What's driving Paytm's stock price?

Although still below its IPO price of Rs2,150, the payments provider's stock has gained around 35 percent in the quarter ending June to around Rs850

Last Updated: Jul 06, 2023, 14:30 IST3 min

After reporting adjusted Ebitda breakeven in the three months ending December 2022, almost a year ahead of its guidance, Paytm’s stock has been on the upswing. Ten out of 13 analysts covering the fintech major recommend a buy rating on the stock, which has gained 35 percent in the three months ending June. What’s driving this bullish sentiment?

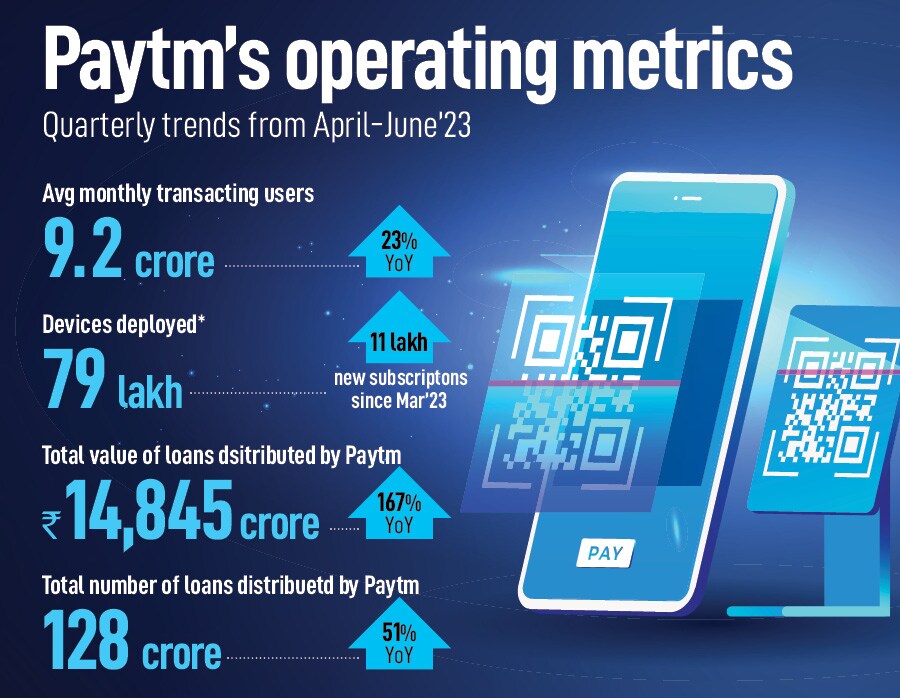

First, continued expansion of consumer base, as Paytm’s monthly transacting users (MTU) grew to 9.2 crore for the three months ending June, up 23 percent compared to 7.5 crore MTUs seen in the same three-month period a year ago (YoY).

Third, Paytm’s merchant payment volumes or GMV grew to Rs4.05 lakh crore ($49.3 billion) in the quarter ending June, up 37 percent from the Rs2.96 lakh crore GMV recorded in the quarter ending June 2022. “The sustained growth in the deployment of devices enables robust transaction volumes and drives healthy growth in merchant and consumer loans," says Nitin Aggarwal, research analyst at Motilal Oswal.

Fourth, Paytm disbursed loans worth Rs14,845 crore in the quarter ending June, up 167 percent YoY. A total of 1.2 crore loans were disbursed during the period, up 51 percent YoY. Loan ticket sizes increased from Rs10,000 in April to Rs12,500 in May, and the quality of loans also improved, notes Ansuman Deb, lead analyst at ICICI Securities. Paytm currently has seven lending partners and plans to onboard another three to four partners in the current financial year.

Also read: Paytm turns operationally profitable. But can it sustain the momentum?

Moreover, revenue from Paytm’s financial services arm—of which the loan business is a part—increased to 19 percent in FY23, up from a mere 4 percent in FY19. With faster growth in GMV, merchant acquisition and cross-sell rates, Aggarwal estimates financial services to contribute 32 percent to Paytm’s total revenues by FY25.

Fifth, in recent years, Paytm has been gradually moderating its payment processing charges, marketing activities, and promotional expenses. As a result, direct expenses have moderated to ~51 percent of revenue in FY23 from 162 percent in FY19. Similarly, indirect expenses have moderated to ~51 percent of revenue from 69 percent in FY19. “Paytm will naturally continue to invest in growth and merchant base expansion, but the improvement in operating leverage will nevertheless aid profitability," says Aggarwal.

Moreover, Paytm’s contribution margin has improved to 48.8 percent in FY23, up from 30.1 percent in FY22, driven by a rise in financial services revenue. Given this, Aggarwal believes Paytm is on track to report Ebitda breakeven in H2FY25.

Finally, there’s massive headroom to still grow. “Penetration within Paytm’s universe remains very low," says Deb. Postpaid (BNPL) loans as a percentage of average MTUs were a mere 4.3 percent in Q4FY23. Personal loans as a percentage of MTUs were 0.9 percent in Q4FY23. Merchant loans as a percent of device merchants were 5.9 percent and device penetration as a percentage of total merchants was 20 percent.

Says Deb, “The positive cycle customer growth, retention and cross-sell shown by the company will only continue to build confidence [in the stock]."

First Published: Jul 06, 2023, 14:30

Subscribe Now