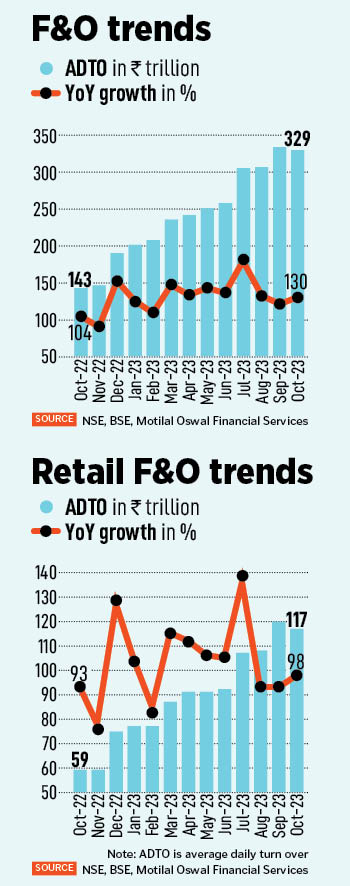

Surprisingly, despite steep losses in equity F&O, the number of retail or individual traders in the segment is ballooning. Derivative trading has stripped cash market volumes with a phenomenal rise in the number of active derivatives traders. In October, the total average daily turnover (ADTO) in the F&O segment was Rs 329 trillion, surging 130 percent from same month last year, at Rs 143 trillion, shows analysis by Motilal Oswal Financial Services, based on data from NSE and BSE. This year so far, ADTO in the F&O segment was the highest in September, at Rs 334 trillion, up 121 percent year-on-year (y-o-y).

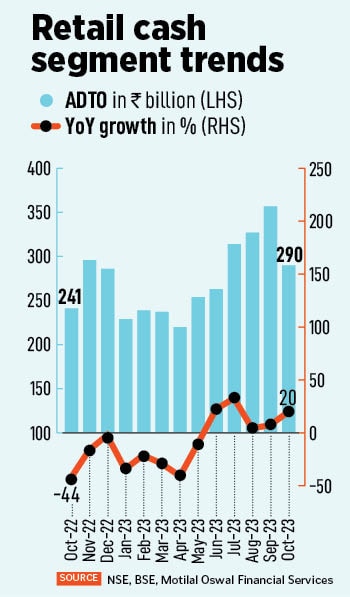

However, the market regulator is concerned by the exponential surge of retail traders in the F&O segment, which is considered risky and often loss-making. In October, retail ADTO in the F&O segment was Rs 117 trillion, rising 98 percent y-o-y, whereas retail ADTO in the cash market was only Rs 290 billion, up merely 20 percent y-o-y. Though retail ADTO in the cash market segment was Rs 357 billion in September, it is comparatively small to the Rs 120 trillion in the F&O segment.

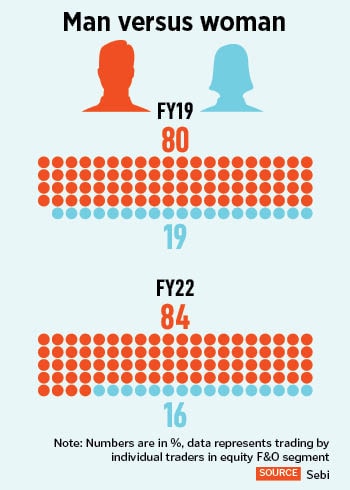

According to a study by the Securities and Exchange Board of India (Sebi), the total number of unique individual traders who traded in the equity F&O segment was 45.2 lakh in FY22, growing from 7.1 lakh in FY19. This is a significant increase of more than 500 percent in FY22 as compared to FY19.

Human greed! And a few regulation changes in F&O trading that have made the segment attractive for all varieties of traders.

Many factors can be attributed for the high volume in the F&O segment by retail traders, says Deepak Jasani, retail research head, HDFC Securities, citing gambling instincts and human greed as driving factors. “It is human nature to be aspirational and desire to achieve monetary goals faster, just like in gambling. Also, lower ticket size of lots in derivative trading and low premium for OTM calls/puts on expiry days has made this segment attractive among retail participants," he explains.

Introduction of weekly expiry and zero days to expiration (0DTE) are a few other factors, he mentions, that have driven high volume of trade in the F&O segment. 0DTE refers to options contracts that are expiring on the same trading day. This is in contrast to regular options contracts that may have days, weeks, or even months until expiration.

![]() Shorter durations indicate that the options market is shifting from hedging to speculation. The Collins Dictionary defines derivatives as contracts, such as options or futures contracts, whose value is contingent on the value of the underlying securities or commodities. Originally designed as a tool for hedging risk, derivatives are now a tool for taking risk.

Shorter durations indicate that the options market is shifting from hedging to speculation. The Collins Dictionary defines derivatives as contracts, such as options or futures contracts, whose value is contingent on the value of the underlying securities or commodities. Originally designed as a tool for hedging risk, derivatives are now a tool for taking risk.

Change in contract structure, leverage combined with the ease of onboarding, and interfaces of trading apps have triggered gamification of this market, says Ashish Gupta, CIO, Axis Mutual Fund. As a result, he adds, the number of active derivatives traders has increased eightfold from less than half a million in 2019 to 4 million.

Index options are typically the preferred choice, constituting 99 percent of derivative volumes and, within this, accounts for 95 percent of weekly trades. The effective leverage on an index option on expiry day is 500 times, which is luring retail traders. A Rs 2,000 option allows Rs 10 lakh exposure, and these are largely speculative bets a retailer holds as options, on average for just 30 minutes.

“What"s driving retailers is the introduction of weekly expiry by other indices as that provides opportunity to retail participants daily. Secondly, the weekly options premium as compared to the monthly options is less, hence that has attracted many retail traders. Also, as the margin requirement has reduced drastically, the bet size has also increased," says Jay Thakkar, head, Alternate Research, Capital Market Strategy, Sharekhan by BNP Paribas.

Others concur that changes in the expiry date and nature of products in the F&O segment have made it attractive. Rishi Kohli, managing partner & CIO, Hedge Fund Strategies, InCred Alternative Investments, explains there are a mix of reasons for the growth of F&O trading volume, such as rise of online trading, especially driven by people having spare time during the Covid-19 pandemic and dabbling in trading through online brokers and platforms, introduction of weekly options first on BankNifty, then Nifty indices, and in recent past on FinNifty, MidcapNifty and Sensex indices.

![]() Also, trading platforms and online brokers like Zerodha and Upstox have helped grow the market, where tools for simulation on F&O strategies is provided to retail investors who never had the chance earlier to dabble in such stuff, which was the exclusive space for institutional players.

Also, trading platforms and online brokers like Zerodha and Upstox have helped grow the market, where tools for simulation on F&O strategies is provided to retail investors who never had the chance earlier to dabble in such stuff, which was the exclusive space for institutional players.

Kohli explains. Weekly options have been the major reason and now index expiry is on each day of the week with MidcapNifty on Monday, FinNifty on Tuesday, BankNifty on Wednesday, Nifty on Thursday and Sensex on Friday. So, for a lot of retail traders who buy options, when they trade on expiry day their potential to make 10 times of their capital is what is attractive, as that opportunity is there on every day of the week. For option sellers who are typically institutions and prop traders, daily and weekly expiring options are much better than monthly options, which used to be the only option duration till a few years back.

Typically, buyers of options get attracted due to daily expiries where the potential to make multiple times their capital is very attractive, but as that happens most retail traders end up losing most of the time. Inexperienced retail traders who sell options may not have the expertise or knowledge to hedge or manage risks, so a sharp move ends up in sharp losses for them.

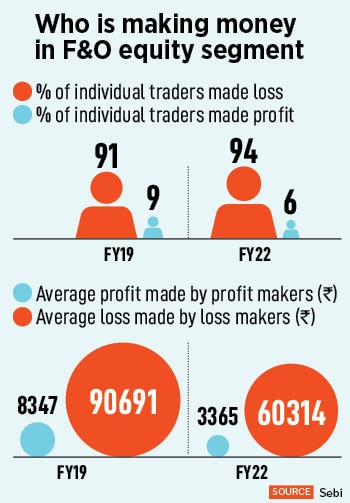

According to a study by Sebi, in FY22 only 11 percent of individual traders in the equity F&O segment made profits, with an average profit of Rs 1.5 lakh. The percentage went down to 10 percent for active traders, though the average profit made by them went up to Rs 1.9 lakh during the same period.

In FY22, 89 percent of individual traders in the equity F&O segment incurred losses, with an average loss of Rs 1.1 lakh in FY22, whereas 90 percent of active traders incurred average losses of Rs 1.25 lakh in the same period.

“Mainly, retail traders are buyers of options and not sellers. The probability of winning in options buying is 33 percent and with the increased number of trades due to lower premiums the probability of winning in options turning in the money decreases even more. Hence nine out of 10 trades are in losses," Thakkar says.

There are two types of risks: First, as an option buyer if the retailers don"t put stop-loss, then their entire capital invested for option buying can become zero, as many options expire worthless. Secondly, as an option seller the gain is limited to option premium credited but losses are unlimited if the position goes in the opposite direction, hence, in the absence of stop-loss it can result in unlimited losses, Thakkar adds.

![]() For groups of active traders, on average, loss makers registered net trading loss close to Rs 50,000 in FY22 while average loss of a loss maker was over 15 times the average profit by a profit maker in the same year, shows the Sebi study. The percentage of loss makers was marginally lower at 83 percent for non-active individual traders in FY22, compared to 76 percent in FY19.

For groups of active traders, on average, loss makers registered net trading loss close to Rs 50,000 in FY22 while average loss of a loss maker was over 15 times the average profit by a profit maker in the same year, shows the Sebi study. The percentage of loss makers was marginally lower at 83 percent for non-active individual traders in FY22, compared to 76 percent in FY19.

“Option sellers need to understand that even if they make money 90 percent of the time in an option selling strategy but lose 10 times of that amount the remaining 10 times, they will end up being losers. The overall payoffs have to be understood rather than just winning percentage of trades, which is what naà¯ve traders focus on," Kohli elaborates.

Similarly, option buyers who tend to buy deep OTM options to get large, leveraged payoffs need to understand that the big moves happen only five to 10 percent of the time and, even then, if one is too far OTM then the gains would not make up for the losses in the rest of the times. According to him, both types of retail traders need to understand these statistics, probabilities and payoffs apart from doing better risk management and position sizing.

Handle with care!

According to Chandan Taparia, head, Derivatives & Technical Research, Motilal Oswal Financial Services, retail investors are attracted to this segment of trade because it has the potential to recover and make consistent money if certain rules work and they can manage their risk and position sizing. “Many retail investors come with revenge," he adds.

However, the pulsating rise of retail traders in the F&O segment is making the Sebi chief confused. “I must admit, I am always a little confused and surprised as to why people continue to do that [bet in futures and options], knowing that the odds are not in their favour at all," said Madhabi Puri Buch, Sebi chief, at an event.

![]() Buch sounded cautious that there is a 90 percent chance of investors losing money in the F&O segment, “but we also know, and the data shows us, that if you take a long-term view of the market, and if you invest with a long-term perspective, you will rarely go wrong".

Buch sounded cautious that there is a 90 percent chance of investors losing money in the F&O segment, “but we also know, and the data shows us, that if you take a long-term view of the market, and if you invest with a long-term perspective, you will rarely go wrong".

On another occasion, Ashish Chauhan, MD and CEO, NSE, also warned that trading in derivatives should be avoided by retail investors due to the high amount of risk involved in the segment. The irony is, higher volume of F&O trade transactions benefit few entities such as exchanges, Sebi, discount brokers and government on items like turnover fees, GST, securities transaction tax (STT) and stamp duty.

“All the warnings and caution to retail investors by NSE and Sebi just seem like lip service," says an industry veteran who did not want to be named. The person explains that new upfront margins for all-cash trades were introduced by the regulator in 2020, which itself made trading in that segment expensive, indirectly driving a lot of retail participants to the F&O segment.

“Why has Sebi not introduced or implemented any regulations to curb high volume trading in the F&O segment by retail investors if it is so risky?" asks industry veteran. The market regulator, NSE, government and brokerage firms get richer on every trade on the F&O segment irrespective of the trader making profits or losses. For instance, Sebi charges turnover fees, etc on every trade conducted in the segment. So, higher the volume and turnover, higher the revenue for these entities, the person explains.

Thakkar adds that losses in the F&O segment can be curbed by placing stop-losses, hedging the strategy, maintaining trading discipline and avoiding compulsive trading. “With increase in the number of participants in the market, volumes in the F&O segment are likely to increase. If all of these indices do even 50 to 75 percent volumes of what Nifty and BankNifty do, then too overall volumes in the F&O segment is likely to increase," he says.

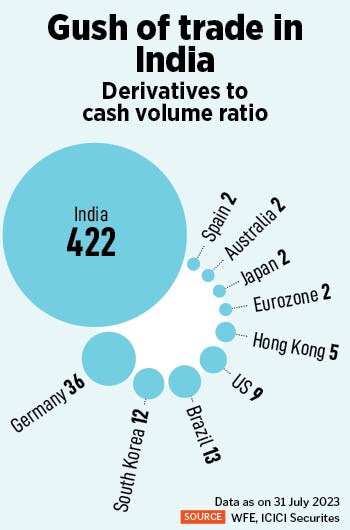

![]() The growth of the derivatives market is not unique to India. In most markets today derivatives volumes outstrip cash market volumes. In the US, derivatives account for 70 percent of traded volumes, compared to 99.6 percent currently for the Indian markets. A key reason for attractiveness of the product is the embedded leverage, where only a fraction of the notional value is needed to transact, which ends up magnifying the potential gains (as well as losses) for the participant.

The growth of the derivatives market is not unique to India. In most markets today derivatives volumes outstrip cash market volumes. In the US, derivatives account for 70 percent of traded volumes, compared to 99.6 percent currently for the Indian markets. A key reason for attractiveness of the product is the embedded leverage, where only a fraction of the notional value is needed to transact, which ends up magnifying the potential gains (as well as losses) for the participant.

Of the more than 5,000 companies listed in India, derivatives contracts are available for 193 stocks and indices. For these, there are 46,000 individual contracts available at any point spanning products (futures, options), tenor and strike prices. Index options reign supreme, accounting for 98 percent of total derivative volumes.

According to Gupta, at a system level, derivatives have a useful economic function, wherein risks can be transferred from those who do not want it to those who want it. Another useful function that the product provides is that of additional liquidity in the market, beyond what is available in the cash markets. “The outsized derivatives market though can itself be a source of additional macro and market risk, we have seen this in global cases with CDS and derivatives contracts. Black swan events and resultant spikes in volatility in particular can drive exaggerated moves in stock prices and result in market dislocation," he elaborates.

Shorter durations indicate that the options market is shifting from hedging to speculation. The Collins Dictionary defines derivatives as contracts, such as options or futures contracts, whose value is contingent on the value of the underlying securities or commodities. Originally designed as a tool for hedging risk, derivatives are now a tool for taking risk.

Shorter durations indicate that the options market is shifting from hedging to speculation. The Collins Dictionary defines derivatives as contracts, such as options or futures contracts, whose value is contingent on the value of the underlying securities or commodities. Originally designed as a tool for hedging risk, derivatives are now a tool for taking risk. Also, trading platforms and online brokers like Zerodha and Upstox have helped grow the market, where tools for simulation on F&O strategies is provided to retail investors who never had the chance earlier to dabble in such stuff, which was the exclusive space for institutional players.

Also, trading platforms and online brokers like Zerodha and Upstox have helped grow the market, where tools for simulation on F&O strategies is provided to retail investors who never had the chance earlier to dabble in such stuff, which was the exclusive space for institutional players. For groups of active traders, on average, loss makers registered net trading loss close to Rs 50,000 in FY22 while average loss of a loss maker was over 15 times the average profit by a profit maker in the same year, shows the Sebi study. The percentage of loss makers was marginally lower at 83 percent for non-active individual traders in FY22, compared to 76 percent in FY19.

For groups of active traders, on average, loss makers registered net trading loss close to Rs 50,000 in FY22 while average loss of a loss maker was over 15 times the average profit by a profit maker in the same year, shows the Sebi study. The percentage of loss makers was marginally lower at 83 percent for non-active individual traders in FY22, compared to 76 percent in FY19. Buch sounded cautious that there is a 90 percent chance of investors losing money in the F&O segment, “but we also know, and the data shows us, that if you take a long-term view of the market, and if you invest with a long-term perspective, you will rarely go wrong".

Buch sounded cautious that there is a 90 percent chance of investors losing money in the F&O segment, “but we also know, and the data shows us, that if you take a long-term view of the market, and if you invest with a long-term perspective, you will rarely go wrong". The growth of the derivatives market is not unique to India. In most markets today derivatives volumes outstrip cash market volumes. In the US, derivatives account for 70 percent of traded volumes, compared to 99.6 percent currently for the Indian markets. A key reason for attractiveness of the product is the embedded leverage, where only a fraction of the notional value is needed to transact, which ends up magnifying the potential gains (as well as losses) for the participant.

The growth of the derivatives market is not unique to India. In most markets today derivatives volumes outstrip cash market volumes. In the US, derivatives account for 70 percent of traded volumes, compared to 99.6 percent currently for the Indian markets. A key reason for attractiveness of the product is the embedded leverage, where only a fraction of the notional value is needed to transact, which ends up magnifying the potential gains (as well as losses) for the participant.