The 34-year-old takes us to 2014. The engineer from one of the top colleges co-founded a ‘consumer’ startup—he doesn’t want to disclose either the name of the segment or the venture—which had the potential to be disruptive and change the dynamics of the consumer market. A premium school background, a promising service and an impressive storytelling…the rookie founder tapped into his alum network, and quickly found backers, angels as well as institutional investors.

Being quick as a bunny in getting funded, though, was not magical. “That was the curtainraiser. The magic show had not yet started," says the founder who starts to reconstruct a sequence of events from his ‘not-so forgettable past’.

The cafeteria in Gurugram suddenly sees heavy footfall, soft music in the background gets lost in the loud chatter, and both of us step outside to resume the conversation.An empty bench, an inconspicuous tiny park and a muted surrounding were all that were needed to slip into the past. “It was getting loud inside my head," recalls the founder, alluding to the first year of his venture, a heady pace of growth, and an erroneous sense of confidence. “It was much more than over-confidence," he clarifies. “And you can’t blame me. Every little or big thing inflated my confidence," he adds. Brisk funding, deceptive consumer love on the back of hefty discounts, aggressive expansion, an ever-swelling team, a flashy lifestyle and a massive scale built by burning cash at an insane rate…the entrepreneur could not have wished for a better start. “All these were intoxicating and magical," he recalls.

Now the magic show started. The VCs egged the founding team to burn cash, dole out discounts, and play the land grab game. “You have to be the biggest in your segment," was the clear directive. “Don’t worry about funding," promised one of the VCs. “Just remember, you need to fail fast and move on," is what another ‘founder-friendly’ VC counselled. The founder’s ambitions got stoked.

![]() Meanwhile, the backers stayed true to their promise. More funders joined the show, the venture kept aggressively fanning out, and the topline grew furiously. “This was magic," he says, adding that the progress was surreal. “My board started calling me magician," he recalls. There was a perfect product-market fit, revenues soared, valuation jumped, and the founder started flirting with the idea of listing the company after three-four years. “Do you know how a magician pulls a rabbit out of a hat," he asks. “It happens due to sleight of hand and misdirection."

Meanwhile, the backers stayed true to their promise. More funders joined the show, the venture kept aggressively fanning out, and the topline grew furiously. “This was magic," he says, adding that the progress was surreal. “My board started calling me magician," he recalls. There was a perfect product-market fit, revenues soared, valuation jumped, and the founder started flirting with the idea of listing the company after three-four years. “Do you know how a magician pulls a rabbit out of a hat," he asks. “It happens due to sleight of hand and misdirection."

Two years later, in 2016, ‘sleight of hand’ got exposed. The startup ecosystem slipped into a down cycle of funding. Most found it tough to raise money, many were left with an alarmingly short runway, and others like the one narrating his tragic story was forced to take drastic steps. He undertook layoffs, cut advertising and marketing expenses, and downsized operations to a few cities. “My startup was gasping for breath," he recounts, alluding to the ‘breach’ of promise by his backers who declined to put in more money. “I was forced to shut down," he underlines. “The hat was empty. There was no rabbit," he says.

The painful memory of the ‘death of his first baby’ chokes his voice. He stays mum for a few minutes, tries to regain his composure and starts talking again. “My VCs called me a trickster," he says, alluding to the blame game where he was accused of years of reckless spending. “I didn’t do any financial bungling," he claims. “What would you call me—a trickster or a magician?" he asks. Magic and trick, he underlines, have a strong element of deception. Both are manipulative. “It’s only when the magician dies, you get to see a trickster," he rues.

![]() Fast forward to 2023. The Indian startup ecosystem has been rocked by a series of alleged financial irregularities. It started with GoMechanic in January. Amit Bhasin, one of the co-founders, confessed to grave errors in judgement in financial reporting. In a LinkedIn post on January 17, he outlined the stark reality faced by founders. “As entrepreneurs, we identify problems, come up with solutions, and explore every opportunity to grow those solutions to meet unmet needs. But in this instance, we got carried away," he wrote. "Our passion to survive the intrinsic challenges of this sector and manage capital took the better of us and we made grave errors in judgment. We followed growth at all costs, particularly in regard to financial reporting, which we deeply regret."

Fast forward to 2023. The Indian startup ecosystem has been rocked by a series of alleged financial irregularities. It started with GoMechanic in January. Amit Bhasin, one of the co-founders, confessed to grave errors in judgement in financial reporting. In a LinkedIn post on January 17, he outlined the stark reality faced by founders. “As entrepreneurs, we identify problems, come up with solutions, and explore every opportunity to grow those solutions to meet unmet needs. But in this instance, we got carried away," he wrote. "Our passion to survive the intrinsic challenges of this sector and manage capital took the better of us and we made grave errors in judgment. We followed growth at all costs, particularly in regard to financial reporting, which we deeply regret."

Five months later, in early June, Sanjeev Bikhchandani-backed Info Edge initiated forensic auditing into the operations of 4B Networks. Through its subsidiary Allcheckdeals India, Info Edge invested Rs288 crore in Rahul Yadav-owned 4B Networks, which comprised Rs276 crore in equity and Rs12 crore in debt. A delayed response in terms of forensic auditing has made experts question the move. “The InfoEdge management could have informed stockholders about the issues in 4B Networks while initiating the forensic audit," says -Deepak Shenoy, founder and CEO of Capitalmind, a Bangalore-based investment research and wealth management startup. However, Shenoy points out, it may not have an ideal situation for InfoEdge to comment on the issues before the audit.

![]() Meanwhile, a few weeks down the line, another case of alleged financial irregularity popped up. This time it is healthcare startup Mojocare, which was founded in May 2021, raised $20 million in Series A funding, and counted B Capital, Chiratae Ventures, Better Capital, and Peak XV (formerly Surge, Sequoia Capital India’s accelerator programme), among its backers. In a media statement, the backers pointed out that major investors of Mojocare initiated a review of the company"s financial statements. “Initial findings have uncovered financial irregularities, and it has become apparent that the business model is not sustainable due to a variety of operational and market factors," the backers reportedly said in a statement released in the third week of June.

Meanwhile, a few weeks down the line, another case of alleged financial irregularity popped up. This time it is healthcare startup Mojocare, which was founded in May 2021, raised $20 million in Series A funding, and counted B Capital, Chiratae Ventures, Better Capital, and Peak XV (formerly Surge, Sequoia Capital India’s accelerator programme), among its backers. In a media statement, the backers pointed out that major investors of Mojocare initiated a review of the company"s financial statements. “Initial findings have uncovered financial irregularities, and it has become apparent that the business model is not sustainable due to a variety of operational and market factors," the backers reportedly said in a statement released in the third week of June.

Is there anything common among GoMechanic, 4B Networks and Mojocare? A founder-turned-venture capitalist spots three common threads or words: Unsustainable business model, market factors and financial irregularities’. “All three," explains the VC who runs a small fund and doesn’t want to be named, “have been accused of these." I asked him if all these founders tricked the VCs or is there anything more to it? He starts with a disclaimer, and his plight. “Being a VC now, I can’t paint them as villains. And being a former founder, I am pained to see entrepreneurs being made scapegoat."

He starts with GoMechanic, and takes us back to period between 2019 and 2021. The story begins with the Series B round of funding in December 2019. The startup raised Rs105 crore, the round was led by Chiratae Ventures and Sequoia Capital, and the third round of institutional funding made GoMechanic the highest-funded venture in the space of tech-enabled car repairs and services. The investment, the press release underlined, would be used to support expansion into 10 more cities by the end of 2020, brand promotion and streamlining spare-parts procurement.

![]() Kushal Karwa, one of the co-founders, went ballistic in baring his unbridled ambitions. “The goal to become the largest end-to-end player in the vehicle maintenance and repair space in India is very ambitious," he stressed in the press note. The money raised, he continued, would be used to continue aggressive geographical expansion and investment in innovation to keep the startup ahead of the curve. In 2017, GoMechanic raised money from Orios Venture Partners, Kunal Bahl and Rohit Bansal.

Kushal Karwa, one of the co-founders, went ballistic in baring his unbridled ambitions. “The goal to become the largest end-to-end player in the vehicle maintenance and repair space in India is very ambitious," he stressed in the press note. The money raised, he continued, would be used to continue aggressive geographical expansion and investment in innovation to keep the startup ahead of the curve. In 2017, GoMechanic raised money from Orios Venture Partners, Kunal Bahl and Rohit Bansal.

The backers were delighted with the progress made by the young guns. “In the 12 months since Sequoia India led the Series A, the company has scaled many times on the back of its asset light network of workshops and, most importantly, built true customer love," Abhishek Mohan, the then vice president at Sequoia Capital India, remarked in the official funding announcement. “Given the massive market potential of $5B+, we are excited to see what comes next," he underlined. Mohan was not alone to be impressed with the scale. Rehan Yar Khan, managing partner at Orios Venture Partners, was effusive in his praise. “This is a true ‘garage’ startup. We are glad to have backed GoMechanic when it was little more than a plan," he said.

![]() Now, let’s jump to June 2021. GoMechanic reportedly closed FY21 at Rs 34 crore. In June, the startup raised $42 million in Series C funding led by Tiger Global Management. Existing investors such as Sequoia Capital India, Orios Venture Partners and Chiratae Ventures too participated in the round. To the backers, the performance of the company was still fascinating despite the loss of Rs27 crore in FY21. But why would anybody look at losses when there was a brighter picture to focus on? The company had a revenue of Rs57 lakh in FY17, raised an undisclosed amount from Hero Motocorp’s Pawan Munjal, and galloped to Rs34 crore in four years.

Now, let’s jump to June 2021. GoMechanic reportedly closed FY21 at Rs 34 crore. In June, the startup raised $42 million in Series C funding led by Tiger Global Management. Existing investors such as Sequoia Capital India, Orios Venture Partners and Chiratae Ventures too participated in the round. To the backers, the performance of the company was still fascinating despite the loss of Rs27 crore in FY21. But why would anybody look at losses when there was a brighter picture to focus on? The company had a revenue of Rs57 lakh in FY17, raised an undisclosed amount from Hero Motocorp’s Pawan Munjal, and galloped to Rs34 crore in four years.

The backers were betting on the young guns, a promising present and an ambitious future. “Since Sequoia Capital India first partnered with GoMechanic in 2018, the company has had a very strong growth trajectory," Abhishek Mohan, principal at Sequoia India, remarked in a press release in June 2021. GoMechanic, he underlined, had expanded geographically to several cities, made a deep foray into spares, which is a $7 billion opportunity, and the team has deployed tech across the value chain exceptionally well. “This additional growth capital will enable the company to grow faster and tap into newer opportunities," he concluded. Another backer highlighted his long association. “We invested with them at seed and every round after," Khan of Orios Venture Partners stressed.

The growth story was indeed panning out in an incredible manner. This writer did a story on GoMechanic in 2021, and was guilty of not being sceptical about the numbers shared. The company claimed that the garages it partnered with grew from 145 in Q2 of 2019 to 617 in Q2 of 2021. During the same period, the claims made about number of cars serviced was equally astonishing: 22,600 to 1.13 lakh. The growth indeed looked magical, and the company reported that operating revenue for FY22 has jumped to Rs91 crore.

Cut to June 2023. The GoMechanic founders confessed of grave errors in financial irregularities, the backers washed their hands off, and the venture was finally sold off. “Why did nobody on Earth (on the board of the startup) spot any number misreporting or exaggeration for all these years," asks the founder-turned-VC cited above. “All kept on encouraging the young founders to continue with their outrageous gambit of aggressive expansion. What were the VCs doing?" The reality, he underlines, is not in black and white. There are dominant shades of grey.

Let’s start with the first ‘shade’. Venture capital, the VC underlines, is not a patient and long-term money. It has a shelf life of seven years or so, and is founded on the principles of outsized gains. Second, though it’s a valuation game, a small jump is not what VCs look for. “Look at the valuation if Byju’s. It kept swelling at an abnormal rate, and nobody was bothered for all these years," he asks. Suddenly, he adds, market conditions have been called for muted growth, layoffs and performance which by no stretch of imagination justifies valuation.

Third, founders become willing partner to the VCs. What they, however, fail to realise is that, for VCs, their venture happens to be one of the hundreds. “He just needs one silver bullet," he says, adding that it is foolish to expect VCs to play the role of a responsible father to guide the founder. “The founder, however, needs to be a responsible son," he says, underlining that the startup happens to be the only venture of a founder. “So he/she can’t be reckless irrespective of pressure to scale, and punch above their weight," he says.

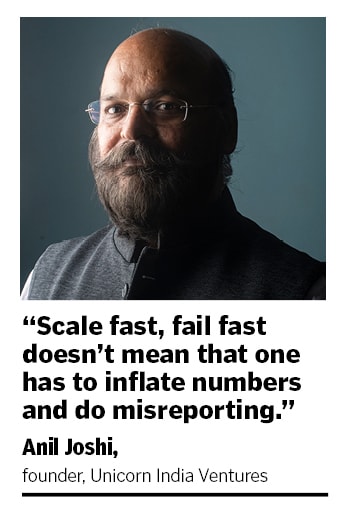

Anil Joshi explains why it would be unfair to blame the VCs. “Scale fast, fail fast doesn’t mean that one has to inflate numbers and do misreporting," says the founder of Unicorn India Ventures, a venture fund backing early-stage startups. VC money, he underlines, has to be used to grow and not indulge in malpractices. “I can understand that one has to live up to the valuation but do all startups indulge in financial irregularities?" he asks. “If not, then why blame the VC model?"

Interestingly, GoMechanic was not the only case of alleged financial irregularities. In 2022, more skeletons that tumbled out of the closet in the cases of Trell, BharatPe and Zilingo. Stunned by the widescale filth that the low tide of funding had bared, Sequoia Capital posted a blog— ‘Corporate Governance: The Cornerstone of an Enduring Company’—in April. “Recently some portfolio founders have been under investigation for potential fraudulent practices or poor governance. These allegations are deeply disturbing. We have always strongly encouraged founders to play the long game. We focus on the enduring, and discourage focussing on vanity metrics," the post said.

Taking on the critics who pointed out lack of due diligence by the VCs, the blog post made a case to cut some slack. “Let’s remember that when investments are made at seed or early stage, there is hardly a business to diligence," the post underlined. Even later-stage investors can face negative surprises, post investment, if there is wilful fraud and intent, it highlighted.

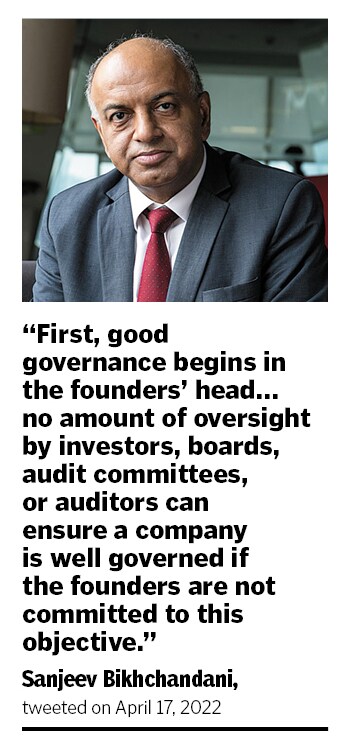

The message was appreciated by everybody in the ecosystem. Sanjeev Bikhchandani commented on Sequoia’s blog. “First, good governance begins in the founders’ head," he tweeted on April 17. “No amount of oversight by investors, boards, audit committees, or auditors can ensure a company is well governed if the founders are not committed to this objective."

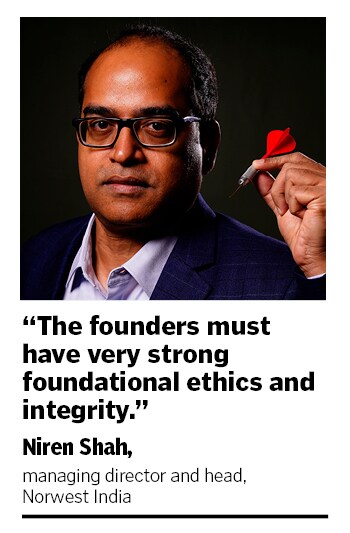

Commentators, analysts and VCs are unanimous in denouncing the act perpetrated by some of the founders. “It"s a lot about ethics and integrity," reckons Niren Shah, managing director and the head of Norwest India. All kinds of unethical practices, he adds, has a lot to do with the way young founders are mentored and educated. The investors need to make it clear that there are red lines which can’t be crossed. “Founders must have very strong foundational ethics and integrity," he says.

![]() Agrees Asish Mohapatra the co-founder and CEO of OfBusiness. “The values can’t be compromised," says the VC-turned-entrepreneur. “The values have to be inbuilt in a founder. If they go missing, I don’t know what to say."

Agrees Asish Mohapatra the co-founder and CEO of OfBusiness. “The values can’t be compromised," says the VC-turned-entrepreneur. “The values have to be inbuilt in a founder. If they go missing, I don’t know what to say."

Mohapatra explains how a founder falls in the trap. “The problem lies in a gross mismatch between what you can do and what your business can do," he says. While people are hungry to succeed, every business is not built to support that kind of hunger. “Every venture can’t have a hockey-stick growth. Simple," he says. An investor will give money and will have his expectations. “But it is the entrepreneur’s job to manage everything," he adds.

The buck indeed stops with the founder. Unless the entrepreneurs are committed to good corporate practices since the beginning, no steps taken by PEs, VCs, the auditors or the board can ensure that a startup is well governed and compliant with laws. “The ultimate responsibility lies in the hands of the founders," says Mayank Mehta, partner at Pioneer Legal, a Mumbai-based law firm.

Piyush Sharma, who heads leadership centre at IIM-Ahmedabad, too, echoes a similar emotion. The principle of a healthy balance between the interests of different stakeholders, including the promoters, shareholders, employees, and customers, is at the heart of corporate governance. “By striking a balance between the short and the long term, the credibility and transparency can be ensured," he says. The recent controversies, he underlines, have highlighted the demand for strong corporate governance in Indian businesses. “A regulatory body and regulations need to be in place," Sharma adds.

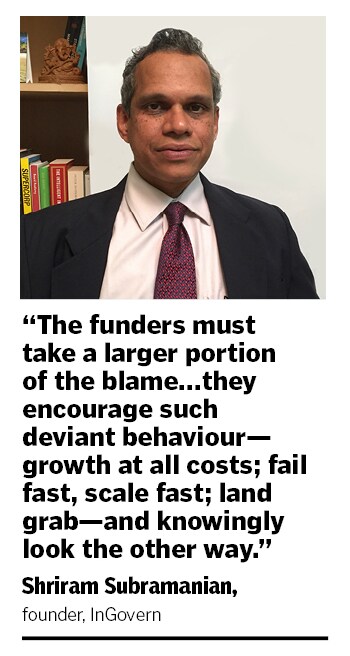

Amid the loud chorus clamouring to go hard against the erring founders, there is a strong voice that points to the other side of the coin, and deliver an unambiguous message: Froth leads to fraud. “The PEs and VCs must take a larger portion of the blame for this mess," says Shriram Subramanian, founder at InGovern, a corporate governance advisory firm. “At the end of the day, they encourage such deviant behaviour—growth at all costs fail fast, scale fast land grab--and knowingly look the other way," he says.

The genesis of the problem lies in the good heady days of funding. The venture gets excessive money, is over-valued and is being prepped for the next round of funding and valuation. The cycle keeps getting built up until the funding down-cycle hits. “Only when the tide goes out do you discover who"s been swimming naked," says Subramanian quoting legendry investor Warren Buffet. “GoMechanic and other recent examples are just the beginning. The real pain is yet to come out."

Meanwhile, a founder in Bengaluru shares his side of untold pain. “They (VCs) asked me to throw all caution out of the window," says the entrepreneur with a struggling venture. The original business plan was to grow slowly, but the backers wanted a steroid-led growth. “Don’t make it a lifestyle business. It has to have immense scale," was the decree to the founder who had to play a different game that needed to hire talent at all costs. The outcome was poaching at irrational salary. “I knew I was riding a tiger, but there was no option," rues the founder requesting anonymity. The expenses got bloated, funding winter set in, and largescale layoffs emerged as the only survival choice. “Now we are just buying more time," he says.

In Delhi-NCR, one gets to hear another interesting tale. This time again, the narrator is a founder. “How many VCs do the diligence?" he asks. “It’s shocking but there are many who cut large cheques within minutes. And yes, there are no questions asked. You also know companies that became unicorn with either zero revenue or nothing to talk about in terms of financials," he says. If such examples are rampant, then why would a founder not get tempted or encouraged to follow the herd. “Who wants to be left out? Let’s be clear. It’s a dog-eats-dog world. If I don’t bend the rules, others will and race ahead."

Back in Gurugram, the second-time founder has a piece of advice for his fellow entrepreneurs. “Don’t try to be a magician," he says, adding that the temptation will always be there. “But if you decide to dance with the devil, you will pay the price," he says. “It’s all about choices we make. I made the wrong choice, I paid a heavy price," he regrets.

Meanwhile, the backers stayed true to their promise. More funders joined the show, the venture kept aggressively fanning out, and the topline grew furiously. “This was magic," he says, adding that the progress was surreal. “My board started calling me magician," he recalls. There was a perfect product-market fit, revenues soared, valuation jumped, and the founder started flirting with the idea of listing the company after three-four years. “Do you know how a magician pulls a rabbit out of a hat," he asks. “It happens due to sleight of hand and misdirection."

Meanwhile, the backers stayed true to their promise. More funders joined the show, the venture kept aggressively fanning out, and the topline grew furiously. “This was magic," he says, adding that the progress was surreal. “My board started calling me magician," he recalls. There was a perfect product-market fit, revenues soared, valuation jumped, and the founder started flirting with the idea of listing the company after three-four years. “Do you know how a magician pulls a rabbit out of a hat," he asks. “It happens due to sleight of hand and misdirection." Fast forward to 2023. The Indian startup ecosystem has been rocked by a series of alleged financial irregularities. It started with GoMechanic in January. Amit Bhasin, one of the co-founders, confessed to grave errors in judgement in financial reporting. In a LinkedIn post on January 17, he outlined the stark reality faced by founders. “As entrepreneurs, we identify problems, come up with solutions, and explore every opportunity to grow those solutions to meet unmet needs. But in this instance, we got carried away," he wrote. "Our passion to survive the intrinsic challenges of this sector and manage capital took the better of us and we made grave errors in judgment. We followed growth at all costs, particularly in regard to financial reporting, which we deeply regret."

Fast forward to 2023. The Indian startup ecosystem has been rocked by a series of alleged financial irregularities. It started with GoMechanic in January. Amit Bhasin, one of the co-founders, confessed to grave errors in judgement in financial reporting. In a LinkedIn post on January 17, he outlined the stark reality faced by founders. “As entrepreneurs, we identify problems, come up with solutions, and explore every opportunity to grow those solutions to meet unmet needs. But in this instance, we got carried away," he wrote. "Our passion to survive the intrinsic challenges of this sector and manage capital took the better of us and we made grave errors in judgment. We followed growth at all costs, particularly in regard to financial reporting, which we deeply regret." Meanwhile, a few weeks down the line, another case of alleged financial irregularity popped up. This time it is healthcare startup Mojocare, which was founded in May 2021, raised $20 million in Series A funding, and counted B Capital, Chiratae Ventures, Better Capital, and Peak XV (formerly Surge, Sequoia Capital India’s accelerator programme), among its backers. In a media statement, the backers pointed out that major investors of Mojocare initiated a review of the company"s financial statements. “Initial findings have uncovered financial irregularities, and it has become apparent that the business model is not sustainable due to a variety of operational and market factors," the backers reportedly said in a statement released in the third week of June.

Meanwhile, a few weeks down the line, another case of alleged financial irregularity popped up. This time it is healthcare startup Mojocare, which was founded in May 2021, raised $20 million in Series A funding, and counted B Capital, Chiratae Ventures, Better Capital, and Peak XV (formerly Surge, Sequoia Capital India’s accelerator programme), among its backers. In a media statement, the backers pointed out that major investors of Mojocare initiated a review of the company"s financial statements. “Initial findings have uncovered financial irregularities, and it has become apparent that the business model is not sustainable due to a variety of operational and market factors," the backers reportedly said in a statement released in the third week of June. Kushal Karwa, one of the co-founders, went ballistic in baring his unbridled ambitions. “The goal to become the largest end-to-end player in the vehicle maintenance and repair space in India is very ambitious," he stressed in the press note. The money raised, he continued, would be used to continue aggressive geographical expansion and investment in innovation to keep the startup ahead of the curve. In 2017, GoMechanic raised money from Orios Venture Partners, Kunal Bahl and Rohit Bansal.

Kushal Karwa, one of the co-founders, went ballistic in baring his unbridled ambitions. “The goal to become the largest end-to-end player in the vehicle maintenance and repair space in India is very ambitious," he stressed in the press note. The money raised, he continued, would be used to continue aggressive geographical expansion and investment in innovation to keep the startup ahead of the curve. In 2017, GoMechanic raised money from Orios Venture Partners, Kunal Bahl and Rohit Bansal. Now, let’s jump to June 2021. GoMechanic reportedly closed FY21 at Rs 34 crore. In June, the startup raised $42 million in Series C funding led by Tiger Global Management. Existing investors such as Sequoia Capital India, Orios Venture Partners and Chiratae Ventures too participated in the round. To the backers, the performance of the company was still fascinating despite the loss of Rs27 crore in FY21. But why would anybody look at losses when there was a brighter picture to focus on? The company had a revenue of Rs57 lakh in FY17, raised an undisclosed amount from Hero Motocorp’s Pawan Munjal, and galloped to Rs34 crore in four years.

Now, let’s jump to June 2021. GoMechanic reportedly closed FY21 at Rs 34 crore. In June, the startup raised $42 million in Series C funding led by Tiger Global Management. Existing investors such as Sequoia Capital India, Orios Venture Partners and Chiratae Ventures too participated in the round. To the backers, the performance of the company was still fascinating despite the loss of Rs27 crore in FY21. But why would anybody look at losses when there was a brighter picture to focus on? The company had a revenue of Rs57 lakh in FY17, raised an undisclosed amount from Hero Motocorp’s Pawan Munjal, and galloped to Rs34 crore in four years. Agrees Asish Mohapatra the co-founder and CEO of OfBusiness. “The values can’t be compromised," says the VC-turned-entrepreneur. “The values have to be inbuilt in a founder. If they go missing, I don’t know what to say."

Agrees Asish Mohapatra the co-founder and CEO of OfBusiness. “The values can’t be compromised," says the VC-turned-entrepreneur. “The values have to be inbuilt in a founder. If they go missing, I don’t know what to say."