Over the ensuing year, those 150 US deaths swelled to 550,000 some 3 million souls were lost worldwide. Tens of millions of jobs evaporated, along with hundreds of thousands of small businesses. Remote work went from exotic to standard. The suburbs went from dull to desired. The death of George Floyd triggered a reckoning concerning race and social justice. The presidential election tested democratic norms. Simultaneously, though, many individuals, industries and investments thrived.

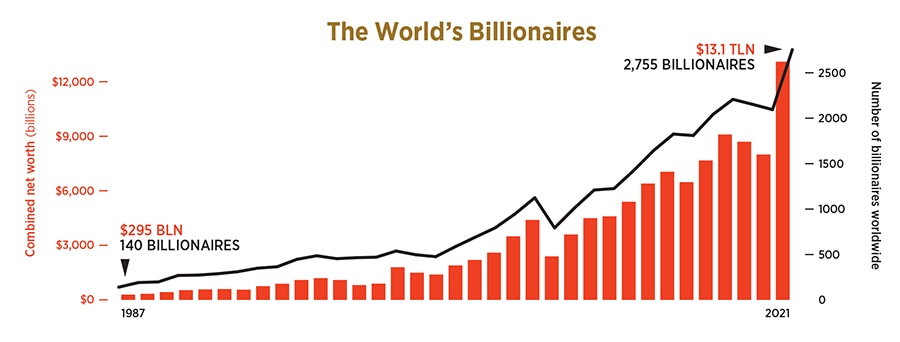

One year after that fortuitously timed snapshot, we repeated our March billionaires audit, taking the measure, at the point of the pyramid, of the past year’s seismic changes. The results defy hyperbole. Over the past 12 months, 493 people worldwide joined the Forbes list—a newly minted billionaire every 17 hours. Rising asset prices vaulted another 250 previous drop-offs back over the ten-digit mark. Amid widespread economic insecurity, precious few billionaires fared worse financially: Just 61 dropped off the list for reasons other than death, representing the lowest percentage of drop-offs for any year on record. All told, Forbes estimates that there are now 2,755 billionaires globally, up from 2,095 last year, and the notion that the rich get richer has never been more apt: They’re worth, in aggregate, $13.1 trillion—a staggering $5.1 trillion more than at the start of the pandemic.

These figures will engender endless amounts of consternation, most of it justified. There’s no getting around a collective $5 trillion wealth surge during a pandemic, when most of the world felt scared, sick, besieged. Capitalism, the greatest system ever for generating prosperity, rests upon a social compact of expansion, unequal by design, ultimately lifting all boats. The Covid-19 economy has strained that concept yawning economic disparity poses arguably the greatest threat to modern social order.

But as miraculous vaccines chart a course back to normalcy, the factors driving these numbers conjure a different emotion: Optimism. The pandemic’s most enduring positive legacy will turn out to be as an accelerant, compressing decades of change into one year. And the newly super-rich, proxies for opportunity, or lack thereof, have never felt more different, looked more different or acted more different. It’s worth spending some time to deduce why.

We’re at that rarest of inflection points—the kind that’s apparent even as it happens. Vaccines will wash across the planet at the same time the global economy seems primed to roar back. And while the initial reaction to the billionaire surge of 2021, a newcomer tally 70 percent larger than any we’ve logged before, will lean toward outrage, the underlying trends offer a road map to greater prosperity for all. Like anything else salvaged from a once-a-century plague, we just need to be brave enough to harness it.

![]() John Arnold was the first billionaire to get behind a new ‘Give While You Live’ promise—a public commitment to grant at least 5 percent of his personal net worth to good causes each year

John Arnold was the first billionaire to get behind a new ‘Give While You Live’ promise—a public commitment to grant at least 5 percent of his personal net worth to good causes each year

*****

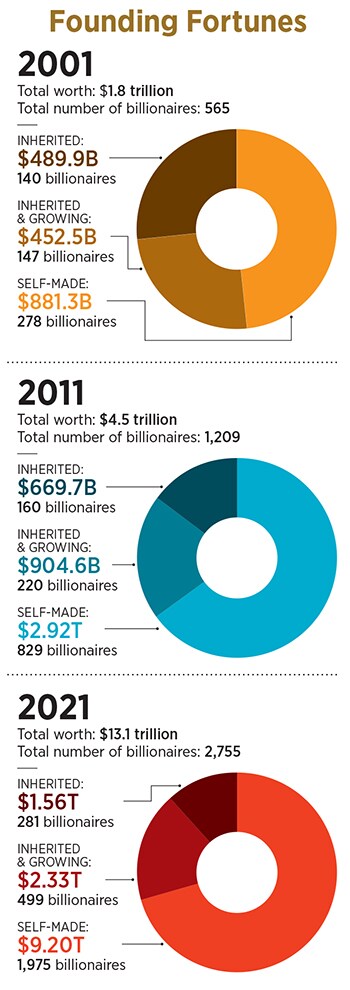

For pretty much all of human history, wealth has been dynastic. The John D. Rockefellers and Henry Fords of a century ago launched the first era of entrepreneurship, but even those successes turned into entrenched family wealth. The very first Forbes 400 list of the richest Americans, in 1982, remained chock-full of their progeny, as well as plenty of Mellons, DuPonts and the like—some 63 percent of that inaugural Rich List pretty much inherited it. Many of the rest had a background that involved starting life on first, second or third base, in the mould of Rupert Murdoch or Donald Trump.

The technology revolution changed that dynamic, here and around the world. By 2002, a slim majority, 52 percent, of the Forbes global billionaires were self-made, including 59 percent of Americans. Ten years ago, that total had jumped to 69 percent globally.

The 493 new members of the Covid Newcomers of 2021, however, are in a class by themselves: 84 percent of them are self-made (including 90 percent of Americans), swelling the figure among billionaires overall to 72 percent—a record in each case. People like Whitney Wolfe Herd, who flipped the script on dating apps by empowering women Tyler Perry, who started producing his own movies and television shows in Atlanta because no one would give him a break in Hollywood and UÄŸur Åžahin, the Turkish immigrant to Germany whose BioNTech helped produce a Covid-19 vaccine in months rather than years—all embody economic dynamism, not bloodline dynasties.

![]()

Opportunity stems from this dynamism, as these new billionaires illustrate. A decade ago, the median length of time it took a new billionaire in America to create his or her fortune, according to our data, was 18 years. Historically speaking, that’s extraordinarily fast.

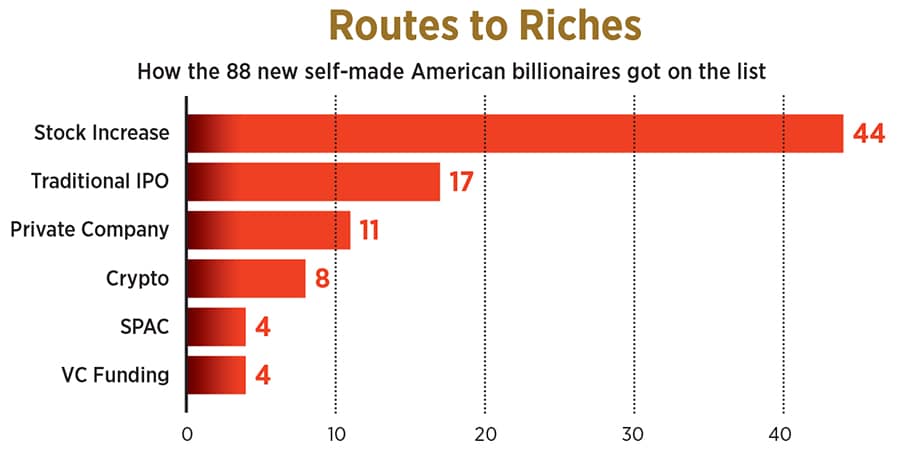

Among this year’s 88 new self-made Americans, that number has decreased drastically, to 13 years. The ability to rapidly translate ideas into riches helps level the playing field. Code (intellectual resources) trumps capital (accumulated resources), with the latter desperate for the former. A generation ago, fortunes went to those with the luck or pluck to secure funding today, a good concept chooses which funding to accept.

That increased opportunity has in turn changed what a billionaire looks like. While women continue to have a far harder time getting good ideas funded than men, they’ve nonetheless steadily nudged up the tables and now encompass 11 percent of global billionaires, 12 percent of American billionaires and 13 percent of new billionaires, all high-water marks. More importantly, female entrepreneurs now account for 4 percent of all billionaires, more than double the percentage even five years ago.

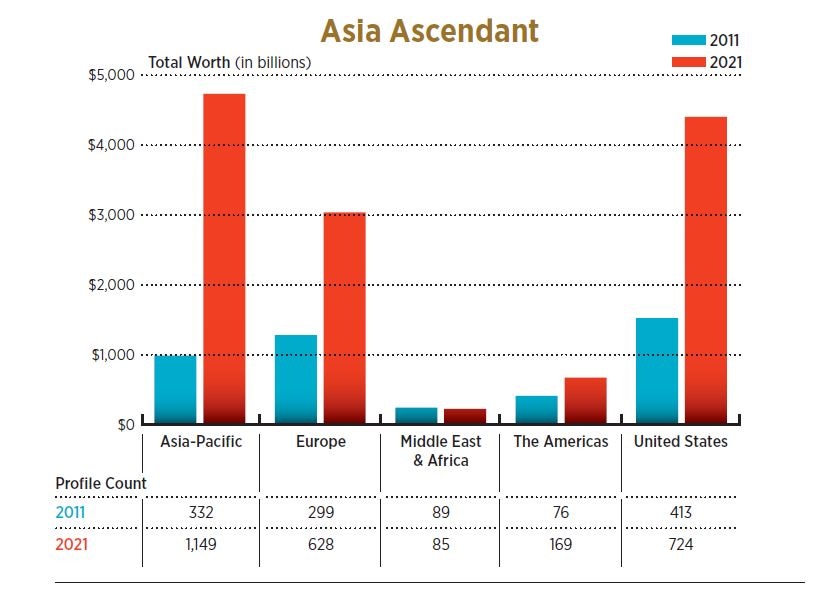

![]() And while in America extreme success remains disproportionately white, the global business aristocracy increasingly reflects the world itself. China alone, including Hong Kong, added a staggering 210 billionaires this past year. Factor in 19 new faces from India, 14 from Japan and multiple debuts from seven other Asian countries, and people of colour made up a majority of new billionaires worldwide.

And while in America extreme success remains disproportionately white, the global business aristocracy increasingly reflects the world itself. China alone, including Hong Kong, added a staggering 210 billionaires this past year. Factor in 19 new faces from India, 14 from Japan and multiple debuts from seven other Asian countries, and people of colour made up a majority of new billionaires worldwide.

How do these more meritocratic, more dynamic, more diverse billionaires run their companies? In ways that are better for all of us. Forbes contracted with our partners at JUST Capital, which measures corporate citizenship, to gauge the civic performance of the 88 new self-made US billionaires. We took the companies that drove each billion-dollar fortune and, leaning on industry averages, calculated each score based on how they treat their workers, their customers and the environment, among other factors. The net result: Not only did these new billionaires found or run companies that rank above average in terms of the three factors mentioned above, but they’ve also improved in each of these categories when measured against the new billionaires of 10 years ago.

Take Chris Britt, who in eight years has built Chime into one of the world’s largest digital banks. In a fee-based industry that’s often adversarial to those who need it most, Britt grabbed market share during the pandemic with low-risk, customer-centric gestures. “We’re on the front line," he says. “We see how Americans are stressed out." Leveraging customer records, Chime comfortably advanced people against their stimulus checks at no cost, and offered overdraft protection via a programme called SpotMe. (By comparison, payday-loan companies lend against things like stimulus checks at usurious interest rates as high as 650 percent.) Such customer-friendly policies, Britt says, help him recruit better employees—his payroll has tripled to 800 in a year—which leads to better returns. “You get those pieces right, with a good business model, the equity shareholders will manage just fine." Apparently so. As of September, Chime was valued by venture capital investors at $14.5 billion, with Britt’s stake worth $1.3 billion.

Still more new billionaires are taking steps to support their employees. Mat Ishbia, the 41-year-old CEO of United Wholesale Mortgage, had an incredible past 12 months, as millions changed where they lived or refinanced with record-low interest rates. Equally incredibly, he’d never taken on partners or investors, so he and his family owned 100 percent of the company going into the pandemic. When he took the company public this January through a SPAC, pushing his net worth at the time to $12.6 billion, he carved out $35 million in stock for his 8,000 workers.

“We all won together as a company," says the former Michigan State basketball player. Well, to some degree. Throwing your employees about one-quarter of 1 percent—an average payout of about $4,000—when you’re sitting on 99.7 percent and almost 11 digits seems exceedingly paltry. But it’s also progress. Go back to that original Forbes 400 list from 1982, and you’ll find hundreds of tycoons who didn’t think of their employees as much more than a cost or liability.

![]()

Others took stands for their hometowns, including Jeff Lawson, the co-founder of surging cloud communications business Twilio, who hit the list this year at a cool $2.2 billion. Silicon Valley saw many companies and leaders decamp from the Bay Area, Elon Musk and Larry Ellison most notably. Lawson felt that he had an obligation to his community, which is another factor measured by JUST Capital. So he publicly declared in January that his company would stay in San Francisco. Another civic booster, Rocket Mortgage founder Dan Gilbert, whose net worth exploded past $50 billion over the last year, recently committed $500 million from his company and his personal foundation to bolster low-income residents of Detroit, where he’s headquartered, which included wiping out the property-tax debt of 20,000 homeowners. “Our commitment to Detroit is absolute," Gilbert tells Forbes.

*****

All this acceleration comes with a heightened realisation among those at the very top about the obligations that come with extreme success—and the possible repercussions, from confiscatory tax regimes to social unrest, that could follow inaction. It’s not hard to read the tea leaves—altruism, in this case, mirrors self-interest. Speaking with a half-dozen members of the newcomers of 2021, along with a handful of younger billionaires, the post-pandemic attitude change is palpable.

John Arnold sensed a shift as the pandemic approached. While the path he took to his estimated $3.3 billion fortune—trading energy contracts for disgraced and defunct Enron—won’t earn him any Nobel laurels, he and his wife, Laura, have spent the past decade creating a plan to maximise their impact—“the benefit," he says, “of looking at 100 years of great wealth in America." Alarmed at the state and standing of philanthropy in the US today, he convened a handful of philanthropists, academics and foundation heads in New York in January 2020, posing a question: How can we get those sitting on trillions of dollars to take bigger, faster action, with more accountability?

![]() That group evolved into the Initiative to Accelerate Charitable Giving. Its primary targets: The $142 billion in donor-advised funds, or DAFs, which allow donors to take upfront tax deductions for parking money in community foundations or financial-services firms, even if there’s no mandate or visibility for when or how the money goes to the public good and perpetual foundations that try to end-run annual minimal giving requirements by sliding in expenses when they report.

That group evolved into the Initiative to Accelerate Charitable Giving. Its primary targets: The $142 billion in donor-advised funds, or DAFs, which allow donors to take upfront tax deductions for parking money in community foundations or financial-services firms, even if there’s no mandate or visibility for when or how the money goes to the public good and perpetual foundations that try to end-run annual minimal giving requirements by sliding in expenses when they report.

But Arnold also feels the super-rich need to go further individually.

So he became the first billionaire to get behind a new “Give While You Live" promise—a public commitment to grant at least 5 percent of his personal net worth to good causes each year—which is being organised by the advocacy group Global Citizen. (Disclosure: I’m a board member at Global Citizen.) Merely holding money in a DAF or a foundation doesn’t cut it, nor does the excuse that rich people are better off compounding their money and giving it away later. “Problems compound too," Arnold says in his first interview about this initiative. “Let this generation handle this generation’s problems."

The Give While You Live concept is a more time-urgent spin on the Giving Pledge, which has admirably pushed billionaires to publicly commit to give away half of their wealth while they’re still alive—or after they die. “It hasn’t necessarily spurred giving in the short term," says Arnold, a Giving Pledge signatory. Pretty much every new billionaire Forbes spoke to, while expressing general support for the Giving Pledge and an openness to committing to it, focused instead on what they can do immediately.

Over the past 12 months, the world’s third-richest woman, MacKenzie Scott, who joined the Forbes Billionaires list last year after divorcing Amazon’s Jeff Bezos, went on a giving spree as notable as anything in recent philanthropic history. Rather than endow a foundation, Scott enlisted advisors to generate data on the ways her money can help the most people now. Then, in July and December, she transparently wrote 500 checks, totaling $5.8 billion, no strings attached, to grantees in all 50 states, many of whom were utterly surprised when the money arrived.

“The pandemic has been a wrecking ball in the lives of Americans already struggling," Scott wrote in a public statement. (She hasn’t given an interview since the divorce.) “Meanwhile, it has substantially increased the wealth of billionaires."

It certainly increased the wealth of Jared Isaacman, CEO of Shift4 Payments, a Square competitor that focuses on restaurants and hotels. His roller-coaster year took him from preparing for a public offering to worrying if his customers—and his company—would survive, to becoming an indispensable tool for his clientele, to pulling off an IPO after all.

After ringing the bell at the New York Stock Exchange, which gave him a $1.4 billion net worth, Isaacman, 38, wrote a $100 million check to St. Jude Children’s Research Hospital. His motivations mimicked Scott’s. He gave immediately after coming into immense wealth.

Rather than set up a foundation, he steered money to people already doing good work. He did so transparently. And he did it with scale, after his business’ brief near-death experience underscored for him how many people were hurting. “If you had asked me before the pandemic, ‘Could you imagine writing a $100 million check?’, I never would have expected it."

Then Isaacman, who owns and flies his own MiG fighter jet, applied some leverage. He announced he would lead the first all-civilian mission to space, in partnership with Elon Musk’s SpaceX. He would bring a St. Jude frontline worker—as well as a random St. Jude donor, a stunt he hopes will raise another $200 million for the hospital, which he publicised through a Super Bowl commercial. He even got Musk, a charitable skinflint to date, to commit to St. Jude.

Immunologist Tim Springer’s coronavirus epiphany has been a matter of scale. Twenty years ago, he netted $100 million founding a biotech company, and in turn he made the kinds of donations you might see from people at that wealth level, endowing chairs at Harvard Medical School and Boston Children’s Hospital. He also put about $5 million into a little startup called Moderna—a stake that brings him onto the Billionaires list this year with a net worth of $2.2 billion.

Springer has already put forth $30 million to establish the Institute for Protein Innovation, a non-profit that creates tools and provides expertise for biotech researchers and entrepreneurs. But the urgency of the moment has him rethinking things philanthropically—later this year, he says, he’ll announce a bigger donation. He’s coy about it, though he does say he’ll likely be “adding another zero". And that’s just the beginning. “I want to give more money. That’s my motivator to start companies now," he says. “If I’m successful, as I think I could be, [with] the scale of things, we could add yet another zero."

And if starting businesses designed specifically to create billion-dollar charitable windfalls sounds far-fetched, meet 29-year-old Sam Bankman-Fried, who’s already doing exactly that. Perhaps the most interesting new billionaire in the world, Bankman-Fried started the FTX cryptocurrency exchange two years ago, making a bigger fortune—$8.7 billion—more quickly than anyone under 30 ever has, Mark Zuckerberg included.

From Carnegie to Rockefeller, Gates to Buffett, philanthropy was always the by-product of entrepreneurship. Bankman-Fried is surely the first billionaire for whom entrepreneurship was the by-product of philanthropy. He embraces a philosophy called Effective Altruism, which has cropped up over the last decade and applies rational logic to maximising good. “It’s for people who like math and people who like giving," Bankman-Fried says. Effective Altruists try to quantify things like lives saved per dollar. Or whether it’s more urgent to quell malaria or potentially malevolent technologies. Or whether a brilliant MIT student named Sam should follow his dream and become an animal-rights activist. “Honestly, you should go to Wall Street and give it to us," Bankman-Fried remembers hearing from one of the Ethical Altruism movement’s leaders, 34-year-old Oxford professor William MacAskill. “You’re not the best leafletterer we’ve found."

Mission accomplished. Bankman-Fried, in pursuing a vocation less than noble—a zero-sum, notoriously cut-throat exchange in which newcomers face a slew of sharp-elbowed pros—has created a massive source of wealth that he promises to deploy almost entirely for what he sees as the public good. (He says he will keep only a few percentage points for himself, and even that might prove too much. “If it’s used to justify buying a few yachts, that’s pretty bad.") And while he’s already placing bets, backstopping a few charitable initiatives and giving $5 million to help get Joe Biden elected (Effective Altruists like Bankman-Fried don’t differentiate much between non-profits and politics they merely look at outcome ROIs), he anticipates accelerated scale starting in five years, when he’s more liquid.

The only reason he won’t give it all away as fast as possible is so that he can keep some powder dry for the moment, sooner rather than later, when he sees an “outlier opportunity."

“When you find one of those, everyone tends to go too small," Bankman-Fried says. “F--king go all in."

We’re at an all-in moment in history, actually, and those at the top have raised their own stakes to a level that’s unfathomable considering the year we’ve all experienced. Changes are upon us faster than we could possibly have conceived last March. Now is not the time for the world’s billionaires, or any of us, to go small.

John Arnold was the first billionaire to get behind a new ‘Give While You Live’ promise—a public commitment to grant at least 5 percent of his personal net worth to good causes each year

John Arnold was the first billionaire to get behind a new ‘Give While You Live’ promise—a public commitment to grant at least 5 percent of his personal net worth to good causes each year

And while in America extreme success remains disproportionately white, the global business aristocracy increasingly reflects the world itself. China alone, including Hong Kong, added a staggering 210 billionaires this past year. Factor in 19 new faces from India, 14 from Japan and multiple debuts from seven other Asian countries, and people of colour made up a majority of new billionaires worldwide.

And while in America extreme success remains disproportionately white, the global business aristocracy increasingly reflects the world itself. China alone, including Hong Kong, added a staggering 210 billionaires this past year. Factor in 19 new faces from India, 14 from Japan and multiple debuts from seven other Asian countries, and people of colour made up a majority of new billionaires worldwide.

That group evolved into the Initiative to Accelerate Charitable Giving. Its primary targets: The $142 billion in donor-advised funds, or DAFs, which allow donors to take upfront tax deductions for parking money in community foundations or financial-services firms, even if there’s no mandate or visibility for when or how the money goes to the public good and perpetual foundations that try to end-run annual minimal giving requirements by sliding in expenses when they report.

That group evolved into the Initiative to Accelerate Charitable Giving. Its primary targets: The $142 billion in donor-advised funds, or DAFs, which allow donors to take upfront tax deductions for parking money in community foundations or financial-services firms, even if there’s no mandate or visibility for when or how the money goes to the public good and perpetual foundations that try to end-run annual minimal giving requirements by sliding in expenses when they report.