Adopting digital financial services to further the goal for financial inclusion remains paramount for the RBI. It has to be achieved under the overarching need to provide a seamless payment experience while ensuring financial security and minimising privacy risks. But in a crowded world where payment aggregators, payment gateways and fintechs are trying to boost transaction volumes to be relevant, it is payments banks (PB) that have an edge over them by owning the customer account.

PBs were set up as niche entities to facilitate small savings, and to provide payments and remittance services to migrant labour, low-income households, small businesses and other unorganised sector entities.

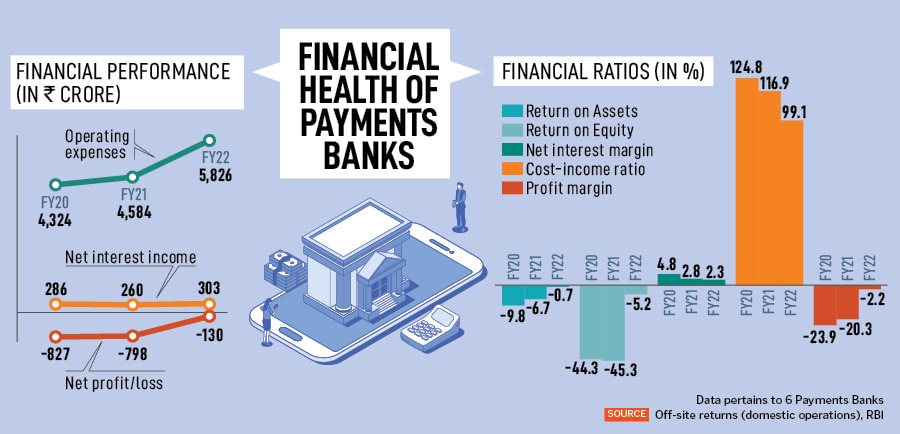

Around six years after most payments banks went live in India, three of the existing six—Airtel Payments Bank, Paytm Payments Bank and Fino Payments Bank—are profitable, according to data available from them and the RBI. India Post Payments Bank is likely to break-even by FY24. The RBI continues to restrain PBs from issuing loans directly, which impacts the ability to earn more interest and their ability to build a sizeable balance sheet.

Further, 75 percent of the deposits earned (a maximum end-of-day limit of Rs2 lakh per individual customer) has to be parked with government securities of one-year maturity and the balance can be kept with commercial banks. The higher interest rate regime has meant improved yields from these bonds. The PBs also need to maintain the statutory cash reserve ratio (CRR), as decided by the RBI.

PBs earn revenues through transaction charges on utility bill payments and other such transactions, earnings from micro-ATMs for providing remittances and cash withdrawal services, providing business correspondence services to other banks, cash management services and commission on transactions through PoS (point of service) terminals and MDR (merchant discount rate) charges and para-banking activities.

The current ecosystem within which PBs operate should be considered testing in some ways—where income from payments is still the majority earner for most banks, followed by income from cross-selling financial products and then interest income.

Finding their Differential

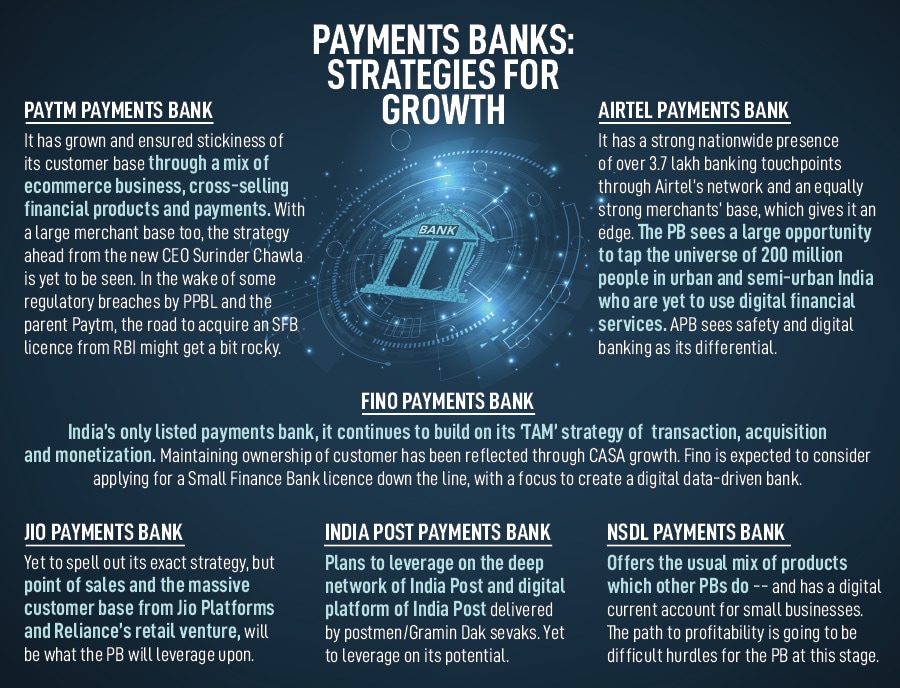

In this scenario, each of the PBs has identified its own strategies for growth and a differential (see table), which have kept them relevant.

The unlisted Airtel Payments Bank (APB), which forms part of the broader Bharti Airtel telecom group, is one of the fastest-growing PBs. APB has shown a profit of Rs21.7 crore on revenues of Rs1,291 crore for FY23. The bank turned profitable in FY22 and “has been rapidly growing with a 40 percent CAGR on revenues over the last three years", its managing director and CEO Anubrata Biswas tells Forbes India.

APB is a largely digital banking operation, with just seven physical branches, serving over 56 million customers totally. The bank has a base of 3.44 lakh monthly active merchants along with a network of 3.7 lakh monthly active banking points, who are business correspondents (BCs) rewired from the large base of Airtel’s original retailers. The BCs deal with customers in Tier V or IX parts of India, where they are assisted with opening of bank accounts, sending money and carrying out transactions at micro ATMs.

Biswas claims that in this rural landscape, APB is the largest inclusion bank with 20 million users monthly, while rival Fino has about 7.5 million across the country. Paytm, though, has a large transacting user base of around 90 million, but the dedicated Paytm Payments Bank customer base is difficult to assess.

For urban Indians, Biswas’s strategy to attract customers is linked towards ‘safety’ and ‘digital banking’ rather than payments. “A payments bank account became a natural conduit for someone to open an ancillary bank account and keep some money aside for online transactions," Biswas says.

One of the unique India-First innovations, Airtel ‘Safe Pay’, serves as a third layer of authentication—compared to the industry’s two-factor authentication norm—and a high level of protection from potential frauds such as phishing, stolen credentials or passwords and phone cloning.

![]()

The thrust to grow CASA (current and savings accounts) and deposits has continued for APB. In FY23, it opened nine million savings accounts, reflecting a 17 percent year-over-year (y-o-y) growth, and customer deposits growth of 59 percent y-o-y to Rs1,865 crore. “This growth has been fuelled by rising consumer interest and increased adoption of the bank’s core propositions of digital safety and omnichannel convenience, across India and Bharat," he says. The digital presence for APB is real: The PB’s GMV stood at Rs2.01 lakh crore in FY23 and it now processes over seven billion annualised transactions across its platforms.

Cross-selling of financial products is something where it competes with Paytm Payments Bank, but Biswas claims APB is one of the largest distributors of micro-insurance in India.

Almost 77 percent of the bank’s revenues currently come from payments, followed by 16 percent from fee income and 7 percent from consumer deposits. “This mix has and is rapidly changing as the bank grows its users and usage," Biswas says.

As APB continues to expand across India, Biswas is confident of a still-vastly-untapped digital banking opportunity. “There are 500 million people who are underserved in banking and will upgrade to formal banking or digital banking. Of this, there is a 200 million user opportunity in urban and semi-urban India, who use smartphones but are yet to upgrade to digital payments," Biswas adds. Every year, India opens 80 to 90 million new bank accounts and APB opens one in 10 bank accounts each year.

**********

Fino Payments Bank occupies a unique spot in the PB ecosystem: It is the only listed entity and one of the few not promoted by a corporate entity. Fino (Financial Inclusion Network & Operations) was incubated as a business correspondent by ICICI Bank in July 2006, before getting the nod for a payments banking licence in 2017.

Its strength was its reach and the rich experience of servicing customers on ground in remote locations. This meant having a largely physical presence, unlike other PBs, that are more digital focussed. Currently, Fino, besides a 7.5 million customer base, has a 1.4 million merchant base which it plans to grow to two million by FY26.

Continuing to focus on its TAM strategy—which is transaction, acquisition and monetisation—the PB is already well into the phase II and III of its strategy, focusing on customer acquisition and monetisation. It had built its transaction phase by offering a range of simple products such as remittances, cash withdrawal products, domestic money transfers and micro ATM and AEPS (Aadhaar-enabled payment systems) to hook customers into the Fino ecosystem.

Fino continues to see growth through its CASA and cash management systems (CMS), with 75.2 lakh CASA accounts in FY23, a 45 percent y-o-y jump in new accounts. Deposit growth has risen by 66 percent y-o-y in FY23 to Rs1,200 crore. Fino added over 2.5 lakh new CASA accounts every month in the three months to March 2023.

![]() Rishi Gupta, MD & CEO, Fino Payments Bank Ltd

Rishi Gupta, MD & CEO, Fino Payments Bank Ltd

While continuing to build on CASA, Fino PB, like its peers, is now concentrating on cross-selling financial products. This had started with gold loans and insurance, but it only caters to a small segment of customers and needs to scale up where the model becomes business-to-business-to-consumer B2B2C.

Fino Payments Bank’s offer of a sweep account facility along with Suryoday Small Finance Bank, which started in 2019-20, has worked well for its customers. The partnership allows customers to transfer the excess amount from their deposit account in Fino to Suryoday, helping them to earn more on their account.

Rishi Gupta, Fino Payments Bank’s managing director and CEO, says the focus for the bank will be to convert the walk-in transacting customer (‘off us’) to a CASA customer (‘on us’). “This also results in a shift of our revenue pie from transaction business to higher-margin ownership business," Gupta says. Renewal income for Fino has surged by 167 percent to Rs73.1 crore in FY23 from Rs27.5 crore a year earlier. CMS throughput has grown by 10x from Rs4,300 crore in FY20 to nearly Rs46,000 crore in FY23.

While the focus will be to also grow the transaction volumes and CASA accounts, Gupta says Fino’s main advantage is that it has a low customer acquisition cost, since it does not advertise aggressively or offer massive cashback offers.

Sanjay Khan Nagra, partner (corporate and commercial practice group) at Khaitan & Co, believes that customer acquisition and retention—rather than pure earnings from payments transactions—will be the differentiator among PBs. “NBFCs have a loan-based relationship, but banks have a savings-based relationship. If a payments bank can ensure that an individual is a regular and creditworthy user, they could leverage on such individual"s data to empower them to access customised products," he says.

“Cross-selling, bundling of products/services and offering payments commissions are all value adds and solutions for these banks. Customer acquisitions and retention are the first steps towards a long-term financially viable businesses," Nagra tells Forbes India.

*********

The strategy of customer acquisition and retention is what Paytm has built over the past decade across its platform—what started several years ago with offerings such as paying utility bills, internet data card charges and postpaid mobile bills. The business engine was obviously propelled by the ruling government’s move for demonetisation, but the parent company had already solidified its base through the acquisition of wallet customers by then.

The Paytm Payments Bank (PPBL) continues to leverage on the success of Paytm’s wallet customers and on the strong merchant relationships which Paytm has built over the years. For payment services, Paytm earns revenues from the transaction fee it charges merchants based on a percentage of transaction value and consumer convenience fees from consumers, for certain types of transactions.

The PPBL does not need to tweak its business model too much, having a mix of ecommerce business, cross-selling and distribution of loans and insurance and payments, to retain its customer base. The percentage of income from pure payment transactions—as seen for several PBs—is likely to continue to diminish in value, as the UPI platform continues to grow.

![]()

In February, PPBL went live with a UPI Lite app feature, which allows user to make transactions for as low as Rs200. Official data from the National Payments Corporation of India (NPCI) shows that more than half of the everyday UPI transactions in India are less than Rs200.

“Paytm Payments Bank is aggressively expanding into Tier III-IV towns. But the core wallet product is losing value to UPI, and customer acquisition cost and rate of customer addition will be a concern, particularly considering that customer acquisition is through the parent company," says Bhavik Hathi, managing director, Alvarez & Marsal. The strategy for growth under the new CEO and veteran banker Surinder Chawla, who joined them in January, needs to be tested. PPBL declined to participate in this story.

Financial performance for the other three PBs, Jio Payments Bank, India Post Payments Bank and NSDL Payments Bank, for recent years was not readily available. India Post Payments Bank CEO J Venkatramu told the Financial Express last month that the bank is “expected to break-even" by 2024-25, after having been in losses for the FY18 to FY22 period.

Path towards Small Finance Banks

The relevance for PBs and their ability to grow do in some way depend on whether the RBI considers to allow them to lend small-ticket loans. While this has often been extended to the regulator to consider, there is no signal that the RBI will concede and allow PBs to start lending.

If we assume that this proposal stays on the backburner, PBs have another option. RBI guidelines say a PB can apply for a conversion into a small finance bank (SFB), after five years of successful operation. SFBs take deposits in CASA and fixed deposit accounts, besides also providing a range of retail loans. These avenues would help boost a PB’s profitability, once they become an SFB.

Alvarez’s Bhavik says as businesses get bigger, “it remains to be seen how much capital and efforts will be made by the parent firm to make this business grow, compared to the core business". Airtel"s possible plan for a listing of the payments bank venture indicates the need to bring in capital and monetise the business.

Bhavik adds that in some cases, there could be a possibility where the models could morph or get absorbed into the ecosystem. “Paytm, Airtel and Jio will continue to focus on the core business of payments while the value proposition as a standalone payment bank play for India Post Payments Bank and NSDL Payments Bank remains a question."

PBs as a model always had question marks and they remain. The players will rethink whether they need to carry on business with the banking licence (with higher cost structure and more compliance) or go down the path of fintechs who, except for raising CASA, can do the same with more flexibility and agility given how business models and regulations are changing, Bhavik adds.

Khaitan’s Nagra says upgrading into an SFB could be an option for some PBs. “But some may also choose to remain a payments-first type of fintech, where the focus is on technology, which would help them leverage with whoever is the best-suited regulated entity—a lender, an insurance partner, etc—and offer the relevant services to their customer."

In the current stage of their business journey, most PBs are focussed on not just customer acquisition but also retention. Paytm and Fino could consider the SFB route at some point, while APB is more likely to grow further and seek to unlock shareholder value at a suitable time, over the next one or two 2 years. Till then, PBs will continue to be tested in their endavour to become stronger and bigger.