the Gulf region,” says Vinod Karki, equity strategist, ICICI Institutional Equities Research.

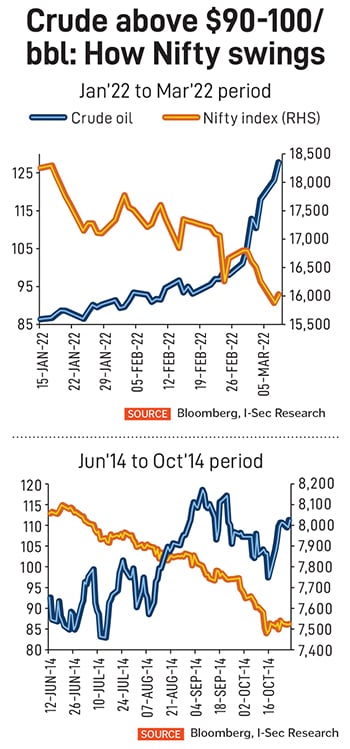

According to his estimates, if crude prices sustain above $100 per barrel, the Nifty could potentially drop by 10 percent, while the price-to-earnings (PE) ratio could drop to 18 times, which is closer to the lowest levels in the post-Covid era.

“Consequently, the earnings yield could rise to 5.6 percent (highest in the post-Covid era), while the relative spread of bond yield over earnings yield could dip to 100 basis points, thereby increasing the relative attractiveness of equities over bonds (assuming bond yields do not spike),” Karki explains.

In 2022, when oil prices spiked beyond $100/bbl for three to four months, driven by Russia’s invasion of Ukraine, the Nifty had slumped 10 percent before rallying the following year.

Overall, steep crude prices negatively affect demand as prices rise. Corporate profitability is also impacted, as fuel and raw material costs for most companies surge.

What’s in it for OMCs?

The heightened risk of supply disruption from the Middle East, a key crude source for Asia, has driven a sharp rise in global oil prices, which will likely intensify financial pressure on oil companies, says Moody’s.

“Price caps and delayed cost pass-throughs will compress margins and increase working capital needs, weighing on near-term cash flows where compensation mechanisms remain uncertain. The speed of the price surge brings fuel-pricing frameworks and the adequacy of financial buffers into immediate focus,” it says.

In India, domestic retail prices of fuels have remained largely steady since April 2022, despite swings in global oil and gas prices and the country’s high dependence on imports.

According to Moody’s, India’s oil marketing companies (OMCs) will bear rising input costs from higher energy prices without corresponding increases in selling prices because the government’s influence over retail pricing prevents timely cost pass-throughs. These companies control nearly 90 percent of retail fuel outlets in the country.

It explains that India stands out among the large Asian economies that rely on crude from the Middle East. The country holds crude reserves covering 74 days’ worth of net oil imports. To ease global crude supply constraints caused by the closure of the Strait of Hormuz, the US government has also granted a 30-day waiver for India to buy Russian oil stranded at sea. These measures increase crude supply options for OMCs.

However, Fitch Ratings believes that an extended closure of the SoH or sustained high oil prices beyond a few quarters could pressure issuers’ near-term credit metrics and standalone credit profiles (SCPs), although ratings will remain supported by strong government linkages and state support.

“In the event of a prolonged disruption, we expect the government to strike a balance between maintaining adequate financial profiles at OMCs while managing domestic inflation and fiscal policy, as demonstrated in the past, which mitigates risks,” Fitch says.