Lack of affordability and not innovation is a challenge for climate solutions in

Asset financing structures for energy efficiency, alternative heating and cooling solutions, and decarbonised industrial processes can go a long way towards helping scale climate adoption, Climake fou

India still needs significant capital to enable the adoption of climate tech solutions

Illustration: Sameer Pawar

Advertisement

Over the last year, private investment in climate innovation has grown rapidly, with equity investors deploying $7.15 billion in capital. If debt and green bonds are included, total climate investment in India is estimated to be as high as $20 billion. Renewable energy (solar and wind power) attracted 60 percent of equity investment emerging sectors such as electric mobility and agritech supply chain also generated considerable interest.

However, India still needs significant capital to enable the adoption of climate tech solutions. To achieve our goal of net-zero emissions, we need to move climate action from an emergent niche sector towards a mainstream activity. The challenge is not the lack of innovation it is the lack of affordability of physical and asset-heavy solutions, especially those developed for new market segments by early-stage startups.

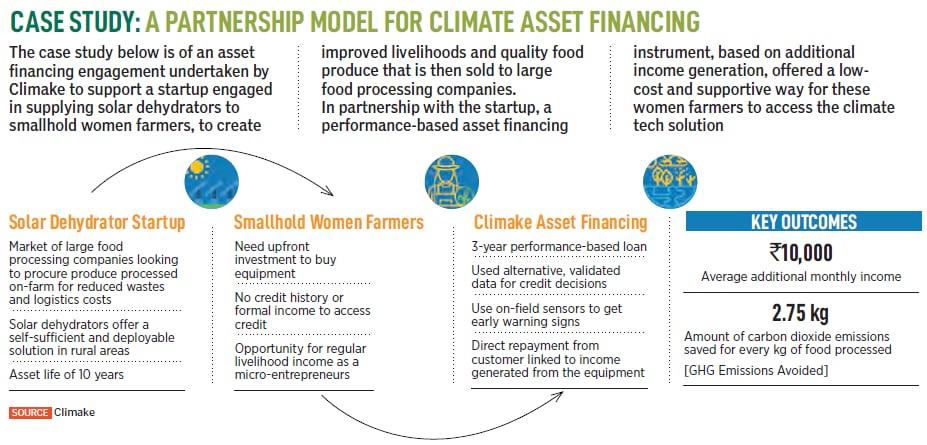

The climate tech financing gap

Forty percent of the country’s GHG emissions, used for powering our infrastructure, equipment, buildings and a lot more, can be addressed by a transition to renewable energy. Solar and wind companies are able to deploy solutions at scale by accessing a maturing and diverse range of financial instruments (equity, debt, bonds) developed over the last 20 years, with relative ease.

The other 60 percent of India’s GHG emissions come from activities and products that consumers and businesses rely on and use, such as transport, agriculture, and industrial and manufacturing processes. The solutions needed to tackle these emissions are also known as demand-side climate tech, a relatively nascent sector compared to renewable energy.

Adopters of demand-side climate tech solutions either replace existing assets (e.g. energy-efficient fans) or buy new, untested solutions (e.g. IoT solutions to reduce power consumption). They need to commit to an upfront capital cost that is usually more expensive than non-climate friendly alternatives, and hope that this additional cost will be recovered either from the cost-saving benefits or increased income from using the asset. There are two challenges here.

The first is that a large segment of India’s customers—individuals and small businesses—are unable to pay for capital investments upfront. In such cases, some customers can afford to make smaller regular payments over a period of time (something that EMI schemes have made familiar to them), especially if payments are linked to the additional income or cost saving realised.

But this brings up the second problem: Even when customers can afford a new product, climate tech startups face a long and arduous process in getting a buy-in for solutions that are relatively untested and have a limited track record. Even if a small enterprise, such as a kirana store, has suitable funds, they tend to be averse to risking it to purchase a device, such as a newly introduced solar refrigerator, that in their minds may or may not work.

This leads to a delay or avoidance of purchase decisions, which when occurring at the early-stage of adoption, often determines success or failure for a startup.

Climate asset financing can help scale adoption

The answer to our customer’s dilemma is asset finance. It is a time-tested tool of finance for buying homes, cars and electronics. Even in solar energy, asset financing is a common instrument customers sign a power purchase agreement and, instead of buying the asset upfront, pay for the results of setting up the power plant.

If we can create similar financing structures for energy efficiency, alternative heating and cooling solutions, and decarbonised industrial processes, climate adoption can scale rapidly. However, the reason we do not see a mushrooming of climate asset financiers is due to two key challenges.

The first is that of credit and default track records. Home finance companies and vehicle financiers are able to quite accurately predict expected losses and defaults, from decades of data and experience in customer behaviour and loan repayments. As climate assets and markets are new, no such data exists for these solutions it is more convenient to classify them as high risk, making the lending rates unaffordable.

The second challenge is the lack of performance data over long periods for the assets themselves. If we cannot accurately predict how an asset will perform in a few months or years, the asset financiers cannot put a value to any assets they reclaim on default, or build an active second-hand market to redeploy those assets.

These challenges create an opportunity for risk capital and early investors, and needs to go beyond just the availability of capital. The climate innovation startup and the asset financier can work together to create an integrated ecosystem, namely: 1. A credit guarantee from impact funders or grant providers to kickstart asset financing for new segments and to build a track record of credit performance to a point where it is large enough for commercial credit. 2. Buyback and redeployment contracts with climate startups until an active second-hand market can be developed for climate assets, where, in the event of non-payment by a customer, the asset can be redeployed to another adopter.

Conclusion

India is going to need more than $100 billion in climate investment every year until 2030. This investment is going to be one of the most critical and foundational steps towards achieving net-zero targets. For adoption at scale to happen faster, the key financing instrument will be asset financing, not private equity. Affordable asset financing is where India’s climate finance focus needs to shift towards.