Coming of Age: How Flipkart is flipping the script

How India’s startup OG is reinventing itself while consumers evolve, technology gallops, competition intensifies, and an IPO looms

Last Updated: Feb 24, 2026, 16:20 IST13 min

In 2018, Rajneesh Kumar was part of the $16 billion deal process that saw United States-based retail giant Walmart acquire a 77 percent stake in Flipkart. Kumar was, at the time, chief corporate affairs officer and director with Walmart India. The Flipkart he saw back then believed in the philosophy of move-fast, fail-fast, and re-build.

After joining Flipkart Group as chief corporate affairs officer in 2018, Kumar says he saw the company’s DNA evolve right before his eyes. In the Flipkart of today, innovations are first tried out in a controlled environment and governance is embedded in all experiments from the time they are mere concepts. In Kumar’s words, the horizontal ecommerce company, which began life as an online bookseller in 2007 before morphing into India’s answer to Amazon, now has “brakes, so that it can drive faster” with confidence.

So, where is that drive—faster, with confidence—taking Flipkart as it enters the last of its teen years and prepares to launch its maiden public issue at a time when the buzz in Indian ecommerce is largely about the post-pandemic phenomenon called quick commerce (Qcomm)?

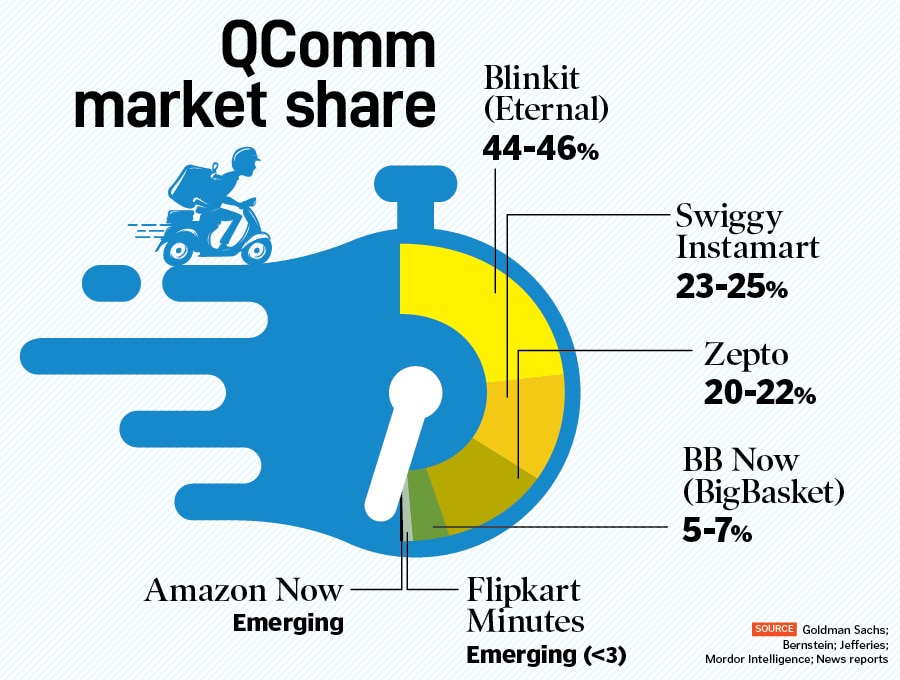

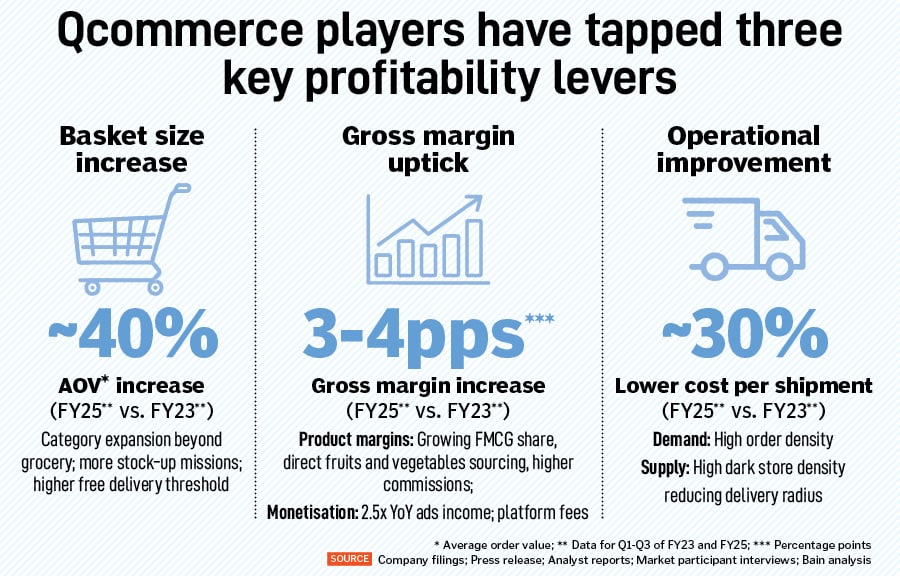

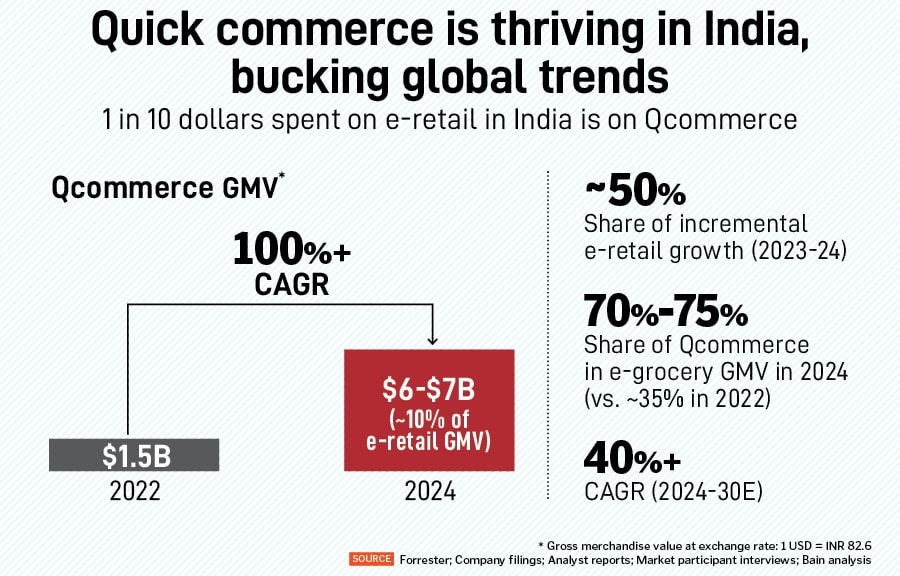

Indeed, Qcomm has changed the way people think of not only online shopping but all shopping. Weekly buying at stores has given way to impulse clicks on apps. Before the pandemic, online deliveries arriving in one day to three or even a week was acceptable. Deliveries are now expected in 10 to 30 minutes. Every segment is riding the QComm wave. From phones to gaming consoles, personal care to printouts of documents, food to domestic help, and everything else in between comes with the promise of 10-minute delivery. In the short period after the pandemic, QComm has quickly come to corner nearly two-thirds of all online grocery orders and promises to grow at 40 percent annually till 2030, according to a report by Bain & Company published in March last year.

To borrow a term from sports, the momentum is with QComm outfits such as Eternal’s Blinkit, Swiggy Instamart, and Zepto, making the old guard of Amazon and Flipkart look old school. Both Flipkart and Amazon have launched their own QComm arms, Flipkart Minutes and Amazon Now, but are seen to be playing catch-up rather than setting the agenda.

The folks at Flipkart, though, appear unperturbed.

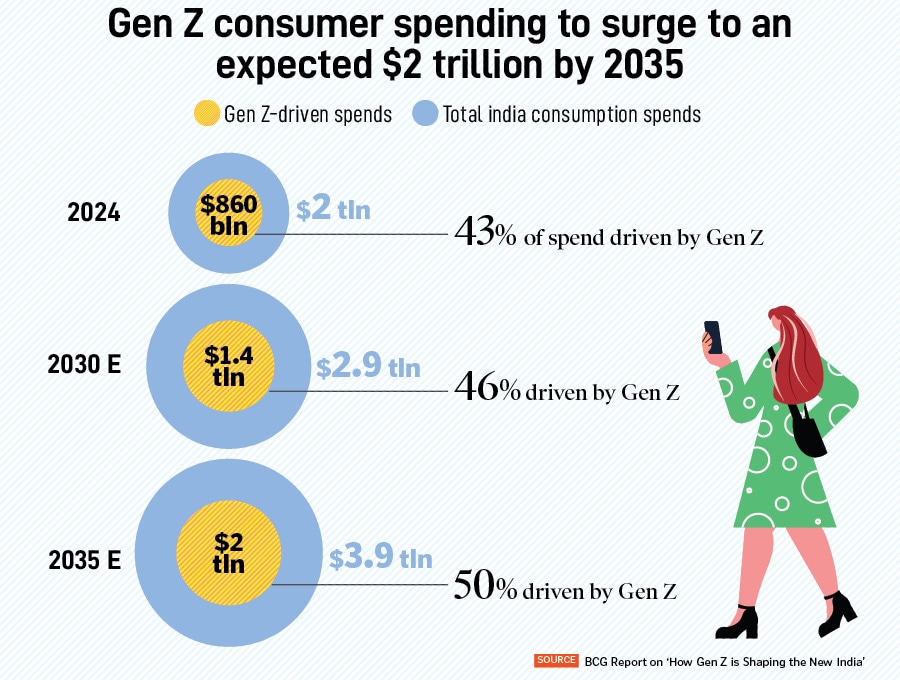

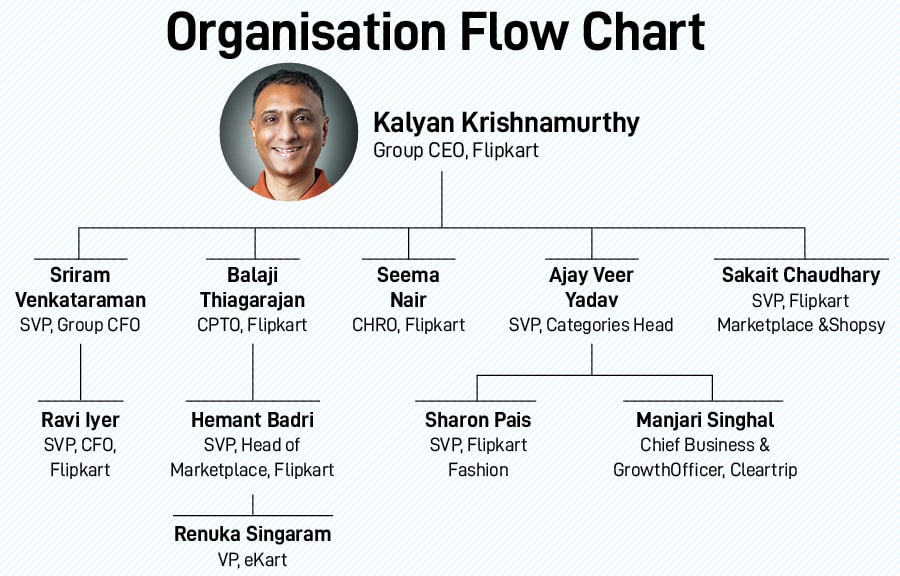

Kalyan Krishnamurthy, who took over as Flipkart’s CEO in 2017 and is now the group CEO, says the last few years have been dedicated to the “future proofing” of Flipkart. At present, the company is working on becoming an artificial intelligence (AI)-first entity, focused on building a platform that would be attractive to Gen Z shoppers. These are people born between 1997 and 2012 who comprise 40 percent of all online buyers in India and show a high potential for growth. Flipkart Minutes, launched in August 2024, is part of this push.

“We identified the need for an AI-first organisation and focused on the Gen Z shoppers as a priority three to four years back and have largely stuck to that. Both the trends will be the differentiator for who wins the Indian customer,” says Krishnamurthy in an interview with Forbes India. He adds that the winner in India’s ecommerce race will be the platform that is agile enough for the new generation of customers. And agility and adaptability will come from being the most AI-enabled.

Also listen: In India's evolving e-commerce scene, can Flipkart make it quick?

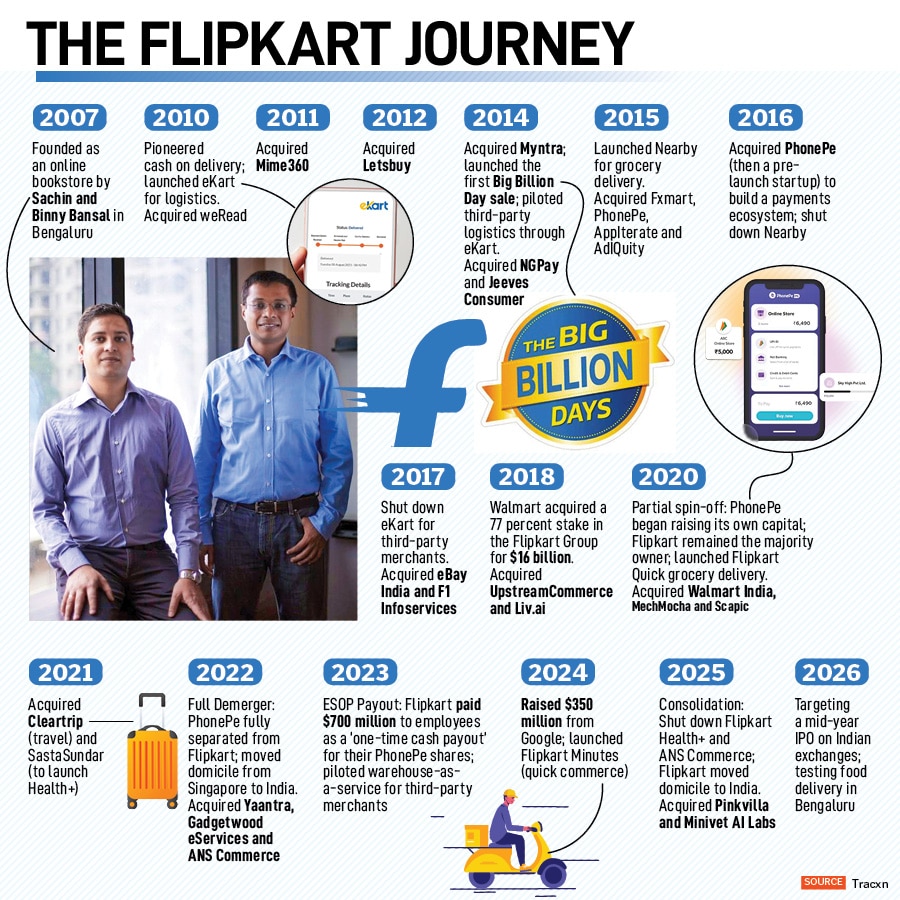

Flipkart was founded by Sachin Bansal and Binny Bansal, IIT Delhi graduates and former Amazon employees, in September 2007 (the website started the following month) out of a two-bedroom flat in Bengaluru’s Koramangala with an initial capital of ₹4 lakh ($6,000 at the time).

Starting as a small online bookstore, it grew by adding electronics, introducing features such as Cash on Delivery, and building its own logistics arm, Ekart—all of which helped it scale through the early 2010s. Its acquisition of Myntra in 2014 cemented Flipkart’s dominance in apparel and remains one of its most strategically important deals in India’s short tech startup history. The company withstood intense competition from Amazon to continue raising large funding rounds and expand into new categories. The historic deal with Walmart in 2018 strengthened its governance and global retail muscle.

Over the years, Flipkart has exited businesses like Nearby, Flipkart Health+, and others. Health+, for its part, had strong tailwinds during Covid, but the overall industry did not scale enough in ecommerce.

“When we started, we were a startup; today we are a corporate. Over the years, while we have retained our nimbleness and agility, we have also built much stronger systems, processes, leadership and talent—people with the right experience,” says Ravi Iyer, the CFO at Flipkart.

More recently, the demerger of PhonePe temporarily lowered its headline valuation from $40 billion to $35 billion, though strong GMV growth of 25–28 percent in 2023 kept its organic value in the $38-40 billion range.

Valued at nearly $36 billion as of 2024, according to data from Tracxn, Flipkart has started the process of reverse flipping by moving its domicile back to India in a move being seen as a precursor to a listing on stock exchanges.

Though the initial public offer (IPO) will be a canon event—it is not every day that one of India’s largest consumer plays tests the public markets with an approximate valuation of $50 billion—this story is not about the process. This story focuses on how the company is reinventing itself in the face of evolving customer expectations and competition from QComm. This coincides with a slowdown in Flipkart’s key GMV (Gross Merchandise Value) contributors while technology and search are undergoing a revolution caused by AI.

AI and Gen Z go hand in hand because, as Krishnamurthy says, India’s Gen Z population is adopting AI very fast. “So how do we make sure we become a destination for the Gen Z force of India? There are 350-400 million young people all empowered with technology and access to information, and Flipkart is a product of that,” he says.

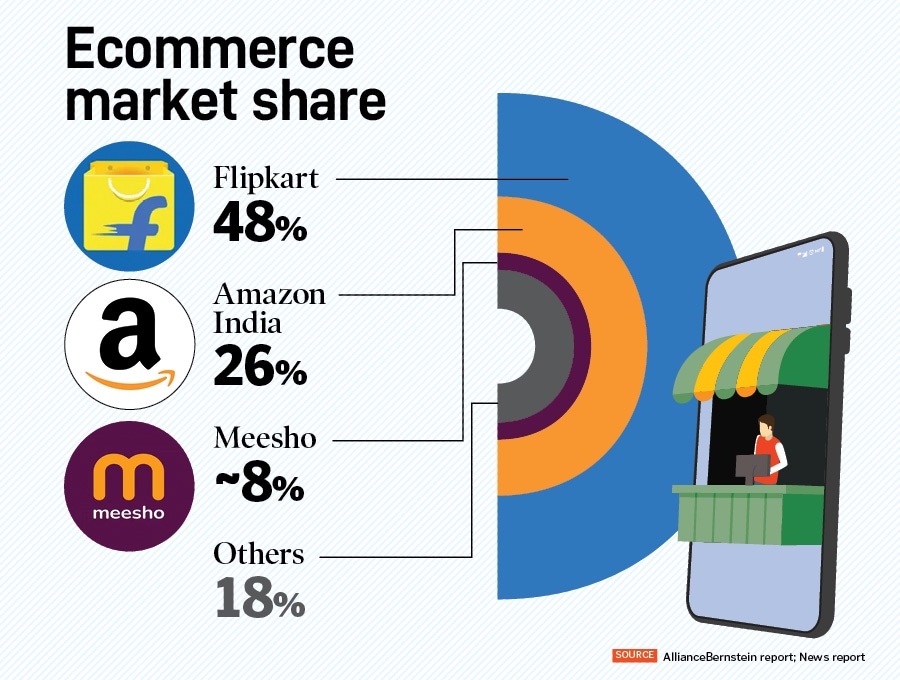

Gen Z is the fastest growing cohort on Flipkart Fashion and is likely to be the largest in a few months. Flipkart Fashion and group company Myntra together command a nearly 40 percent share of India’s online fashion market in terms of GMV, which is the total monetary value of all goods sold on an ecommerce platform. According to market intelligence and advisory company Datum Intelligence, Flipkart Fashion commands a slightly larger pie than Myntra.

To cater to the Gen Z shopper looking for trendy styles at affordable prices, Flipkart works on its search and discovery. “Gen Z has grown up with social media and [for them] there is no divide between local and global. They struggle mainly with the price point. They might not be able to describe an outfit, but they can easily upload a reference picture, and we have made it easier for them to discover those styles... You have to be able to understand what they are saying,” says Sharon Pais, business unit head at Flipkart Fashion.

Having previously served as chief business officer at Flipkart’s fashion entity Myntra, Pais says cohort-specific search becomes important and, based on the search query, the algorithm starts constructing the size and fit the customer is looking for.

While Myntra enjoys a premium customer base with higher Average Order Value (AOV), the AOV for Flipkart Fashion has been historically lower. However, that is changing, says Pais, as the Gen Z shopper typically shops for ‘looks’, including accessories, makeup, and footwear. “This is leading to a diversification of the wardrobe and an increase in AOV,” she adds.

Flipkart also operates Spoyl, a Gen Z-focused fashion store for the value-conscious. “If a complicated material like, say, crochet is trending, which is out of the price-point, the challenge lies in value engineering for the right body size, fit, etc,” adds Pais.

Flipkart has been a market leader in online sales of smartphones and fashion. But these categories have not been growing as rapidly as earlier. According to data by Counterpoint Research, the volume growth in the Indian smartphone market was a mere 1 percent in 2025, though the value of all smartphones sold grew by a record 8 percent, driven by demand for premium devices priced above ₹30,000.

According to Bain, nearly 70 percent of the incremental growth in ecommerce is likely to be fuelled by categories such as grocery, lifestyle and general merchandise by 2030.

Hemant Badri, group SVP and head of Flipkart Minutes, reCommerce, supply chain and customer experience, says Flipkart Minutes is not just delivering groceries in 10-12 minutes but also the range from Flipkart’s ecommerce platform.

“We are Flipkart; we can get your mobile, electronics, home decor, toys—all in 15 to 20 minutes. We want to be a part of your daily-essentials journey and, secondly, we want to bring Flipkart to you in 10 minutes,” says Badri. He adds that nearly 80 percent of Flipkart’s mobile and electronics selection is available through Flipkart Minutes, while the remaining 20 percent is the long tail selection. Long tail in ecommerce refers to niche products of lower value which collectively generate significant revenues due to high sales volumes.

The quick commerce vertical at Flipkart has so far managed to reach 65 cities. The target is 180 cities by the April-June quarter of 2026. However, the quick-commerce forays of horizontal ecommerce platforms like Flipkart and Amazon have been playing catch-up with standalone players such as Instamart, Blinkit and Zepto.

Compared to the incumbents in the market, the throughput of Flipkart Minutes is 50 to 60 percent lower, says Karan Taurani, executive vice president at Elara Capital. “Compared to Blinkit (~2000 orders per day per store) and Instamart (~800 orders per day per store), Flipkart Minutes does around 600 orders per day per store. What works in its favour is the large customer base and deep-tier audience,” adds Taurani.

Apart from the metros, Flipkart Minutes is active in non-metro cities from Bihar-Sharif, Champaran and Bhagalpur to Siliguri and Guwahati. The differentiation for these geographies includes lower cap for free delivery, smaller basket size, and removing the platform fee to encourage adoption.

“Even for the quick commerce players, the share of non-grocery items has increased over time to nearly 20 percent on average, especially through tie-ups with direct-to-consumer brands. Fashion and mobile phones are the categories where Flipkart dominates the market,” says Satish Meena, founder of Datum Intelligence.

Apart from driving adoption, the other challenge for Flipkart’s QComm business is the capital expenditure and having to create a network of dark stores, or micro-fulfilment centres. This makes the business cost-intensive, not to mention wastage and spoilage of perishables. Badri says there are nearly 82 stores being set up every month, and adds that Flipkart harmonises the supply chain for its Qcomm and horizontal ecommerce platforms wherever possible.

“A lot of infrastructure can be common. One channel gets you same‑day or next‑day delivery; one gets you delivery in 15 minutes. Wherever infrastructure can be synergised, we use that synergy to a very high extent,” says Badri.

CEO Krishnamurthy says: “If you are doing it the right way, any business needs investment. We have built a supply chain in India which caters to nearly 22,000 postal codes... So it is not that a particular type of fulfilment model is taking more investment or less. We have built it over the years... Anyone who has built it in a year has probably not built it the right way.”

Another pre-requisite for ecommerce companies to go public is to promise an upside with high growth potential and to show a clear path to profitability—as witnessed by the retail investor sentiment in the markets. While Flipkart Group has been gradually working towards profitability, Myntra registered an EBITDA profit of ₹538.7 crore for FY25 and Flipkart Internet reported an EBITDA loss of ₹4,559 crore, a 17 percent increase year-on-year. EBITDA, short for earning before interest, tax, depreciation, and amortisation, is a tool popular among investors and analysts to measure a company’s core operational profitability and therefore its true value.

The performance of the group is a sum of its moving parts and other operations including Cleartrip, logistics, and revenue drivers such as the Flipkart ads business. Without directly commenting on the preparation for an IPO, Iyer, CFO at Flipkart, says the company is marching along in the right direction.

“We look at it as a portfolio strategy. Every business in Flipkart has a role. Some drive growth, some drive profitability, some drive customer stickiness. We allocate resources such that each category has a clear role and outcome. Given our scale, we are able to operate a portfolio meaningful for the Indian consumer,” he adds.

In a world where horizontal ecommerce gave way to vertical players like Nykaa, followed by direct-to-consumer online brands and quick commerce, there is very little differentiation that a Flipkart or Amazon brings to the table other than its captive customer base, believe industry observers.

The transition of Flipkart from a founder-led company to an operator-led entity has also seen a step-back in the entrepreneurial spirit, observes Arvind Singhal, chairman and managing director of management consulting firm, The Knowledge Company. “When they started… it was before Amazon in India and they had a top-of-the-mind recall with the customers and events like the Big Billion Days sale,” he says. “They have been a follower rather than a trendsetter despite having the first mover advantage, the moment the founder muscles were out.”

However, Vikram Gawande, director of growth investments at Blume Ventures takes a differing view. “Flipkart has a strong parent balance sheet backing them and they are going to do experiments to increase the Lifetime Value of customers on their platform. Food, quick commerce are experiments. PhonePe was one of those backings, which worked and later spun out,” says Gawande.

PhonePe was founded in 2015 by Sameer Nigam, Rahul Chari, and Burzin Engineer and acquired by Flipkart a year later. It came into the Walmart fold when it acquired Flipkart. It is now one of the most successful fintech companies in the country, being the leader in UPI transactions and having forayed into stockbroking and mutual funds.

Having separated from Flipkart in 2022, it was valued at $12 billion in a funding round the following year and is gearing up for its own IPO.

Though Flipkart is in the midst of domiciling its business back to India from Singapore, Krishnamurthy says an IPO or preparation for one will change very little in terms of strategy or compliance and governance. While its peers like Lenskart and successors in the vertical commerce space like Nykaa have already made inroads into the public market, if looked at from an overall public market lens, says Gawande of Blume Ventures, “the average age of companies listed on the public markets over the last decade in India is around 20 years and that said, Flipkart is still not late to go public”.

With US-based retailer Walmart holding the role of the promoter in Flipkart, the path to an IPO will be an exercise in legal considerations and finding the path of least resistance.

“IPO is not a destination for me personally,” says Krishnamurthy. “Our responsibilities go up in a very big way once the company is public, and the way we look at it, we are ready to face those responsibilities. The stakeholder complexity changes once we are public, and ‘are we ready with a future-proof business’ is the way we have been thinking about it, rather than what happens at an IPO.”

He adds that though there is no timeline, his role is that of the manager of a capable team and the decision of the board will be binding on the timing.

“Indian law does not prohibit majority foreign ownership per se, but it does regulate it in a highly calibrated manner,” says Shreevardhan Sinha, senior partner, corporate and commercial, at law firm Desai and Diwanji. “The permissibility and compliance burden depend on the sector, the applicable FDI cap, and whether the investment falls under the automatic or approval route.” He adds that companies with significant foreign shareholding require early alignment between corporate governance structures and foreign investment rules rather than reactive compliance.

Investor fatigue, though, is a real thing, believes Singhal of The Knowledge Company. “Walmart comes from a different DNA where they were not an online business to begin with. They also lack the muscle of an Amazon, where the parent company can drop ship private labels to India, sourced globally. Flipkart’s private labels haven’t really made a mark,” he says, and adds that even with its foray into food delivery, Flipkart is entering a territory dominated by two large players.

Until the IPO becomes a reality, Flipkart’s reinvention to stay ahead in a changing online retail landscape will be closely watched.

First Published: Feb 24, 2026, 16:43

Subscribe Now(This story appears in the Feb 20, 2026 issue of Forbes India. To visit our Archives, Click here.)