What can kick corporate investments out of a slowdown?

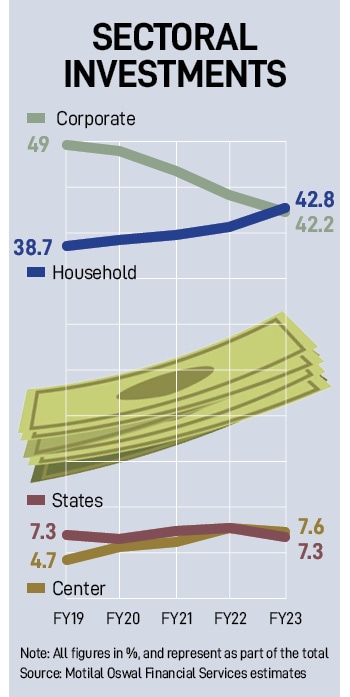

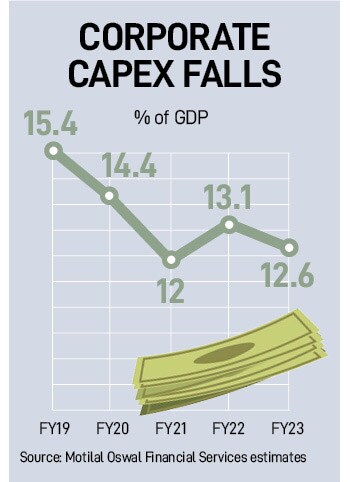

Corporate investments grew 11 percent year-on-year in FY23, while their share fell to 42.2 percent of total investments, the lowest in 19 years. Corporate investments fell to 12.6 percent of GDP in FY

The companies are also possibly waiting for further clarity in the economic policies and business environment before loosening their purse strings as the country is likely to go to polls in May 2024. Image: Anindito Mukherjee/Bloomberg via Getty Images

Advertisement

Even as the perils of a pandemic are gradually ebbing off, companies are yet to fire up their spends in expansion plans. Perhaps lack of growth opportunities or simply limited supply of funds could be the reasons for slow corporate capex in India. The companies are also possibly waiting for further clarity in the economic policies and business environment before loosening their purse strings as the country is likely to go to polls in May 2024.

“Given that elections are likely in 2024, companies will be discreet. Expectations of rates coming down will also defer their plans of investments. Governments at both Centre and states are expected to meet their capex targets and hence sustain backward linkages," says Madan Sabnavis, chief economist, Bank of Baroda.

For the year ending March 2023, corporate investment was the lowest in 19 years. Corporate investments grew 11 percent year-on-year in FY23, while its share fell to 42.2 percent of total investments, the lowest in 19 years, according to data analysis by Motilal Oswal Financial Services. The analysis is based on data covering 13 monthly and six quarterly indicators across 27 states.

Total investments were at 31 percent of GDP in FY23, almost similar to FY22 and the pre-Covid period in FY20, the analysis showed. In FY22, total investment was 31.2 percent of GDP, as against 28.8 percent in FY21 and 30.1 percent of GDP in FY20. Although India’s investment rate was broadly unchanged last year, corporate investments fell to 12.6 percent of GDP in FY23, the lowest since FY04.

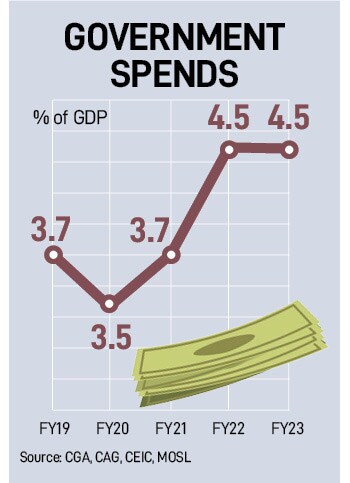

Government investments grew 14.5 percent YoY in FY23, implying an average growth of 14 percent in the last four years (FY20- FY23). This is slightly better than 13 percent average growth in the previous four years (FY16-FY19). It stood at 4.5 percent of GDP in FY23, the same as in FY22, equally split between the Centre and the states.

“Government capex was 4.5 percent of GDP last year, unchanged compared to FY22. The government thus accounted for 15 percent of total investments in the country, like in FY22. The Centre’s capex was higher than the states’ for the second consecutive year since FY05," Nikhil Gupta, chief economist, Motilal Oswal Financial Services explains.

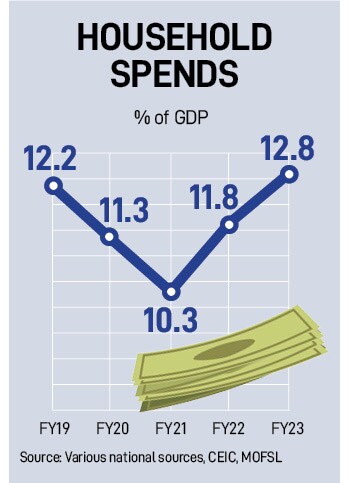

However, what is encouraging is household investments in the fiscal year 2023. The share of household increased to 42.8 percent of total investments in FY23, the highest in a decade and higher than that of the corporate sector, for the first time in 18 years. Household investments, including residential real estate, are estimated to have grown 24 percent YoY in FY23, according to the analysis. This follows a 30 percent (YoY) growth in FY22.

“Overall, a strong residential property market holds the potential to boost economic activity and generally a reversal in this sector lasts for a few years. However, weak income growth, high interest rates, fading base effect, and high economic uncertainties create vulnerabilities about its durability. The corporate capex, at the same time, is certainly still lagging," Gupta adds.

Signs of revival in private capex were most prominently visible in Q4FY23 in sectors like automobiles and data centres, say analysts. “The benefits of the central government’s record high capex allocation in FY24 would accrue to companies in sectors like infrastructure and capital goods, especially cement," says Hitesh Suvarna, analyst, JM Financial. The Union Budget had steeply increased the capital expenditure outlay by 37.4 percent in FY24 to a whopping Rs 10 lakh crore from Rs 7.28 lakh crore in FY23.

A few private companies have increased their capex plans for FY24 going forward. After March quarter earnings, Tata Motors has said it has set an annual capex of Rs 2,500 crore for its commercial vehicle business, an annual capex of Rs 30,000 crore for internal combustion (ICE) engine passenger vehicles business segment and a cumulative capex of $2 billion until FY27 for product development and architectures in the electric vehicle segment. For FY24, Tata Steel has planned a capex of Rs 16,000 crore. Tata Steel has incurred a capex of Rs 4,396 crore during Q4FY23 and Rs 14,142 crore for FY23.

Sabnavis adds that private investment has been more sector specific and is not broad-based and has been concentrated in sectors related to capex of government. “This includes steel, cement, chemicals, electrical cables etc. These get linked to government spending on roads, railways, urban development," he says adding that on the private side housing has contributed to private investment in these sectors. “For consumer-based industries there is still excess capacity and stagnant demand. The same picture is reflected in the sectoral credit matrix and funds raised in corporate bond market. In my view I don"t think there will be major change in FY24. Reason is that high inflation will come in way of consumption. Further pent-up demand unlikely to sustain. Hence private investment [is] to be at best stable," Sabnavis says.

Moody’s Indian affiliate ICRA expects private and government capital expenditure (capex) to surge amid the large size of new projects, improving capacity utilisation levels, production-linked incentive (PLI) schemes and government initiatives towards clean energy. ICRA expects the annual capex from PLI schemes to cross Rs 1 trillion in fiscal 2024 and may peak at Rs 1.7 trillion in fiscal 2026. Hence, fiscal 2024 could be an inflection point for a surge in India’s manufacturing capex, ICRA feels.

“India Inc’s reliance on borrowings will remain high due to multiple reasons, such as an increase in the scale of operations requiring higher working capital capex spending in certain sectors and supply chain uncertainties leading to higher inventory levels. However, we expect the credit profile of India Inc to remain stable, supported by a commensurate improvement in earnings," says Shamsher Dewan, senior vice president and group head, corporate ratings, ICRA.

Others concur. Fitch Ratings believes India’s structural demand visibility, supply side measures such as growing infrastructure spend and PLI schemes by the government, as well as healthier corporate and bank balance sheets will drive capex up for the corporate sector over the medium term. “We believe Indian corporates" deleveraged balance sheets and improving profitability from FY23 lows improve their ability to invest. In addition, the capex is backed by higher internal accruals, given the lower capex/EBITDA ratio, and is hence more sustainable. Concurrently, falling impaired-loan ratios and credit costs have improved the financial health of the Indian banking sector, enabling it to support corporates’ funding needs," Fitch says.

Upasana Chachra, chief India economist, Morgan Stanley also agrees that structural reforms implemented over the last few years will ensure a sustained revival of the capex cycle. "Policymakers have maintained their focus on supply-side reforms with reductions in corporate income tax, introduction of tax incentives encouraging new manufacturing sector investment, and increase in public capex to 18-year highs," she adds.

However, Nomura economists feel that weak global demand, much global uncertainty, elevated real rates and a slowdown in tax collections (especially in second half FY24) are likely to weigh on aggregate capex.

“Government capex was 4.5 percent of GDP last year, unchanged compared to FY22. The government thus accounted for 15 percent of total investments in the country, like in FY22. The Centre’s capex was higher than the states’ for the second consecutive year since FY05," Nikhil Gupta, chief economist, Motilal Oswal Financial Services explains.

“Government capex was 4.5 percent of GDP last year, unchanged compared to FY22. The government thus accounted for 15 percent of total investments in the country, like in FY22. The Centre’s capex was higher than the states’ for the second consecutive year since FY05," Nikhil Gupta, chief economist, Motilal Oswal Financial Services explains. A few private companies have increased their capex plans for FY24 going forward. After March quarter earnings, Tata Motors has said it has set an annual capex of Rs 2,500 crore for its commercial vehicle business, an annual capex of Rs 30,000 crore for internal combustion (ICE) engine passenger vehicles business segment and a cumulative capex of $2 billion until FY27 for product development and architectures in the electric vehicle segment. For FY24, Tata Steel has planned a capex of Rs 16,000 crore. Tata Steel has incurred a capex of Rs 4,396 crore during Q4FY23 and Rs 14,142 crore for FY23.

A few private companies have increased their capex plans for FY24 going forward. After March quarter earnings, Tata Motors has said it has set an annual capex of Rs 2,500 crore for its commercial vehicle business, an annual capex of Rs 30,000 crore for internal combustion (ICE) engine passenger vehicles business segment and a cumulative capex of $2 billion until FY27 for product development and architectures in the electric vehicle segment. For FY24, Tata Steel has planned a capex of Rs 16,000 crore. Tata Steel has incurred a capex of Rs 4,396 crore during Q4FY23 and Rs 14,142 crore for FY23. Moody’s Indian affiliate ICRA expects private and government capital expenditure (capex) to surge amid the large size of new projects, improving capacity utilisation levels, production-linked incentive (PLI) schemes and government initiatives towards clean energy. ICRA expects the annual capex from PLI schemes to cross Rs 1 trillion in fiscal 2024 and may peak at Rs 1.7 trillion in fiscal 2026. Hence, fiscal 2024 could be an inflection point for a surge in India’s manufacturing capex, ICRA feels.

Moody’s Indian affiliate ICRA expects private and government capital expenditure (capex) to surge amid the large size of new projects, improving capacity utilisation levels, production-linked incentive (PLI) schemes and government initiatives towards clean energy. ICRA expects the annual capex from PLI schemes to cross Rs 1 trillion in fiscal 2024 and may peak at Rs 1.7 trillion in fiscal 2026. Hence, fiscal 2024 could be an inflection point for a surge in India’s manufacturing capex, ICRA feels. Others concur. Fitch Ratings believes India’s structural demand visibility, supply side measures such as growing infrastructure spend and PLI schemes by the government, as well as healthier corporate and bank balance sheets will drive capex up for the corporate sector over the medium term. “We believe Indian corporates" deleveraged balance sheets and improving profitability from FY23 lows improve their ability to invest. In addition, the capex is backed by higher internal accruals, given the lower capex/EBITDA ratio, and is hence more sustainable. Concurrently, falling impaired-loan ratios and credit costs have improved the financial health of the Indian banking sector, enabling it to support corporates’ funding needs," Fitch says.

Others concur. Fitch Ratings believes India’s structural demand visibility, supply side measures such as growing infrastructure spend and PLI schemes by the government, as well as healthier corporate and bank balance sheets will drive capex up for the corporate sector over the medium term. “We believe Indian corporates" deleveraged balance sheets and improving profitability from FY23 lows improve their ability to invest. In addition, the capex is backed by higher internal accruals, given the lower capex/EBITDA ratio, and is hence more sustainable. Concurrently, falling impaired-loan ratios and credit costs have improved the financial health of the Indian banking sector, enabling it to support corporates’ funding needs," Fitch says.