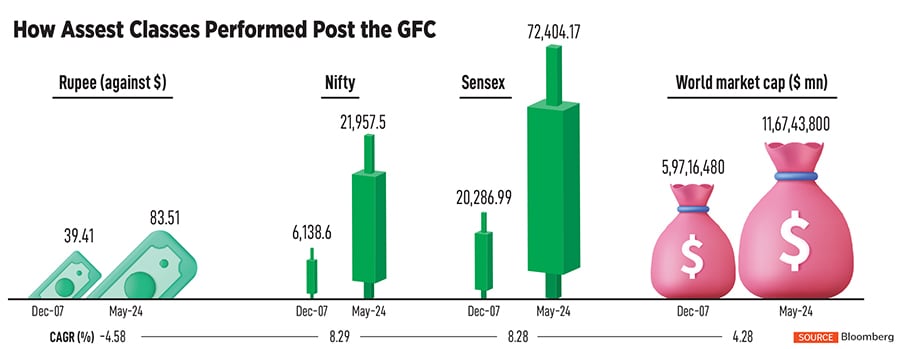

Forbes India @15: Have the 2008 recession wounds healed?

The global financial crisis 15 years ago left an indelible trauma for corporates and all asset classes. Global central banks reacted with soft monetary policies and stricter regulations. Have the woun

The global financial crisis was mostly tirggered by the collapse of the Lehman Brothers in 2007-08, wiping out an estimated $10 trillion economic output

Image: Getty Images

Advertisement

Regulation and more regulation—that’s how economies around the world reacted to the global financial crisis (GFC), mostly triggered by the Lehman Brothers collapse in 2007-08, which wiped off an estimated $10 trillion economic output.

The largest bankruptcy filing in the US crashed stock markets worldwide, punctured the confidence of global central banks and corporates, following which the US Federal Reserve injected liquidity to contain the financial shock. The recovery was slow. The global financial crisis—also referred to as the great recession—brought severe and permanent economic changes to the world.

“While the credit rating regulations were brought in (which India to her credit had in place before the crisis), there was more scrutiny over operations—separated ratings agencies from advisory services—to ensure there was no conflict of interest," says Madan Sabnavis, chief economist, Bank of Baroda.

India was less affected by the crisis as regulators were cautious about financial engineering. “Products like credit default swap (CDS), collateralised debt obligations (CDO), mortgage-backed security (MBS) were in their infancy then," adds Sabnavis.

Companies became more conservative in their capital structure and spends. “The Insolvency and Bankruptcy Code (IBC) is an outcome of the misallocation of capital that happened in the previous decade and the urgent need to find a way to help banks resolve non-performing assets (NPAs) and bring productive assets back...the government resorted to fiscal stimulus, resulting in high inflation and a weakening of the sovereign, reflecting in a sharp tumble in the currency," says Vetri Subramaniam, chief investment officer, UTI AMC.

For Indian corporates, the struggle continued even when interest rates by most global central banks had softened. With the deepening of the crisis, the Federal Open Market Committee (FOMC) accelerated its interest rate cuts, taking the rate to a target range of 0 to 25 basis points, by end of 2008. However, only a few companies took bolder steps and rejigged their business strategies.

According to Saurabh Mukherjea, founder and chief investment officer, Marcellus Investment Managers, as share prices corrected by 30 to 80 percent in 2008 and debt markets froze, there were mainly three sorts of responses from India Inc.

First, smart capital allocators like Shiv Nadar of HCL Tech used the surge in risk aversion to buy attractive assets at bargain basement valuations. HCL Tech acquired UK-based SAP consulting company Axon Group at a discounted valuation in 2008 and went on to build a lucrative franchise around it. Second, indebted companies in sectors like power, infra, metals, real estate etc froze expansion and tried to absorb what was going on. Third, companies with strong balance sheets continued to grow their franchises at a rapid rate through 2008.

Besides regulation, inspection and scrutiny, one key lesson the global financial crisis taught was separating credit rating agencies rating from advisory business, says Sabnavis. Also, commercial banks that deal with deposit holders’ money should not be venturing into high-risk derivatives and if they do, a regulatory framework has to be in place.

Some asset classes that used to be popular pre-crisis never regained their popularity. For instance, convertibles. “Other asset classes returned but in a different shape. For instance, pre-global financial crisis, low quality Indian companies with patchy corporate governance track records were able to issue bonds both in India and abroad," says Mukherjea.

Following the crisis, only the bluest of blue-chip Indian companies were able to raise corporate bonds. As a result, all of these borrowers who were locked out of the bond market had to go to Indian banks for debt, which resulted in banks building huge corporate lending books between 2009 and 2013. Much of that corporate lending turned sour through 2013-16, says Mukherjea.

On the positive side, the economic meltdown also taught Indian equity investors that best bargains can be found when Indian stock markets crash due to a global catastrophe. “Without living through the global financial crisis, I don’t think we could have successfully navigated the Covid panic," Mukherjea adds.

For Indian corporates, the struggle continued even when interest rates by most global central banks had softened. With the deepening of the crisis, the Federal Open Market Committee (FOMC) accelerated its interest rate cuts, taking the rate to a target range of 0 to 25 basis points, by end of 2008. However, only a few companies took bolder steps and rejigged their business strategies.

For Indian corporates, the struggle continued even when interest rates by most global central banks had softened. With the deepening of the crisis, the Federal Open Market Committee (FOMC) accelerated its interest rate cuts, taking the rate to a target range of 0 to 25 basis points, by end of 2008. However, only a few companies took bolder steps and rejigged their business strategies.