The demand for unsecured loans continues to rise and has come to the attention of the RBI, again. The credit uptick signals buoyancy in the ecosystem on improved consumption and spending but the risk

Unsecured loans for most of the big banks in India have been growing rapidly

Image: Niharika Kulkarni / Reuters

Advertisement

There has been much good news in India’s economic growth story recently: Better-than-expected GDP growth, early signs of a recovery in domestic consumption demand and financial institutions that are aggressively lending. This last, however, is not necessarily great news for the traditionally cautious regulator Reserve Bank of India.

It has, both in informal discussions with banks, and formal publications (half-yearly) Financial Stability Report released in June this year highlighted the rapid pace of growth of unsecured loans in India’s retail loans segment over the past two years. Unsecured loans—largely personal loans, loans on credit cards and some forms of consumer durables and student education loans—do not have collateral and thus are considered riskier than secured loans (auto, home, loan against property). Add to that a still high interest rate regime and it raises risks to the lending system.

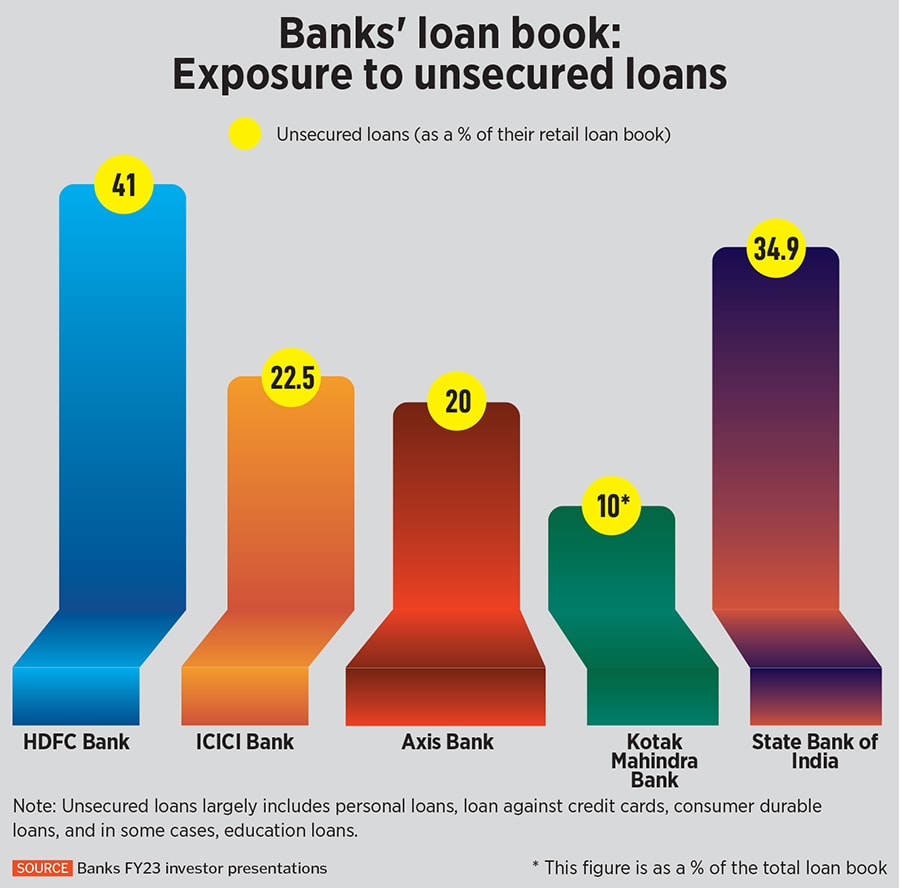

Unsecured loans for most of the big banks in India have been growing rapidly (see chart). Retail grew at a CAGR of 24.8 percent from March 2021 to March 2023, almost double the CAGR of 13.8 percent for gross advances during the same period. It formed around one-third of the total banking system’s gross loans and advances.

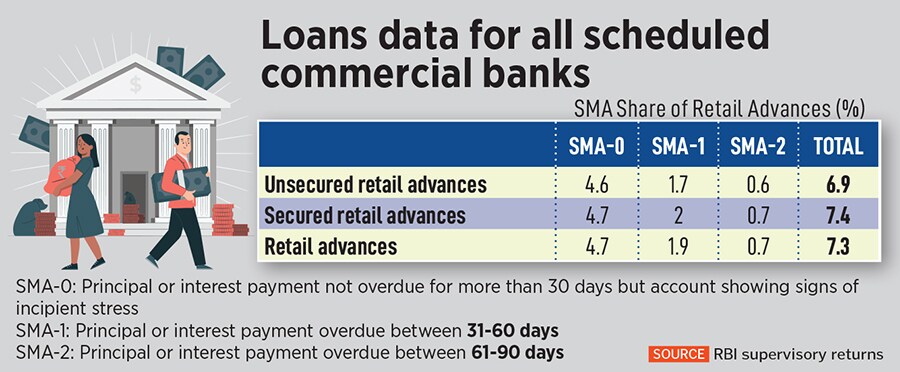

In this same period, unsecured retail loans increased from 22.9 percent to 25.2 percent and secured loans declined from 77.1 percent to 74.8 percent, the RBI Financial Stability Report for June 2023 showed. Although the Gross NPA ratio of retail loans at the system level was low at 1.4 per cent in March 2023, the share of special mention accounts (SMA) was relatively high at 7.4 per cent for all scheduled commercial banks (see table) and it accounted for a tenth of the retail assets portfolio of PSBs.

In the past year, credit card outstanding in terms of bank credit has risen near 26 percent to Rs 1,94,282 crore as on March 24, 2023, compared to levels a year earlier. The credit towards personal loans has risen 22 percent to Rs 11,00,404 crore in the same period.

A sign of buoyancy

Experts recognise the concern the RBI has on the uptick in unsecured personal loans but say it is a sign of buoyancy. “People are willing to spend and buy more products and pay more for it… it is a sign of buoyancy in the system," says Akshay Mehrotra, CEO of digital fintech lender Fibe, formerly known as EarlySalary.

“The report does not say that it is a sign of concern, just that demand for unsecured loans is growing phenomenally. Unsecured loans are an indicator of consumption economy while secured loans are an indicator of asset economy (where people buy assets like homes or cars)," Mehrotra told Forbes India. Fibe has seen an impressive growth in its business, with an AUM of Rs 2,400 crore, adding Rs 150 crore each month. It had raised $110 million from investors TPG’s Rise Fund and Norwest Venture Partners.

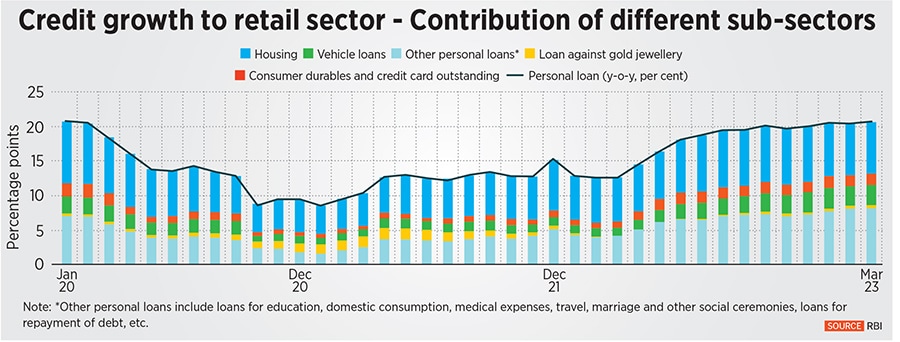

Even within the retail loans segment, the demand for personal loans and credit cards loans is running better than other segments. On average, credit card loans are growing at 30 percent, double the pace of home loans. Personal loan growth is also growing at a higher tick than the overall retail loans portfolio (20 percent), analysts say.

Both these segments also contribute towards improved margin growth for banks. Unsecured retail loans formed 7.9 per cent of the total banking system credit.

If the books for unsecured loans are growing too fast, players will naturally look for more opportunities and the originators of these. “Fintechs have been busy players, becoming originators of unsecured lending—unsecured is a good way to acquire a customer and then sell them a secured product later," Mehrotra adds.

He said banks have been partnering more than ever before with fintechs the number of co-lenders has doubled in the last year. Most of the leading banks such as SBI, Bank of Baroda and Axis Bank have in recent months tied up with non-banking financial companies (NBFCs) and fintechs to boost small-business loan activity.

For banks and NBCs, this has meant finding the route to provide loans faster, and at an affordable rate, to customers. Fibe did about Rs 300 crore of business in the past year through co-lending with banks.

Higher provisions expected?

The RBI has always been concerned whenever the demand for unsecured loans has outstripped the overall retail or other segments. Because of past experiences, the central bank wants the segment to grow in a calibrated manner. “The RBI may call for higher provisions or higher risk weights on unsecured personal loans and credit cards, if the demand for these loans continues to rise," a source at a private bank said, declining to be named.

Some banks, such as HDFC Bank—where unsecured loans form 41 percent of the retail loan book—the provision coverage ratio for unsecured loans is at a high 96 percent.

A TransUnion CIBIL report of April 2023 showed year-on-year credit card loans grew the fastest amongst all retail loan products (77 percent) and personal loans the second fastest (50 percent), for the October to December 2022 period.

Analyst Nitin Aggarwal, head of banking, insurance & financials research at Motilal Oswal Institutional Equities says: “The potential for increased risks to the ecosystem arising out of delinquencies in these two segments is not being seen at the moment."

The only marginal concern has come from SBI Card which has “identified a small segment of the legacy portfolio, which was showing higher delinquencies", its managing director and CEO Rama Mohan Rao Amara told media in May this year. The card issuer has told media that it will “reduce the kind of flow rates and also improve the write-off kind of performance".

The regulator might also start to have a closer look at the lending patterns of the buy-now-pay-later (BNPL) model, which really constitutes a type of personal loan. There is little data available on the delinquencies arising out of the BNPL model. Though the BNPL model is being rethought—after recent RBI regulations for non-banks on loading private payments instruments (PPI) through credit lines—the lack of transparency raises more concerns.