For millions of salaried workers in India, retirement savings are an integral part of monthly financial planning. With fixed contributions from employers and employees, the system ensures financial security long after active employment ends.

The Employees’ Provident Fund Organisation (EPFO) plays a central role in managing provident fund contributions, pension schemes, and insurance benefits for formal sector employees. In December 2024 alone, the EPFO enrolled over 8 lakh new subscribers. Interestingly, the 18-25 age group comprised over half (4.85 lakh) of this figure, reflecting a growing job market and increased awareness of employee benefits.

With growing demand for more seamless digital experiences, the EPFO 3.0 launch marks a significant milestone in how PF services are delivered. In this post, we’ll discuss EPFO 3.0, its new upgrades, and the risks you should be aware of.

What is EPFO 3.0?

EPFO 3.0 is a significant step by the Ministry of Labour and Employment, India, to enhance the efficiency and accessibility of its services for all. Expected to launch this month - June 2025 - this update focuses on streamlining processes such as PF withdrawal and EPF claim settlements, with reduced paperwork and shorter wait times.

You’ll be able to check your PF balance on the UPI platform and transfer money to other bank accounts. You can also update your EPF accounts through OTP verification in simple steps. The goal is to simplify fund access and be more responsive to real-life needs, especially in urgent situations.

What are the new changes in the EPFO 3.0?

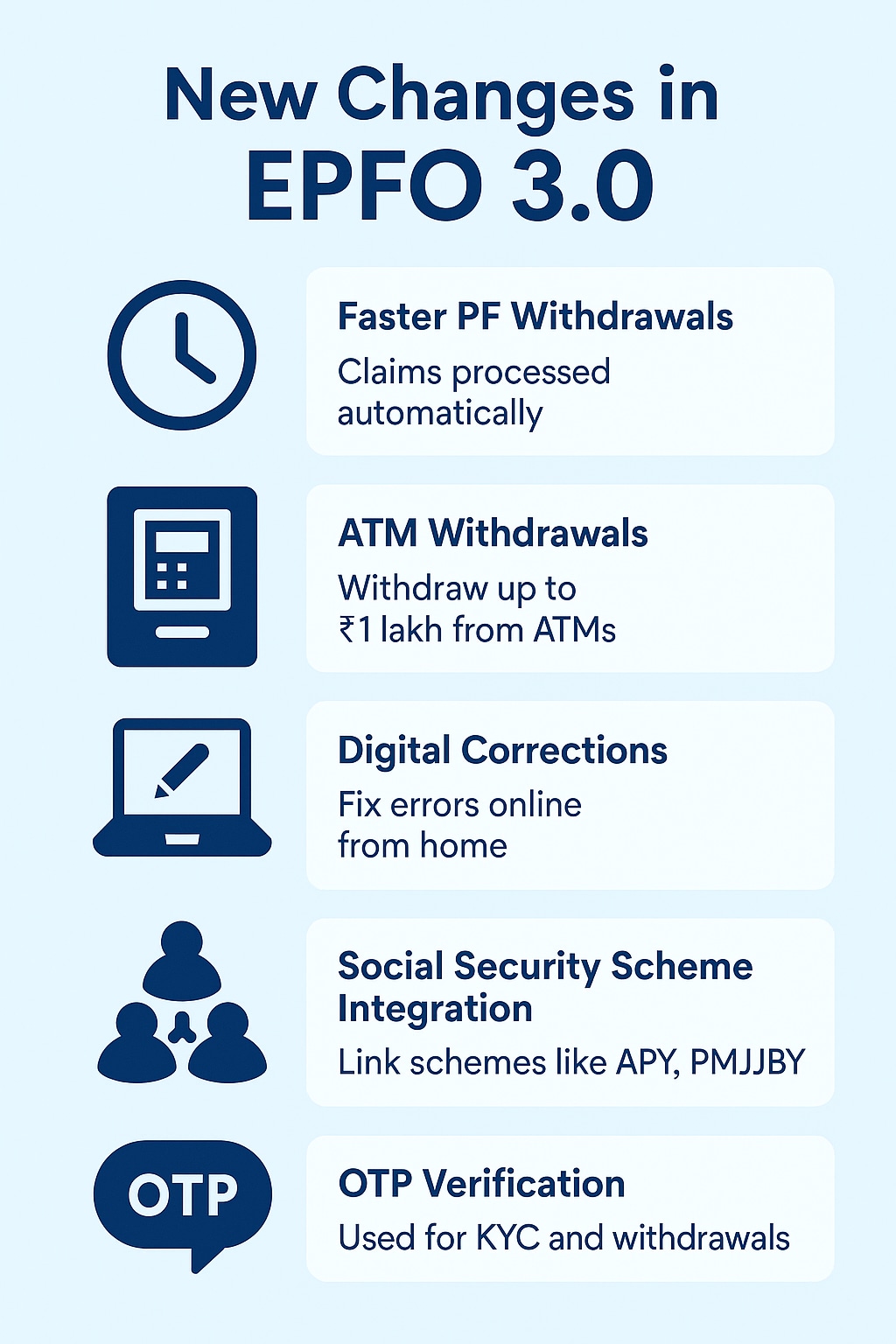

The EPFO 3.0 launch introduces a range of practical updates designed to improve the experience. Here’s what’s changing:

Faster PF withdrawals: Now, claims will be processed automatically, reducing manual work and waiting periods.

ATM withdrawals: Once your EPF claim is approved, you can withdraw up to ₹1 lakh directly from an ATM, similar to how you access a bank account.

Digital corrections: You can fix errors online from home without any additional form requirements, whether it"s a name mismatch or incorrect bank details.

Social security scheme integration: EPFO is exploring ways to link schemes like Atal Pension Yojana and Pradhan Mantri Jeevan Bima Yojana, making benefits more accessible for employees in the unorganised and informal sectors.

OTP verification: From updating KYC to making withdrawals, an OTP replaces lengthy forms, making processes quicker and more secure.

Eligibility criteria for PF withdrawals

The EPFO 3.0 launch outlines specific criteria for PF withdrawals. Ensure that these criteria are met successfully:

Your Universal Account Number (UAN) should be active.

Your mobile number should be working, accessible, and linked to the UAN.

KYC documents (ID and address proof) should be linked to your UAN. This includes your Aadhaar, PAN, bank account number, and IFSC code.

A cancelled cheque that clearly shows your account number and IFSC number.

Once eligible, you will be issued a PF withdrawal card, which will be linked to your EPF account. This card will enable ATM withdrawals, and you’ll also be able to transfer funds via UPI directly to your bank.

Withdrawal limits depend on your reason for withdrawal and years of service. For example, members can withdraw up to 90 per cent for buying a house after five years, 50 per cent for education or marriage after seven years, and up to 90 per cent a year before retirement. Medical emergencies follow a different cap on limits.

What are the potential risks involved?

As convenience increases, so does the need for caution. While the EPFO 3.0 launch promises a smoother experience for PF withdrawals through UPI and ATMs, it has its fair share of risks.

One major concern is PIN theft. Fraudsters or scammers may install hidden cameras near ATMs to capture your keypad activity and misuse your account.

Skimming devices are another threat. These small, often unnoticeable tools are placed over ATM card slots to steal your details. They can be hard to detect and may lead to identity theft or unauthorised transactions.

There’s also the chance of software glitches, such as failed transactions, network lags, or even double debits. These common technical issues can often delay your access to funds.

With the launch of EPFO 3.0, staying alert while withdrawing money or updating your EPF claim details is more important than ever.

Frequently asked questions (FAQs)

1. How long can an employee continue their EPF membership?

An employee can continue employee provident fund (EPF) membership indefinitely, but if no contributions are made for 3 years, the account stops earning interest beyond that period.

2. Is there a time limit for withdrawing the PF amount?

Yes. In case of resignation (not retirement), you must wait 2 months before becoming eligible to withdraw your PF amount. If you remain employed, you can do partial withdrawals under exceptional circumstances.

3. What is EPFO pension?

The EPFO pension, under the Employee Pension Scheme (EPS), provides a monthly post-retirement income. It’s funded jointly by the employer and employee to ensure financial support after retirement.