This perfect storm had resulted in the market pummelling their stocks. The listed universe (except for AU Small Finance Bank, the largest of its type) traded at or below book value. In effect, the market was valuing these businesses only on the basis of the cash they had today. Simply put, it was unwilling to pay for future profits.

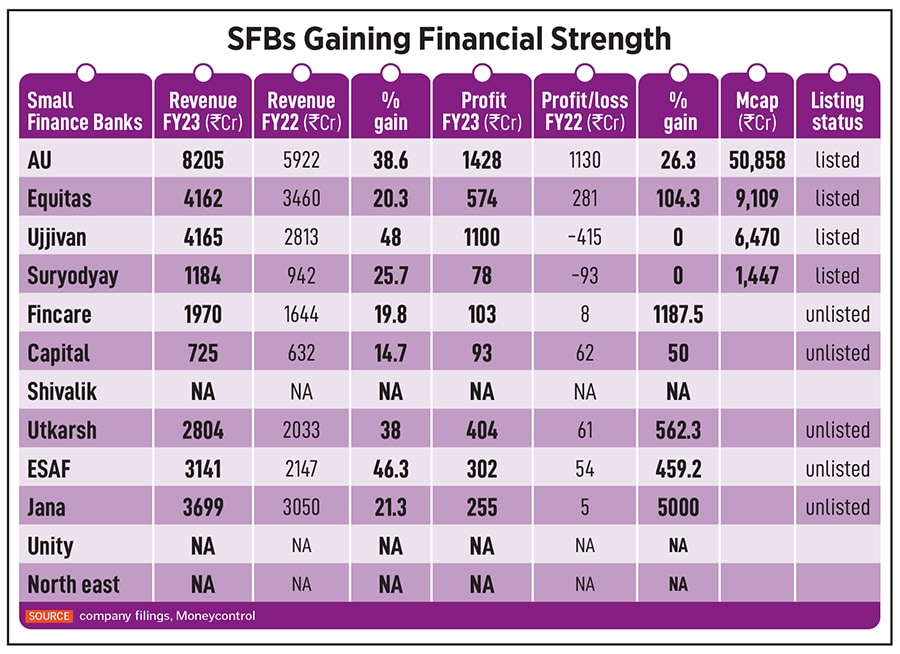

Fast forward to the fiscal gone by and these banks have staged a sharp recovery. “Most of these SFBs still have a reasonably large microfinance portfolio and the key reason for their performance being better is the improvement in the operating dynamics of that sector," says Krishnan Sitaraman, senior director and chief ratings officer at CRISIL Ratings. Net non-performing assets are down sharply for the sector and profitability has rebounded aided in part by write backs (see chart). An improving business environment could see the banks doing a lot better in FY24. The market has in the last month started pricing in future growth.

Equitas SFB hit a record net profit of Rs190 crore for the quarter ended March 31, as loan disbursements grew by 80 percent in the quarter. The smaller Suryoday SFB swung into a net profit of Rs50.2 crore, against a net loss of Rs63.6 crore in the March-ended quarter, reflecting investor confidence in the bank. Suryoday now trades at Rs139, close to its 52-week intra-day high of Rs140 on May 17. Same for Equitas. At Rs82, it trades at its highest ever price. The stock has doubled in the last year and the market now values it at 2.5 times book value.

Rival Ujjivan SFB has also seen a year-on-year 145 percent jump in net profit to Rs309.5 crore, on revenues of Rs1,364 crore. Banks have also used this opportunity to diversify beyond their core microfinance offering. Personal loans, financial institutional group (FIG) lending and housing reflected the sharpest annual growth. AU SFB (AU and Capital SFB are the only two banks with no microfinance portfolio) beat analysts’ expectations with a 23 percent y-o-y jump in net profit of Rs424.6 crore for the same March-ended quarter.

![]()

The middle-income specialist

This is also the time when banks are further honing (and differentiating) their business strategies. Take, for instance, Capital Small Finance Bank. The Jalandhar-based bank was the first SFB to receive a licence. Prior to that, it was a local area bank operating in three districts of Punjab. The bank started spreading its operations across Punjab and in the last five years has grown its income from Rs293 crore to Rs725 crore—a growth of 19.8 percent a year. In the same period, profits have moved up from Rs19 crore to Rs93 crore—a growth of 37 percent a year. Net worth has climbed from Rs232 crore to Rs610 crore. Asset quality has been stable through the pandemic with a net NPA ratio of 1.4 percent over the last three fiscals.

The bank realises it cannot be all things to all people, and it would have its task cut out in competing with large universal banks due to their lower cost of funds. “We aim to be a middle-income specialist," says Munish Jain, chief financial officer at Capital Small Finance Bank. The bank will aim to cater to customers with income of Rs4-40 lakh per year and build a relationship on both the asset and liability side. “This way we get an early warning if something is going wrong with the customer," he tells Forbes India. It plans to expand close to Punjab where it has a majority of its branches. Its next target is to turn Haryana into a similar success story as Punjab. It also has a presence in Himachal Pradesh, Delhi and Rajasthan.

With the 97.9 percent retail-centric deposit franchise and a CASA (current and savings account) ratio of 42 percent in FY23, it is better placed than several mid-sized regional banks.

Capital SFB’s managing director and CEO Sarvjit Singh Samra believes that as the SFB expands into other states, it would retain its focus of serving those in the semi-urban and rural regions. The team is quite likely to retain its customer-centric focus, with a strategy to bring the “customer’s cash flows towards the bank". All of this would help Capital climb in the preferred wallet space of its customer base.

![]() Keyur Doshi, CFO, Fincare Small Finance Bank

Keyur Doshi, CFO, Fincare Small Finance Bank

From microfinance to secured lending

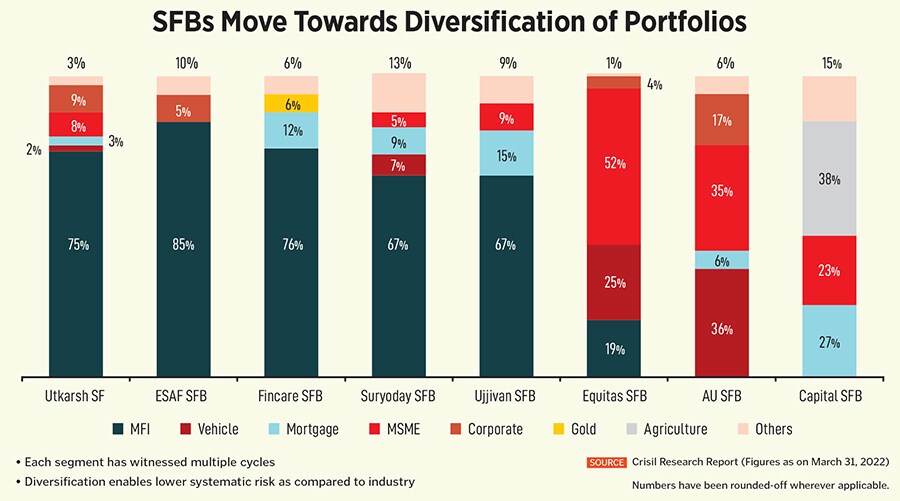

The legacy of several SFBs, who have emerged from being microfinance lenders, has meant that a majority of their loan book is skewed towards microfinance or MSME loans. Both these portfolios of unsecured loans are harder to make recoveries from when the cycle turns for the worse. Borrowers ask for moratoriums and the new norms from the Reserve Bank of India (RBI) mean instalments must be paid fully before the loan is classified as current.

Unlisted Fincare SFB—which was predominantly a microfinance-focussed entity—has been diversifying its book further to reduce its dependence on this one segment. When Disha Microfin (rechristened Fincare) got a banking licence in March 2017, it had just a 6 percent unsecured lending book and the majority 94 was unsecured (microfinance). This has now become a little more balanced 39:61 percent, but with the majority still unsecured.

Fincare SFB’s CFO Keyur Doshi believes the bank has crossed the phase of “being overdependent on the microfinance sector". “The MFI sector faced three crises in the last 12 years, but there is an underlying fact that this business has proved to be scalable, economically viable and for social good. One cannot eye this sector from just a limited commercial angle. The sector is slowly evolving, and the joint liability group concept is also getting evolved," he tells Forbes India.

![]()

With its roots in microfinance, Fincare’s focus to serve the base-of-the-pyramid customers will continue. “But the journey of being a bank will also evolve. From a predominant MFI-driven entity, we will be going towards a secured business. Over the next three to five years, the unsecured part of the book will go down and secured book will go up. The journey is halfway and there will be further progress. The plan is to grow the secured book at a faster pace than the unsecured one. Secured products would allow us to build a more diversified lending portfolio," Doshi says. He is, however, less inclined to share a specific target for the dilution in the microfinance activity.

Fincare SFB has about Rs9,911 crore of assets and Rs8,033 crore of deposits, as of FY23. It operates 1,231 banking outlets in 19 states and three Union Territories, serving 4.5 million clients.

The RBI, too, from a perspective of lowering risks for lending institutions, in March last year, granted microfinance firms the ability to lend more towards segments beyond microfinance, by reducing the minimum limit of microfinance loans of total loan assets to 75 percent. This has automatically allowed lending institutions to get a more balanced lending portfolio and lower their exposure to MFI-related risks. As a result, most SFBs are now in the process of reducing their microfinance exposure.

Seeking growth capital

Of the 12 SFBs that came up mainly through the microfinance route, a few have been able to reduce the cost of their borrowings, diversify into new business areas (commercial vehicle loans, small business loans, personal and gold loans) and take small steps towards becoming universal banks. The RBI mandates that a new SFB must have 25 percent of its total branches opened during the year in rural areas. They also need to allocate 40 percent of their overall advances towards priority sector lending.

In the current setup, among the 11 banks, the North East Small Finance Bank (concentrated in the seven Northeastern states of India and North Bengal) and Shivalik Small Finance Bank—which transitioned from a co-operative bank—are the two which might be limited in their reach or structure, to expand in a rapid manner. The two have no known plans to tap the capital market.

![]() Capital Small Finance Bank"s Jagraon branch in Punjab

Capital Small Finance Bank"s Jagraon branch in Punjab

But for the others, with business models largely intact, some of the SFBs, including Fincare, Capital, ESAF and Jana SFBs, have plans to list in the coming years. As per RBI norms, SFBs have to list within three years of reaching a net worth of Rs500 crore.

In May, Fincare refiled its draft red herring prospectus (DRHP) with the regulator Securities and Exchange Board of India (Sebi), seeking to raise Rs625 crore through a fresh issue and an offer for sale (OFS) of 1.7 crore equity shares by the promoter and investors. The exact timeline for the offering was not disclosed, but it is likely that the bank will not go for another round of private market funding.

Jain and Samra say Capital SFB plans for a listing, but will wait for the “markets to get stabilised". The bank had filed its red herring prospectus, but the one-year timeline to list expired in February. In the meantime, Capital plans for a smaller offering to private equity investors. “We are looking for growth capital rather than regulatory capital," Jain says. In April, the bank raised Rs64 crore from a host of investors, including Max Life Insurance, Amicus Capital and Pi Ventures. The fundraising was made easier by a stellar performance in FY23 as well as a 5.1 percent cost of funds (the lowest among any SFB) that allows the bank to be as competitive with its loan products as its larger rivals. ESAF SFB has also filed its DRHP with Sebi.

Most SFBs are well-capitalised at this stage, with a capital adequacy ratio in the 23 to 30 percent range for the listed small finance banks, much higher than the 15 percent capital adequacy ratio (CAR) mandated by the RBI. So, they could wait for some more time until investors start to appreciate the SFB story better.

The shift towards a secured lending book will obviously reduce risks for these banks. And a diversified portfolio will bring some amount of predictability and durability to an SFB’s earnings. If some of these smaller SFBs can replicate their recent successes as they expand operations to other states, it will boost the confidence of their potential investors and price them at par with their (much) larger rivals.