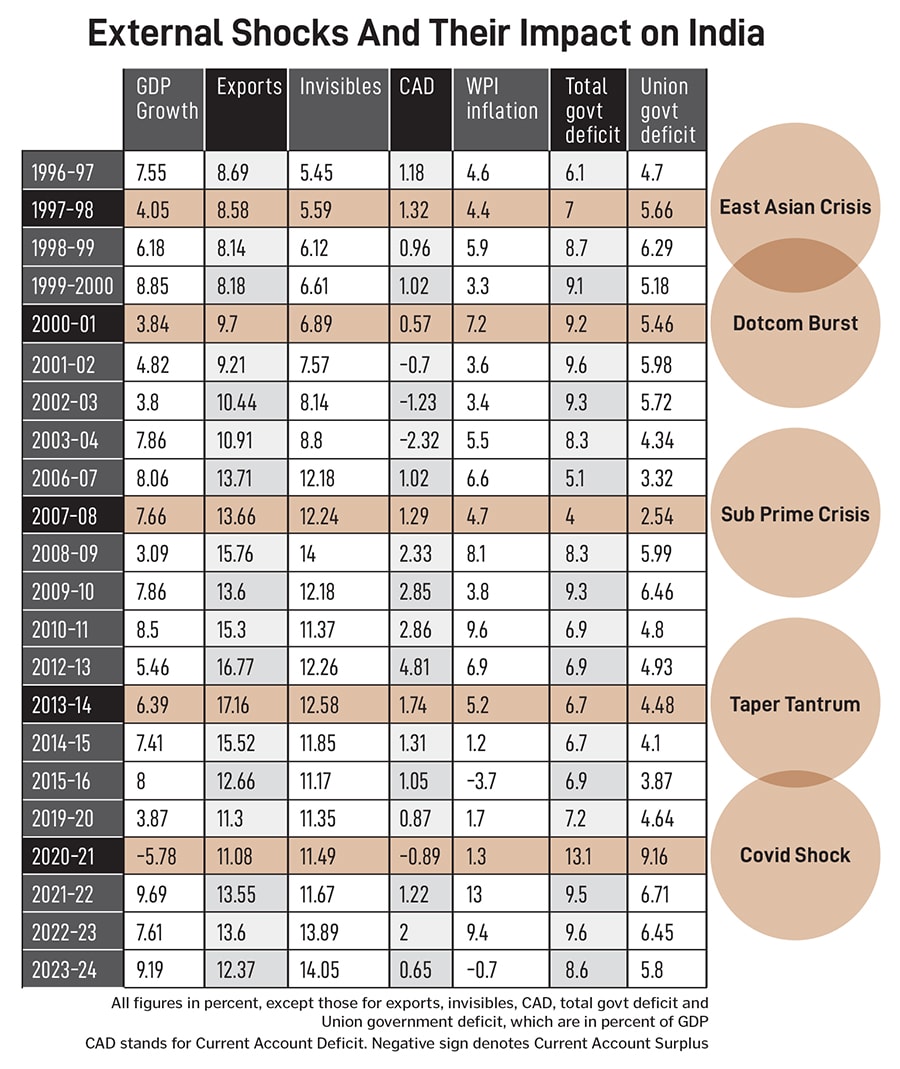

The dotcom bust in 2000, immediately after the tech boom of the late 1990s, played havoc with many developed markets and the fortunes of several technology companies as the overall demand for technology solutions fell. The impact on the Indian stock market and the economy was far less severe as India’s exposure to technology stocks was relatively limited. Proactive regulation also helped. Though the Securities and Exchange Board of India imposed temporary curbs on short selling and raised margin requirements to rein in speculative activity in the stock market, the Reserve Bank of India (RBI) intervened in both the money and foreign exchange markets to stabilise the rupee and adopted a cautious stance on the monetary policy front.

Such proactive interventions were aided by a government that came out with a fiscal stimulus package containing reduced tax rates on the one hand and increased infrastructure spending as also targeted subsidies on the other. India’s technology companies embarked on alternative business models by offering software as services.

The sub-prime crisis of 2007-08, or the North Atlantic Financial Crisis, was largely caused by unregulated lending to high-risk borrowers and against housing assets that were overvalued. India’s stock markets took a huge beating, with many big public offers of companies to raise capital falling by the wayside. India’s banking was relatively safe as its exposure to the US mortgage market was very limited. Even then, the RBI reduced interest rates and infused liquidity to bolster an economy, whose economic growth had more than halved in just about a year.

What made a big difference was the government’s fiscal response by way of reduced taxes, increased infrastructure investment, and relief measures for the rural economy.

The Taper Tantrum of 2013 was a temporary shock to the global and Indian markets. In the wake of the sub-prime crisis in 2008, the US Federal Reserve had rolled out a programme of buying bonds from the market, which led to an increase in liquidity and helped maintain the pace of economic activity. But in May 2013, Fed Chairman Ben Bernanke famously announced that at some point in time he would start tapering its bond purchase programme. This caused a panic reaction in the market. With the demand for US Treasury bonds falling, their prices fell, and their yields spiked as foreign money parked in emerging economies like India began flowing back to the US economy.

However, thanks to the many steps that the Indian government took in 2013-14, its overall impact turned out to be mild. Also, the threat issued by the Fed Reserve was not carried out. The Indian government took a series of advance steps by raising interest rates, placing curbs on gold imports to reduce their adverse impact on the current account, whose deficit had widened to an alarmingly high level of 4.8 per cent of gross domestic product (GDP). Additionally, the Indian government introduced a new scheme to attract deposits from non-resident Indians to cushion its foreign exchange reserves and tightened the fiscal policy. In the end, India managed to absorb the shocks that arose from the US Fed’s Taper Tantrum.

The fifth external shock came from the Covid pandemic. India’s GDP declined by about 6 percent, the first such decline in four decades. However, many steps were taken that helped the government manage its adverse impact on the economy. Apart from launching a country-wide vaccination programme, the government increased its investment in infrastructure and other industries to create jobs, provided financial relief to industries and released free foodgrain to all eligible Indians under the National Food Security Act. As the pandemic was contained, the economy bounced back.

Those challenges arose from well-defined causes and, therefore, were predictable. In short, the nature of the crisis was conventional and the Indian government’s response too was conventional.

How different is the Trump challenge?

The Trump challenges are not conventional. His policies are not predictable either. As a result, the challenges arising from them have become more complex and difficult to deal with only through traditional policy responses. Of course, the government’s current approach to conclude a bilateral trade agreement is on the right track. Going by the recent statements from senior officials of both the governments, it appears that an agreement would be ready to be signed by September-October 2025 around the time of the Quad summit in New Delhi. Sufficient care is also being taken to make sure that sectors whose opening up could become a cause for concern would be addressed through exemptions or exclusions. The US desire to strengthen its strategic alliance with India, as part of its plan to isolate China, will give rise to new opportunities for New Delhi. Apple Inc’s decision to increase its iPhone manufacturing capacity in India so that it could source all the phones needed for the US market from its Indian facilities is one such opportunity. The share of manufacturing in India’s GDP continues to languish at about 14 percent and this can certainly go up if more such strategic investments take place as a result of the Trump-induced disruption in the global economic order. But will that be enough?

India needs to commit itself to the idea of free trade and strive towards concluding free trade arrangements with important trading blocs and countries. The move to conclude a free trade agreement with the United Kingdom will be as necessary as a similar arrangement with the European Union. Along with fresh initiatives, the ones already in place with Australia, United Arab Emirates, the European Free Trade Association (EFTA) and Southeast Asian countries should be strengthened. In addition, the exercise that began a couple of years ago to bring down customs duty on a variety of goods at least to levels that prevailed before 2017-18 should be expedited. Tariffs began to be raised slowly just a year before the 2019 general elections. That was a policy mistake and the Trump initiatives on retaliatory tariff should be an opportunity to bring India’s tariffs down to those that prevail in most Southeast Asian countries—a goal that was set by many finance ministers in the past.

The linkage between trade and investment has always been strong. Global value chains play a major role in manufacturing goods across the world. India must plug itself into these not only through free trade arrangements, but also by encouraging investment in manufacturing in the country. That process can be facilitated if basic factor-market reforms are implemented without losing much time. Laws on land acquisition need to be relaxed to facilitate investment in projects, just as labour laws need to be made more flexible across the country.

The irony is that the Modi government took bold steps to reform both the land and labour laws but failed to make much headway. Land laws, passed through an Ordinance, met with stiff political resistance and the government dropped the idea. Labour laws were relaxed with Parliament sanctioning four new codes, but these are yet to be ratified by all the states with necessary notifications. Worse, some trade unions continue to oppose the changes. Three agricultural laws were passed by Parliament during Covid, but farmers in some north Indian states were upset and their protests forced the Modi government to roll them back.

The government, it seems, has the right intentions in bringing about these factor-market reforms but somehow has either lost the political will or is against using its political capital to bring about these changes. The first Budget of the new government after its formation in 2024 talked about bringing out a new economic policy framework to usher in the next generation of reforms to improve employment opportunities and sustain higher growth. However, not much action has been seen on the ground. In its second Budget, the need for fresh reforms in taxation and the financial sector has been underlined.

The time is now ripe for relaxing the legislation for land, enforcing the implementation of the new labour codes, reinstating the rolled-back laws on agriculture, raising investments in research and development in industry as well as in agriculture, introducing power sector reforms particularly at the distribution-end, bringing about urban policy changes, tweaking the bilateral investment treaties to make them more investor-friendly, implementing the privatisation policy and strengthening the judicial system to expedite legal redress of grievances.

However, there is virtually nothing new in these policy prescriptions. Policy experts have been talking about these policy reforms for almost decades and the pace of executing these changes has been slow.

![]()

So, what more needs to be done?

To take full advantage of the disruption caused by Trump’s policies, the government must revisit the manner in which it conceives and implements reforms. Instead of focusing on what needs to be reformed, time has come to worry more about framing a strategy on how the reforms could be implemented quickly and effectively.

Four suggestions are worth considering. One, the practice of setting up expert committees to examine the pros and cons of a reform idea should be revived. As in 1991 (when domain experts like Raja Chelliah, M Narasimham and RN Malhotra headed committees to submit their recommendations on policy changes for taxation, banking and the insurance industry, respectively), the government should look at identifying experts who could undertake the task of advising the government on how reforms could be undertaken now.

Two, even though several promises of reforming civil services have been made, little progress has been achieved. Even the recent attempts at inducting domain experts into the government did not make any headway in the face of opposition from within the civil services. Similarly, the responsibility of framing reformist policies should be separated from those who should be entrusted with the task of implementing them. That principle can be followed more effectively if private-sector domain experts are recruited in various levels of government service.

Three, reforms are direly needed as much in the states as in the Centre. Since the abolition of the Planning Commission in 2014, there is no institutional mechanism that can provide a platform for Centre-state dialogue and consultation on the ideation and execution of such reforms. The Inter-State Council, set up to facilitate Centre-state relations, has met only once in the last 11 years and just twice in the previous 10. It is time to think of an organisational fix by creating a body on the lines of the Goods and Services Tax Council to facilitate the formulation of next-generation reforms at the Centre and in the states.

Finally, the most important imperative in the current rapidly changing global economic environment is the need for the government to use its formidable political capital for expediting economic reforms. If reforms in 1991 got implemented without much of a problem, it was because of a combination of factors: An unprecedented economic crisis and a political leadership that was willing to build consensus for reforms within the government and among industry leaders as well as other economic stakeholders.

The Trump disruption of 2025 can be an opportunity for India, not just if it enters a few trade agreements or it reduces tariffs. The bigger gain would be if this situation is exploited to build a consensus within the government and among industry leaders on the need for wide-ranging economic reforms and by focusing on the process of executing reforms. That approach perhaps can make India economically more resilient, if not future-proof the Indian economy against further external shocks.