In numbers: India’s debt dilemma

Government pivots to 50 percent debt goal by FY31, navigating interest dues and slowing growth

By Samreen Wani

Last Updated: Jan 19, 2026, 15:15 IST2 min

India has announced plans to significantly reduce its public debt burden, with Finance Minister Nirmala Sitharaman revealing that the government will actively target the debt-to-GDP ratio starting in the fiscal year 2026-27, aiming to bring it down to 50 percent by FY31 (plus or minus one percent).

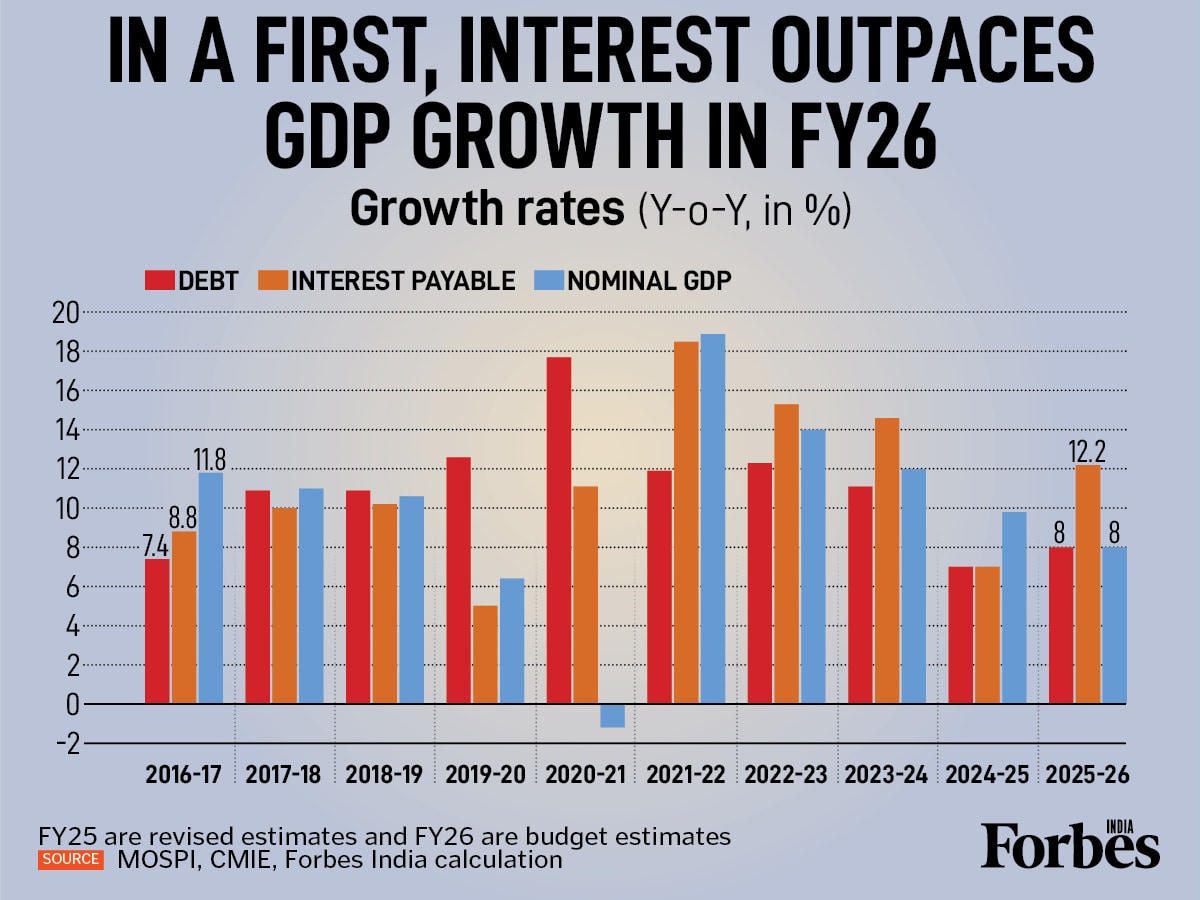

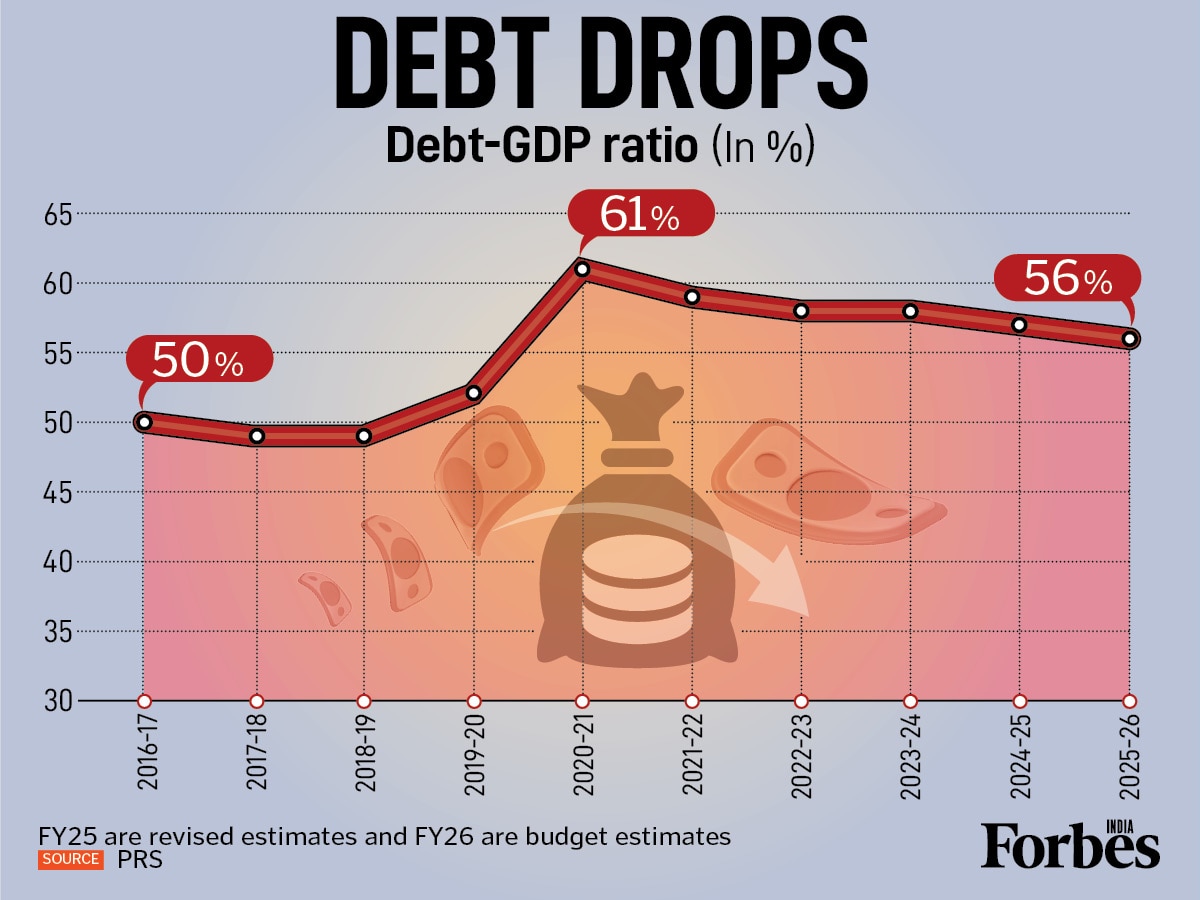

The announcement comes as India’s debt-to-GDP ratio, a key repayment indicator, fell to 56 percent in FY26, down significantly from its 61 percent pandemic peak. While the central government has successfully steered the debt-to-GDP ratio onto a downward path from its pandemic high, for the first time in a decade, the cost of servicing debt is set to outpace economic growth in FY26.

The FY31 target is vital, as a lower debt-to-GDP ratio boosts credit ratings, expands spending capacity, lowers borrowing costs, and drives foreign investment.

The success of India’s fiscal consolidation hinges on maintaining robust growth, as a higher GDP denominator naturally dilutes debt ratios. However, with the FY26 First Advance Estimates pegging nominal growth at 8 percent—well below the long-term average of 10.5 to 11 percent—this moderate expansion will strain debt and deficit targets despite unchanged spending.

Also Read: IMF Raises India’s Growth Forecast to 7.3% for 2025

Central government liabilities, which spiked to 61 percent of GDP during FY21, are projected to moderate to 56 percent by FY26, reflecting recovery efforts after the pandemic expansion. The debt-to-GDP ratio, however, remains higher than pre-pandemic levels.

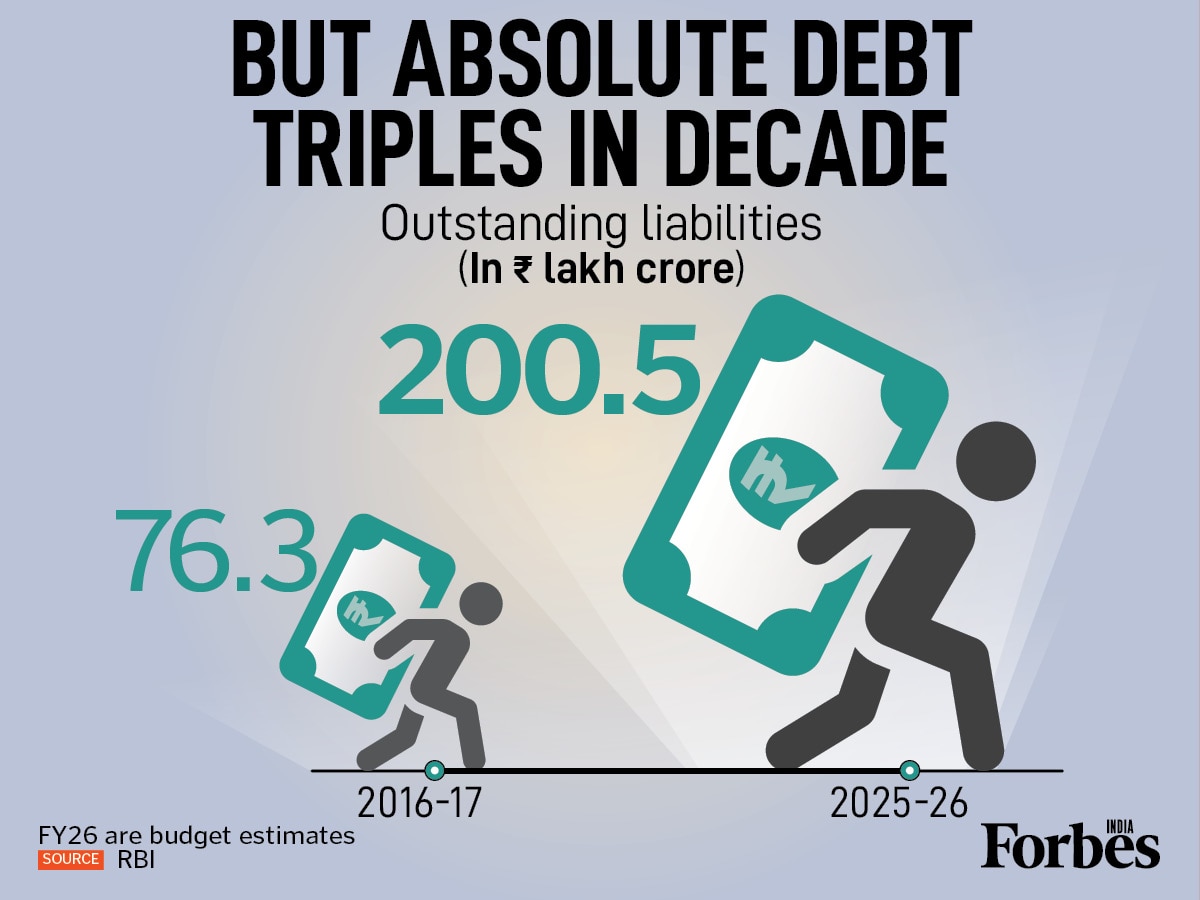

However, there is a surge in absolute terms—over the last decade, India’s outstanding liabilities have nearly tripled from Rs 76.3 lakh crore in FY17.

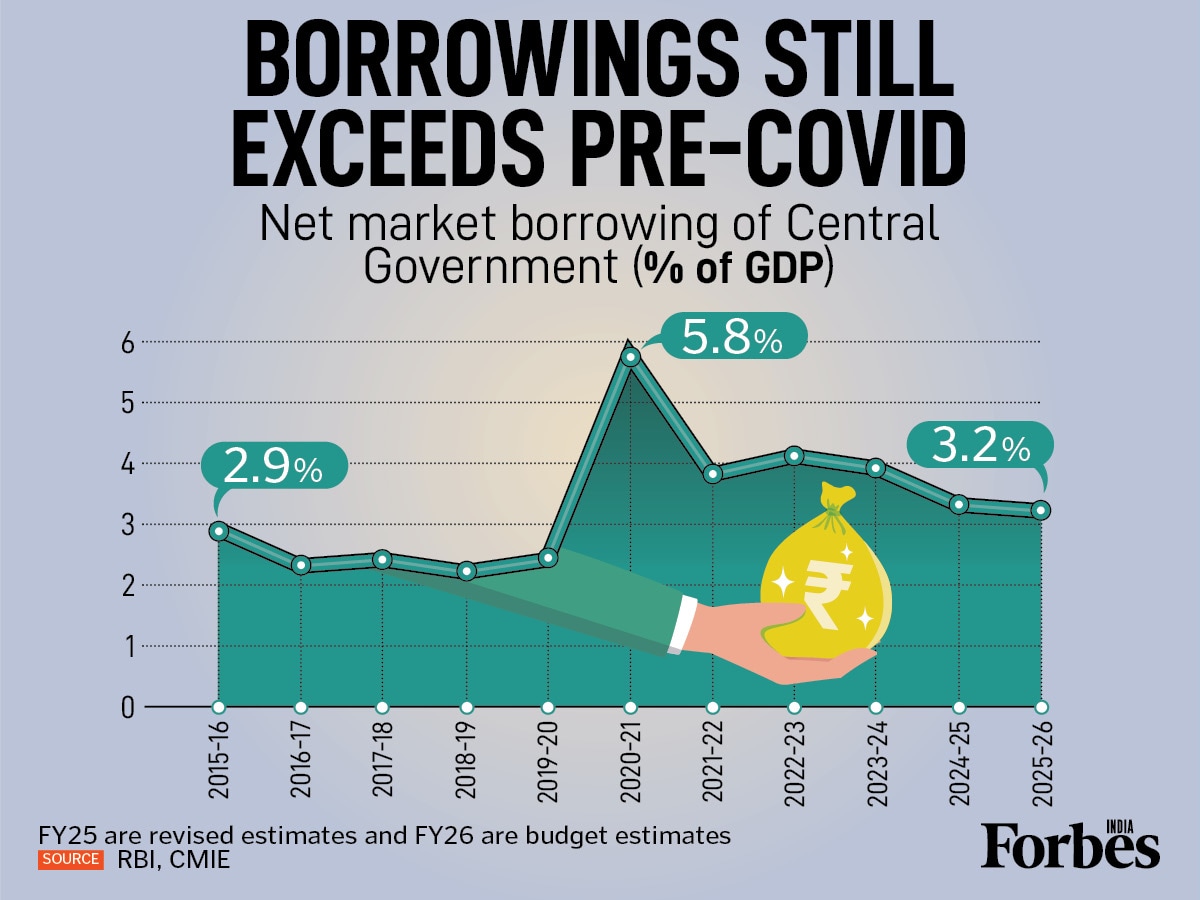

Market borrowings also remain high. At a budgeted 3.2 percent of GDP for FY26, net market borrowings are still significantly above the pre-pandemic level of 2.4 percent seen in FY20.

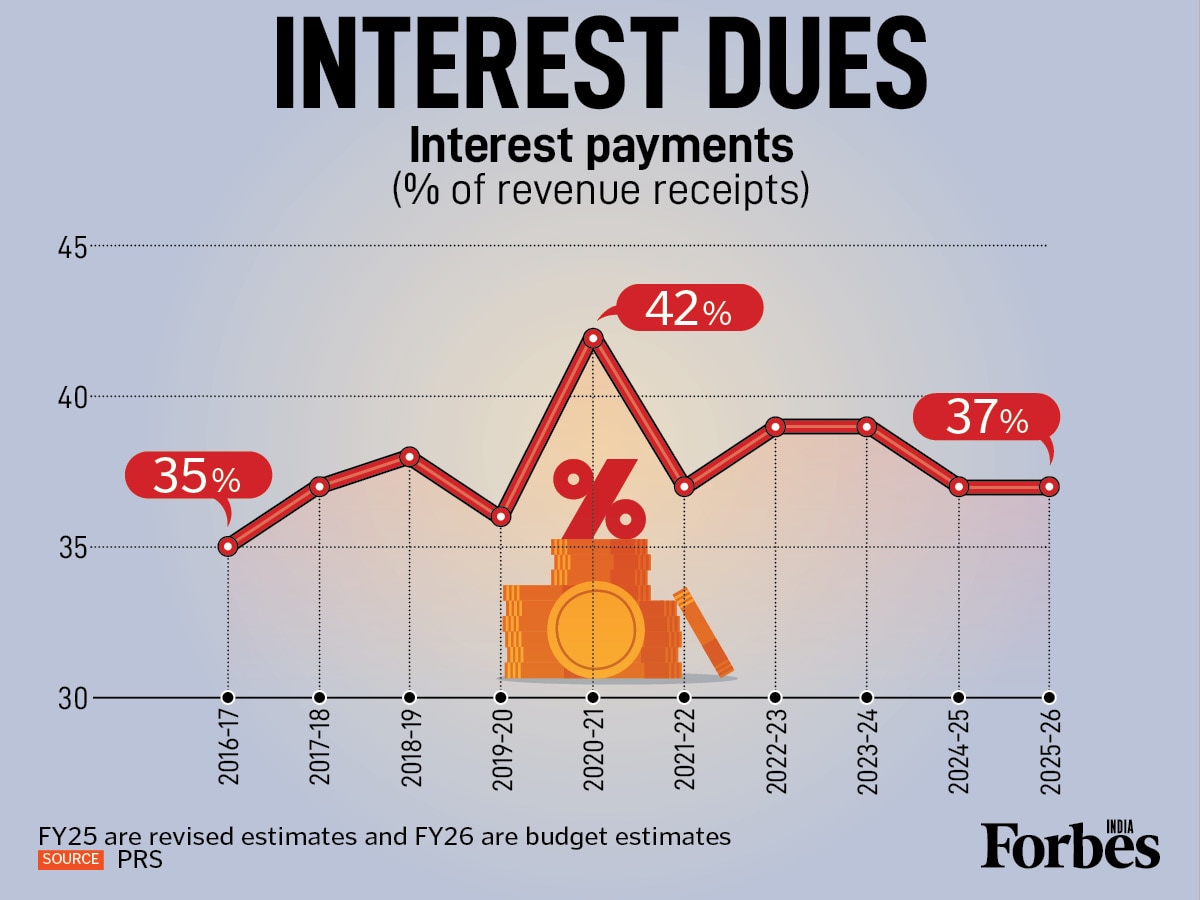

Fiscal pressure is mounting as debt obligations consume nearly 37 percent of revenue receipts, leaving a limited pool available for development spending.

For years, nominal GDP grew faster than interest obligations. In FY26, that trend reverses. While nominal GDP is expected to grow at 8 percent, interest payable is set to grow at 12 percent.

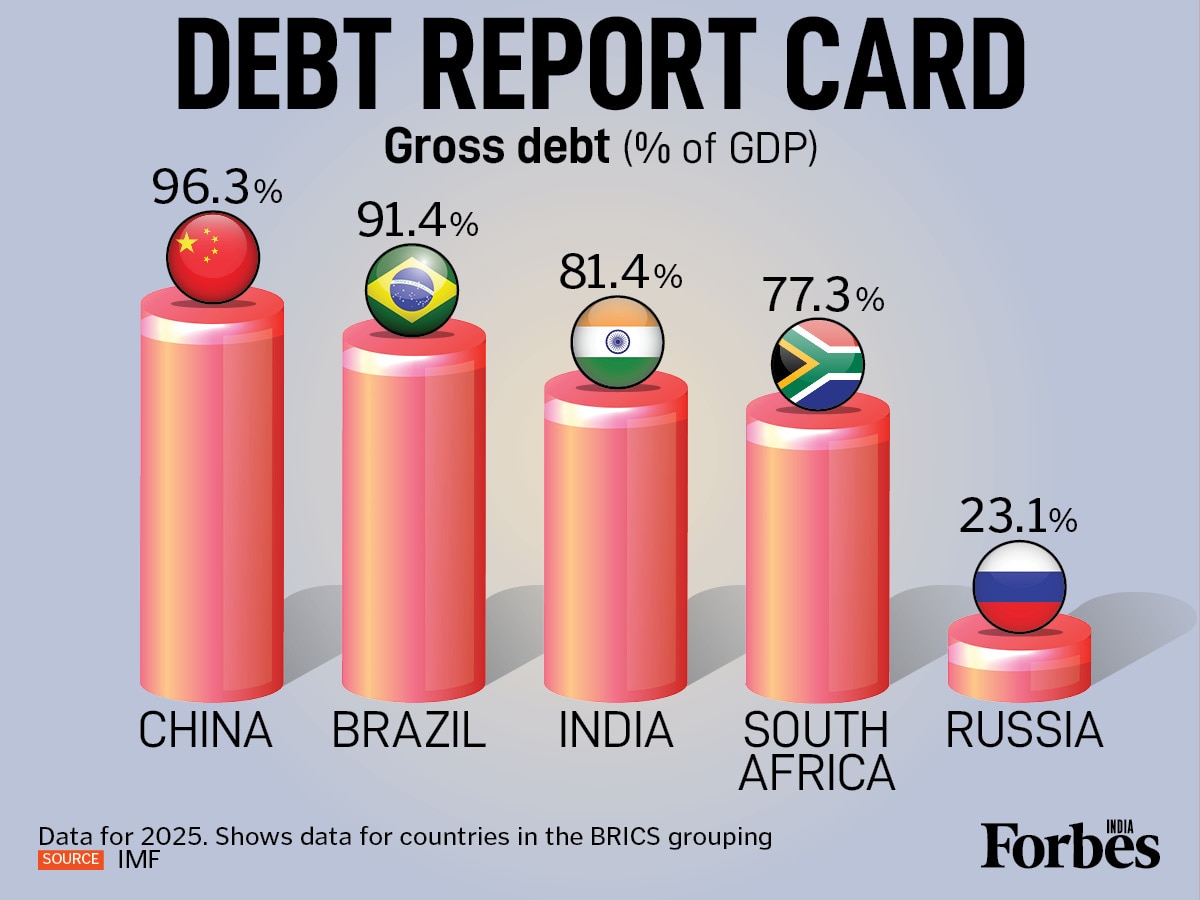

In a global context, India’s gross debt of 81.4 percent (including states) places it mid-pack among BRICS peers—lower than Brazil and China, but significantly higher than Russia.

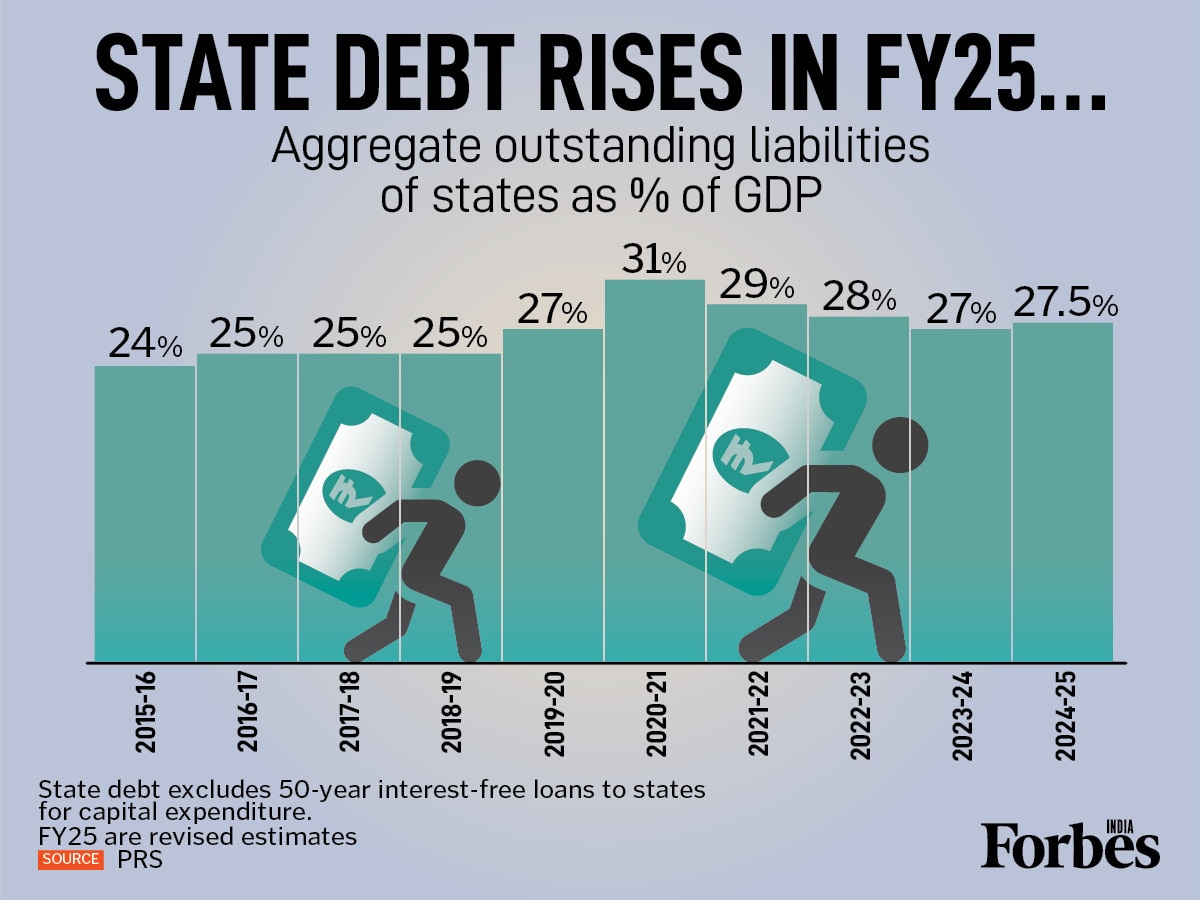

At an event last year, Finance Minister Nirmala Sitharaman urged states to mirror the Centre’s fiscal discipline, warning that failing to manage high-interest debt leads to borrowing for repayments rather than development. While aggregate state liabilities have increased in FY25 and remain higher than pre-pandemic levels, they are largely in line with the 15th Finance Commission’s target for FY25 (30.9 percent of GDP).

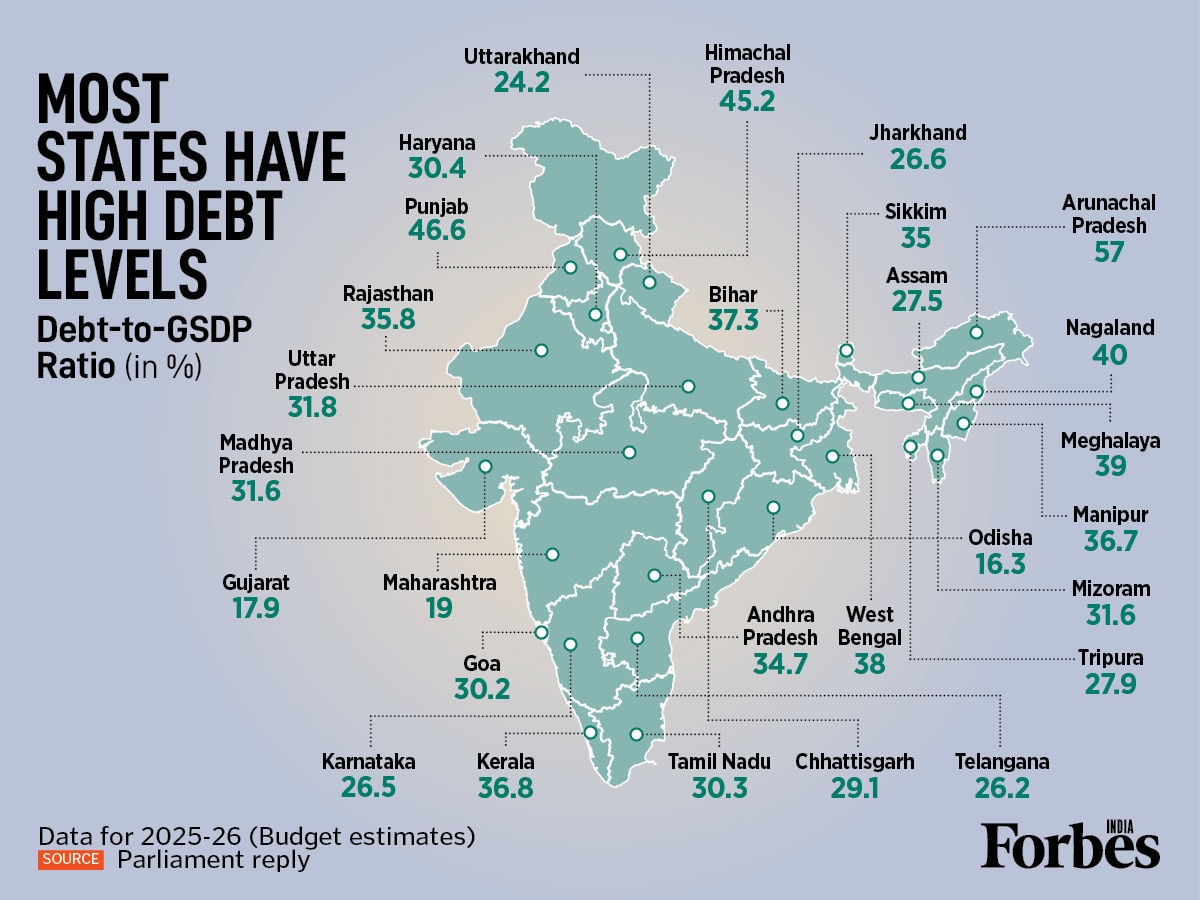

However, the disparity between states is stark. The 2017 FRBM Committee chaired by N.K. Singh set a clear roadmap for fiscal health: a 40 percent debt ceiling for the Centre and 20 percent for states. Yet, by FY25, this benchmark remains elusive for most of Indian states; only Gujarat, Odisha and Maharashtra have successfully contained their liabilities within the recommended limit. Meanwhile, states such as Arunachal Pradesh and Punjab are grappling with debt levels that threaten long-term stability.

First Published: Jan 19, 2026, 15:38

Subscribe Now