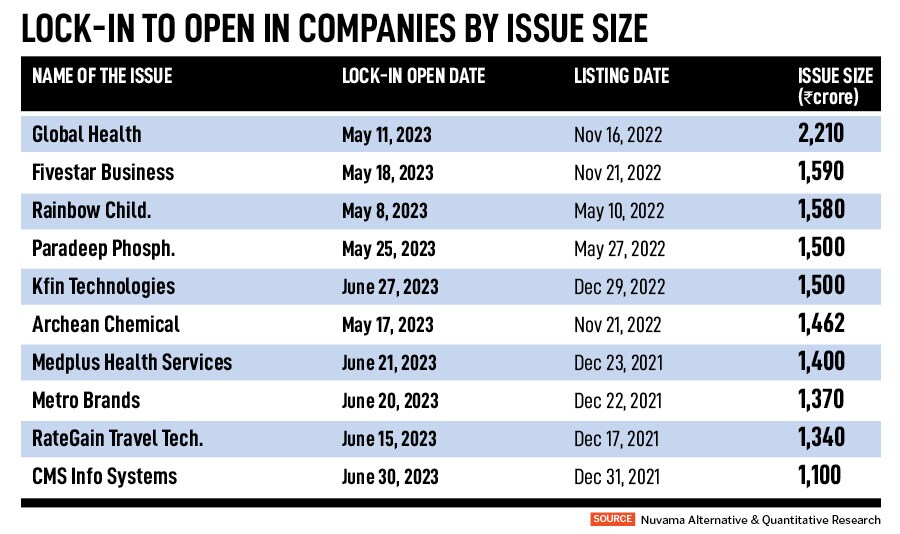

Pre-listing shareholders’ lock-in will open for 33 companies in the April-July period, which may knock off shares worth Rs 61,338 crore, based on an analysis by Nuvama Alternative & Quantitative Research. The analysis considers the closing price of all the stocks as on March 31. These companies had collectbively raised Rs 31,550 crore, and include Global Health (Medanta), Five Star Business Finance, Bikaji Foods, Inox Green, Paradeep Phosphates, RateGain Travel Technologies and KFin Technologies.

As per the analysis, five companies—Radiant Cash Management, Divgi TorqTransfer Systems, Sah Polymer, Electronics Mart, and Kaynes Technology—will see their lock-in period opening in April, while 15 will open in May.

Of the stocks under analysis, there are three that have gained over 100 percent over its issue price. Till March end, the share price of Hariom Pipe has seen a bumper rally, surging 221 percent over its issue while its listing gains were 51 percent. Data Patterns’ (India) share price zoomed 131 percent, after a listing gain of 29 percent, while Venus Pipes has jumped 123 percent, with listing gains of 9 percent.

Then, there are those that have lost too. The share price of AGS Transact Technologies slipped 74 percent till March end over its issue price. Elin Electronics shed 52 percent over its issue price, while on the listing day it fell 8 percent. DCX Systems fell 31 percent since its listing, but gained 49 percent on its day of listing.

“We have seen in the past that anchor investors generally find an exit route after the lock-in period opens up, which at times puts an additional pressure on the stock. However, promoters continue to hold even after the expiry. We have considered all shareholders, non-promoters [like anchor investors, private equity] and promoters," says Abhilash Pagaria, head, Nuvama Alternative & Quantitative Research.

Shares of highly sought-after companies like FSN E-Commerce Ventures (Nykaa) and One97 Communications (Paytm) faced intense selling pressure after the mandatory one-year lock-in period opened last November. For instance, shares of Paytm tumbled over 20 percent in the same month.

What is a lock-in period?

Market regulator Securities and Exchange Board of India (Sebi) has mandated different lock-in periods for separate categories of existing shareholders in a company that is listed on the stock exchanges via the IPO route. The lock-in filters are meant to arrest immediate decline in stocks after listing. For instance, there is a lock-in of 30 days for 50 percent of the portion allocated to anchor investors, and a lock-in of 90 days for the remaining portion. Earlier, the lock-in period for anchor investors was 30 days, which caused a drastic decline in share prices after the window of selling opened.

![]()

For promoters’ shareholding, the lock-in to the extent of minimum promoters’ contribution, which is 20 percent of post-issue capital, is for a period of 18 months. This mandate applies if the object of the issue involves only offer-for-sale (OFS) or if fund raising is for any purpose other than for capital expenditure for a project (more than 50 percent of the fresh issue size). According to Sebi, the promoters’ shareholding in excess of minimum promoter contribution is locked-in for a period of six months instead of the existing one year.

The lock-in of pre-IPO securities held by persons other than promoters has a lock-in for a period of six months. The period of holding of equity shares for venture capital funds or alternative investment funds (AIF) of Category 1 or Category 2, or a foreign venture capital investor, is six months.

IPO slowdown in FY23

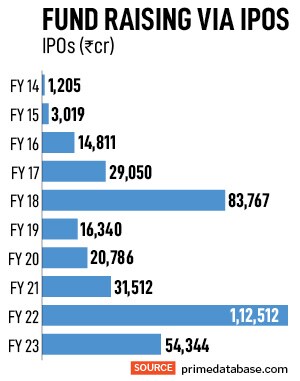

Primary markets in India slowed down in FY23 as volatility in equities caused by nervousness among investors, leading to massive wealth erosion. Rapidly rising interest rates worldwide, geopolitics, and, more recently, the global liquidity crisis caused by Silicon Valley Bank’s collapse and the Credit Suisse issue has stroked fears of an impending recession. These have jittered sentiments, with companies waiting for market conditions to calm down before going public.

As many as 37 Indian companies raised Rs 52,116 crore through IPOs in financial year ending March, which is a drastic fall from the all-time highs of Rs 1,11,547 crore in FY22, according to primedatabase.com estimates. A sum of Rs 20,557 crore or a whopping 39 percent of the total amount raised by IPO in FY23 was by Life Insurance Corporation (LIC) alone, without which the IPO fundraising would have been just Rs 31,559 crore. However, the amount raised in FY23 is still the third highest ever in terms of IPO fund raise. In the previous fiscal, 53 companies raised funds via the IPO route and got listed on the stock exchanges.

“As many as 25 out of the 37 IPOs were in just three months of the year [May, November and December], which shows the volatile conditions prevalent through most of the year, which are not conducive for IPO activity. In fact, the fourth quarter of 2022-23 has seen the lowest amount being raised in the last nine years," says Pranav Haldea, managing director, Prime Database Group.

In FY23, only Delhivery and Tracxn Technologies belonged to new-age technology companies, indicating a slowdown in IPOs from this sector. This compares to five new-age technology companies raising Rs 41,733 crore through IPOs in FY22.

Listing gains fizzling out

What also turned the IPO market in India cold in FY23 is low listing gains, popularly known as listing pop. Typically, retail investors in pursuit of chasing quick bucks buy shares in new companies in the IPO phase, but insignificant increases in listing prices deterred this phenomenon last fiscal. Data analysis of the IPOs in FY23, showed that 16 companies gave a return of over 10 percent.

As stock market returns dwindled, active participation by retail investors also ebbed out. Data shows that retail investors stayed away from subscribing to IPOs in FY23. The average number of applications from retail investors dropped to just 5.64 lakh in FY23 from 13.32 lakh in FY22 and 12.73 lakh in FY21. The highest number of applications from retail investors were received by LIC (32.76 lakh), followed by Harsha Engineers (23.86 lakh) and Campus Activewear (17.27 lakh).

By value, the number of shares applied for by retail investors was Rs 41,671 crore. This category of investors had seen a jump of 17 percent in FY22 compared to the previous fiscal.

Who was at the exit door?

IPOs in FY23 were mainly for raising fresh capital and not merely for offering exits to prior investors. A staggering Rs 14,034 crore, raised by combined IPOs in FY23, was for fresh capital. Only 14 out of the 37 IPOs that hit the market had a prior private (PE) equity or venture capital (VC) investor which sold shares in the IPO. OFS by such PE/VC investors at Rs 7,902 crore accounted for 15 percent of the total IPO amount, OFS by private promoters at Rs 6,373 crore was only 12 percent of the IPO amount, while those by the government was 40 percent of the IPO amount.

![]() Anchor investors collectively subscribed to 32 percent of the total public issue amount, while qualified institutional buyers (including anchors Investors) as a whole subscribed to 59 percent of the total public issue amount.

Anchor investors collectively subscribed to 32 percent of the total public issue amount, while qualified institutional buyers (including anchors Investors) as a whole subscribed to 59 percent of the total public issue amount.

“FY23 saw 68 companies filing their offer document with Sebi for approval [in comparison to 144 in FY22], including the first ‘pre-filing’ case of Tata Play in December 2022. On the other hand, 37 companies looking to raise nearly Rs 52,060 crore let their approval lapse in 2022-23, 12 companies looking to raise Rs 10,386 crore withdrew their offer document and Sebi returned the offer document of a further nine companies looking to raise Rs 20,330 crore," Haldea adds.

According to Haldea, though, with weakness still prevailing in the secondary market, because of a combination of domestic and foreign factors, IPO activity is likely to remain muted for the first couple of quarters. He adds there may be some smaller-sized IPOs. However, it will be a while before we see larger-sized deals, especially in light of the lack of sustained interest from foreign portfolio investors (FPIs).

In FY24, there are 54 companies that are proposing to raise Rs 76,189 crore, and which have got Sebi’s approval another 19 companies looking to raise about Rs 32,940 crore are awaiting Sebi’s approval.

Anchor investors collectively subscribed to 32 percent of the total public issue amount, while qualified institutional buyers (including anchors Investors) as a whole subscribed to 59 percent of the total public issue amount.

Anchor investors collectively subscribed to 32 percent of the total public issue amount, while qualified institutional buyers (including anchors Investors) as a whole subscribed to 59 percent of the total public issue amount.