Digital payments, the biggest fintech segment, will continue to see the strong growth of recent years, touching an estimated $153 billion in transaction value in 2023, compared with $133 billion in 2022, according to data from Statista. Neo banking, which typically refers to fintech ventures that offer banking products and services in partnership with regulated entities, and can also include modern digital banking, will touch $65 billion in transaction value this year, versus $47 billion last year.

One thing about India’s fintech ecosystem is that regulation is striking a fine balance between innovation and security, says Avinash Godkhindi, co-founder and CEO of Zaggle, which offers expense management software to enterprise customers. The one-time password on the cell phone for various transactions is a simple, but great example of that, he says. The bottom line is, “people should be able to trust your platform," he points out, and if the innovation-with-regulation approach continues to ensure that, large global fintech companies could emerge from India.

For now, here are five companies to watch in 2023, as they seek their next phase of growth.

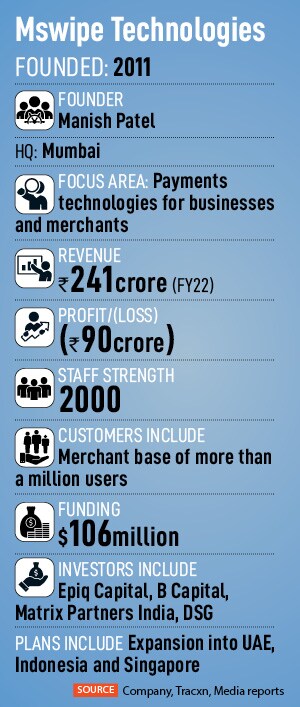

![]() Mswipe Technologies was started more than 11 years ago, and over the course of time, “we"ve seen everything, survived everything, and tried to master whatever we could," CEO Ketan Patel told Forbes India in July 2022. At the time, the company, well known for its point-of-sale terminals, had around half a million merchants using them, Patel said. From 2017-18 Mswipe has focussed on QR code-based payments, with a million merchants using its QR codes, he said. More recently, it brought its own soundbox, the Mswipe Boombox, to the market with which merchants can get sound and display notifications for payments. Mswipe also has an NBFC permit and has been expanding its lending business over the last year or so.

Mswipe Technologies was started more than 11 years ago, and over the course of time, “we"ve seen everything, survived everything, and tried to master whatever we could," CEO Ketan Patel told Forbes India in July 2022. At the time, the company, well known for its point-of-sale terminals, had around half a million merchants using them, Patel said. From 2017-18 Mswipe has focussed on QR code-based payments, with a million merchants using its QR codes, he said. More recently, it brought its own soundbox, the Mswipe Boombox, to the market with which merchants can get sound and display notifications for payments. Mswipe also has an NBFC permit and has been expanding its lending business over the last year or so.

This year it aims to increase revenue by 70 percent and become profitable, both on the payments side and the lending business, Patel said. In August, Mswipe received an in-principal nod from the Reserve Bank of India for its payments aggregator application, CFO Rohit Agrawal told the media in October. This permit will help the company become a bigger online payments operator for its merchant base.

Mswipe sees payments volume of about $3 billion on an annualised basis, according to Agrawal, who is also CEO of MCapital, the NBFC business of Mswipe. Overall, he expects the company to be profitable in the fourth quarter of the current fiscal or the first quarter of the year starting April 2023, according to media reports.

From an innovation perspective, two initiatives by Mswipe are noteworthy. First, with respect to buy-now-pay-later (BNPL), Mswipe has taken the approach of creating a platform 0that will help merchants offer it to consumers. Mswipe itself has stayed away from making BNPL loans. “Our ultimate aim is that the merchant’s business increases," Patel said. In this context, Mswipe is marketing an all-in-one mobile phone, called ‘Dukaan ka phone’, priced at Rs 8,000 that merchants can use to accept card payments, generate dynamic QR codes and so on.

The trigger for this idea came from visiting shops in smaller towns, where typically, post-lunch, the shop owner goes home for a siesta, Patel said. During that time0 there will be one other helper in the store who often doesn’t know how to accept QR-code-based payments. This phone, meant to be always kept in the shop, will help, he said, as it can “accept everything".

In the long run, Mswipe will evolve into a digital bank focussed on small merchants, Patel said. From point-of-sale machines to micro-ATMs to BNPL as a platform, “everything that we’ve been doing is towards that," he says. Currently Mswipe is waiting for a corporate agency license, where it has created a product that will allow merchants to sell insurance policies on PoS terminals.

Eventually, Mswipe will seek a banking license, he said.

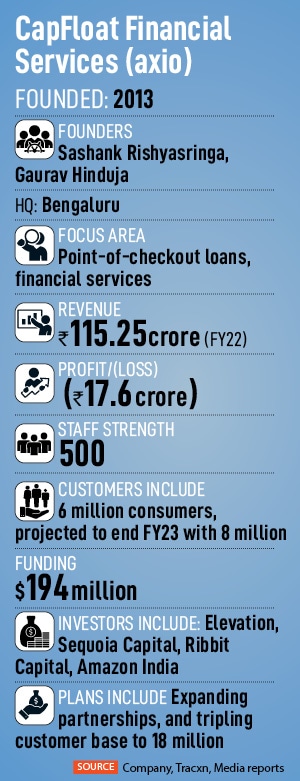

Axio: Redefining consumer loans

![]() Sashank Rishyasringa (left), Gaurav Hinduja cofounders, axio finance

Sashank Rishyasringa (left), Gaurav Hinduja cofounders, axio finance

![]() Axio’s founders took their time finding their groove. The Bengaluru company started with a license to provide loans as a non-banking lender, and the plan was to use proprietary algorithms and processes to figure out creditworthiness and give loans painlessly and quickly.

Axio’s founders took their time finding their groove. The Bengaluru company started with a license to provide loans as a non-banking lender, and the plan was to use proprietary algorithms and processes to figure out creditworthiness and give loans painlessly and quickly.

With the rise of ecommerce and mobile data-based internet penetration in India, Sashank Rishyasringa and Gaurav Hinduja zeroed in on checkout finance. Their venture has more than 6 million consumers taking loans at the point of sale. Hundreds of thousands more are joining every month, and Axio expects to end the current financial year with 8 million customers. “We are embedded into some of the largest ecommerce ecosystems in the country," Hinduja says, which has helped Axio acquire customers at a low cost.

Axio’s tech and underwriting prowess has developed to the level where consumers can get a loan “in under 3 seconds", and use the money for their online purchases at the point of sale. Axio’s software engines can offer “100 millisecond response time on Diwali sale day," Hinduja says.

While the Covid-19 pandemic accelerated the rate at which consumers adopted Axio, the lender has also been able to keep bad loans at less than 2 percent of its portfolio, the duo says. One of the ways is by keeping initial loans to new users low—say Rs 5,000—and growing with them as they prove creditworthy. Axio has automated much of this, they say.

“The big shift has been to go from thinking about products as building blocks to thinking of customers as building blocks," Rishyasringa adds. “Checkout finance is the beginning of a relationship it’s how we acquire customers and how they discover us. Once the customer uses us to finance one purchase, our aspiration is to grow to meet other, larger, needs as they arrive."

Today there are about 130-150 million people in India who shop online. There are, however, more than 250 million who use UPI. And the number of unique credit card holders is only at around 30 million. Over the next two or three years, the number of online shoppers is expected to go to 250 million or more, whereas the number of unique credit card holders is only expected to hit 50-60 million. Therefore, Axio’s founders see an opportunity to offer their products to that segment of 200 million “digitally active" users who won’t have credit cards but still need credit for their purchases.

An acquisition that Axio announced in August 2018 is also playing an important role in accelerating its consumer finance business. Axio purchased Walnut in a $30 million cash-and-stock deal and since then integrated everything under the Axio brand. Customers can get loans, but also use the features that came from Walnut, such as tracking their spends.

The app gives customers “a 360-degree view" of their finances, which is the first step towards financial literacy, Rishyasringa says. Next, it’s possible to build features within the app that help customers make better spending decisions. For example, diverting some idle money into a fixed deposit or showing a prompt to make a credit card payment at a time that would save the user money on interest and so on. Some of these features are already available on the Axio app.

One challenge in Axio’s sector is that the demand for credit is very large. Any regulation that can make it easier for the supply-side to expand will help, Rishyasringa says. In 2023, Axio’s founders expect to triple their customer base.

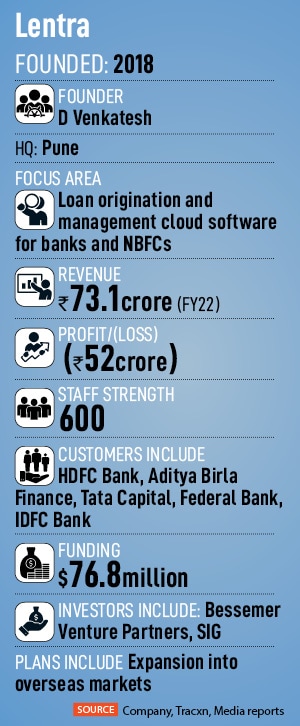

Lentra: Software for transforming lending

![]() Lentra, founder, D Venkatesh

Lentra, founder, D Venkatesh

![]() D Venkatesh got the idea for Lentra because he was already dealing with banks as customers in his previous company. The first product he created at Lentra offered a way for the bank or a lender to query a credit bureau and get a report in an automated fashion. Within three years of being founded in Pune, Lentra added systems for loan origination, loan management, campaign management, lead qualification, collection, and reports generation.

D Venkatesh got the idea for Lentra because he was already dealing with banks as customers in his previous company. The first product he created at Lentra offered a way for the bank or a lender to query a credit bureau and get a report in an automated fashion. Within three years of being founded in Pune, Lentra added systems for loan origination, loan management, campaign management, lead qualification, collection, and reports generation.

“We got the whole nine yards for lending covered and in a manner that the banks can use immediately and in a way that it allows them to come in at a point that they think is useful to them and exit at a point that they think is enough for them," Venkatesh says. “It doesn"t force the bank to use any of our modules that they don"t want to use right now. If they want to solve a specific slice of the entire universe, they could do that on the platform. There are no compulsions that the platform dictates."

Origination is a complicated problem and it can never hit 100 percent, Venkatesh says. It’s time-consuming because the bank has to pin down the identity of borrowers, their backgrounds, and “look for any tremors" with respect to their cash flow. Lentra has built software that make much of this rule-based and automated, helping banks scale up the processing of applications. It is work in progress, but it’s come to a point where 95 percent of the applications processed on the platform are processed with no human intervention.

For the remaining 5 percent, Lentra has built chat and internet-based communication channels so that the bank’s back office can even be in smaller cities and towns. The software also offers an expanding product feature set: Richer reports, ability to schedule partial loan disbursals and collections, and so on. The banks save money on getting creditworthy customers, and identity fraud is approaching zero, where Lentra is used, Venkatesh says.

“We have far exceeded the banks’ expectations on all dimensions," Venkatesh says. “People forget information security and the availability angles when they do these kinds of pieces, but we"ve excelled on those fronts." From the time of inception, Lentra has helped banks give out billions of dollars in loans. On a typical day, its platform helps process over 150,000 applications, Venkatesh says. With the team of employees expected to reach 800, Lentra has visibility of customers and orders to $100 million in revenue in FY24, he says. Beyond that, the ambition is to get to $250 million revenues in 2026.

The latest funding round, also its biggest, of $60 million announced in November 2022, will help Lentra expand overseas, starting with markets like Vietnam, Indonesia and Philippines—out of a base in Singapore—but eventually the US.

The company is rewriting parts of its software “so it scales to a population that we assume will be in the neighbourhood of 12 billion people". If Lentra succeeds in this, then it will be able to handle the global load, he says. “We"ll use funds to strengthen the platform feature-wise, performance-wise, and making it a global software. We should be able to implement it in any language in any country sitting in India." Lentra is also looking at making some targeted acquisitions.

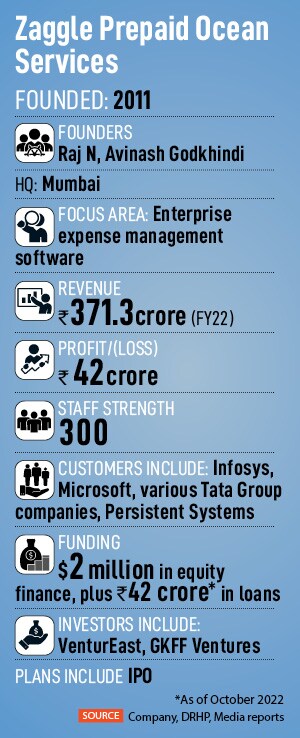

Zaggle: No-hassle expense management and more

![]() Avinash Godkhindi, cofounder, Zaggle Prepaid Ocean Services

Avinash Godkhindi, cofounder, Zaggle Prepaid Ocean Services

![]() Zaggle is a B2B2C software-as-a-service fintech company, offering its tech to enterprise customers who in turn use those solutions to digitise various financial and related processes for individual employees, such as benefits, rewards and expense management. The company also offers channel incentive management—for businesses to deal with their dealers and distributors, for example—and is expanding strongly into vendor management.

Zaggle is a B2B2C software-as-a-service fintech company, offering its tech to enterprise customers who in turn use those solutions to digitise various financial and related processes for individual employees, such as benefits, rewards and expense management. The company also offers channel incentive management—for businesses to deal with their dealers and distributors, for example—and is expanding strongly into vendor management.

“Anything that is repetitive, highly interactive and which culminates in a spend, we come in there," says co-founder and CEO Avinash Godkhindi. “We call it spend management 360."

The Zaggle of today is the result of multiple changes, starting with rewards and recognition in enterprises and moving to offering software to manage benefits and then reimbursements, which opened up the expense management opportunity and in turn vendor management.

Last year the company had revenues of about Rs 372 crore, with Ebidta of about Rs 60 crore. “This year we’ll do even better and the company is fairly scaled up," Godkhindi says. The company has been profitable for three years and its customers include Infosys, Persistent Systems, Microsoft, and various Tata Group companies. Zaggle’s software solutions and mobile app is available in English, Hindi, Telugu, Tamil and Kannada Godkhindi expects to add more languages.

One important reason why Zaggle found strong traction with customers is because it solved problems for business decision-makers who are those making a payment, says Godkhindi. “The decisions about whom to pay, how much to pay, when to pay, where to pay, are invariably taken by business, not accounts. Accounts just executes it. That"s the problem that we are solving."

The technology system is sitting with one set of people in accounts who can execute a payment, but how does the business executive, who is deciding on the payment, understand what’s happening. That communication often happens with emails and spreadsheets, he says. Zaggle’s software suite makes it possible for the business executive also to have a clear view of what’s happening with a payment.

Overall, Zaggle’s tech touches some 2,000 enterprise customers and about 2 million end users. Almost all its business comes from India, but there are plans to eventually offer the products overseas. Some customers, such as ed-tech venture Upgrad, are using Zaggle to facilitate certain payments overseas as well.

Zaggle has raised about $2 million in equity funding, according to private markets intelligence provider Tracxn. The company has also raised substantial debt funding and is currently looking to raise more money, Godkhindi says. Zaggle has filed initial papers to start the process of listing itself on the stock exchanges in Mumbai, according to media reports in December, and is looking to raise Rs 490 crore.

“I think spend management as a category is poised for explosive growth in India and worldwide," Godkhindi says. Companies such as Brex, Ramp, Spendesk and others are already multi-billion-dollar valuation companies, overseas, he points out. In India, the category is nascent, but fast growing. Zaggle aims to take the lead in India.

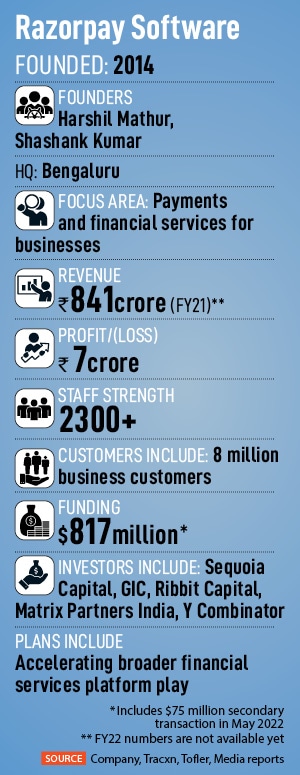

Razorpay: Broader play with sharp focus

![]() Shashank Kumar (right) and Harshil Mathur, cofounders, Razorpay Software

Shashank Kumar (right) and Harshil Mathur, cofounders, Razorpay Software

![]() Razorpay is at something of an inflexion point, as an organization too, which co-founder Shashank Kumar pointed out in a recent interview with Forbes India. It has reached a point where the venture—one of India’s best-known fintech companies—is ready for a professional CTO and head of engineering to take on the reins from Kumar. “We are at a stage where we are processing significant payments volume. It"s a critical part of the financial infrastructure of the country," Kumar said. “I was managing engineering full-time and was also looking after product and design and quite a few other functions."

Razorpay is at something of an inflexion point, as an organization too, which co-founder Shashank Kumar pointed out in a recent interview with Forbes India. It has reached a point where the venture—one of India’s best-known fintech companies—is ready for a professional CTO and head of engineering to take on the reins from Kumar. “We are at a stage where we are processing significant payments volume. It"s a critical part of the financial infrastructure of the country," Kumar said. “I was managing engineering full-time and was also looking after product and design and quite a few other functions."

Now the company has close to 1,000 engineers, including several senior engineering leaders. “If you look at the next five years … we felt like we need someone from an engineering leadership perspective who has seen tremendous scale, who has seen large operations and can help shape the direction of the company towards it."

That’s how, about eight months ago, Murali Brahmadesam, who has worked at Amazon Web Services and Microsoft, took over as CTO and head of engineering from Kumar. And the co-founder expects to focus more on product development and strategy. Brahmadesam sees himself as a “systems engineering" specialist meaning, he’s able to pull together different, complex and often large-scale systems and decide how they’re integrated and managed over their life cycle.

He has helped set up multiple locations at AWS and was part of the founding team of Aurora, the cloud company’s relational database service. After returning to India in early 2020, the combination of the market’s UPI-led fintech revolution and the engineering-focussed culture at Razorpay attracted him, he says.

Changes, such as senior executives joining, are taking place as Razorpay looks to step up its expansion into a broader financial services platform, from its flagship payments business—it accounts for most of its revenues and is making money on a standalone basis—to facilitating loans, and banking software.

The company is expected to go deeper into the emerging hot area of ‘banking as a service’, which accounting giant Deloitte defines as provisioning of banking products and services through third-party distributors. This opens up the possibility that a large number of new niche finance startups can partner large, established banks and financial services companies, and help each other tap a significantly larger market than they could individually. Razorpay could emerge as a facilitator of this growth, and benefit from it. In December 2021, the company was privately valued at $7.5 billion, making it one of India’s most valued startups.

To throw the story forward, while Razorpay has made a name for itself in India, “We want to see how we can create a global engineering brand while we are working out of Bengaluru and India," Kumar says. There are very few such companies from India and southeast Asia, he says Flipkart and Gojek are examples.

“I would really want to make Razorpay a well-known engineering-first brand worldwide."

Mswipe Technologies was started more than 11 years ago, and over the course of time, “we"ve seen everything, survived everything, and tried to master whatever we could," CEO

Mswipe Technologies was started more than 11 years ago, and over the course of time, “we"ve seen everything, survived everything, and tried to master whatever we could," CEO  Sashank Rishyasringa (left), Gaurav Hinduja cofounders, axio finance

Sashank Rishyasringa (left), Gaurav Hinduja cofounders, axio finance Axio’s founders took their time finding their groove. The Bengaluru company started with a license to provide loans as a non-banking lender, and the plan was to use proprietary algorithms and processes to figure out creditworthiness and give loans painlessly and quickly.

Axio’s founders took their time finding their groove. The Bengaluru company started with a license to provide loans as a non-banking lender, and the plan was to use proprietary algorithms and processes to figure out creditworthiness and give loans painlessly and quickly.

Zaggle is a B2B2C software-as-a-service fintech company, offering its tech to enterprise customers who in turn use those solutions to digitise various financial and related processes for individual employees, such as benefits, rewards and expense management. The company also offers channel incentive management—for businesses to deal with their dealers and distributors, for example—and is expanding strongly into vendor management.

Zaggle is a B2B2C software-as-a-service fintech company, offering its tech to enterprise customers who in turn use those solutions to digitise various financial and related processes for individual employees, such as benefits, rewards and expense management. The company also offers channel incentive management—for businesses to deal with their dealers and distributors, for example—and is expanding strongly into vendor management.