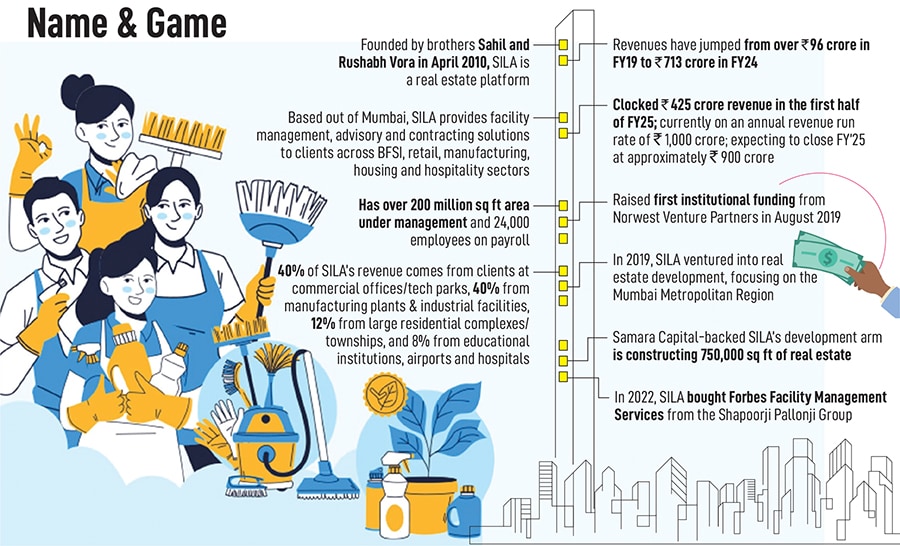

SILA: Slowly, steadily and sustainably building a business

Brothers Sahil and Rushabh Vora bootstrapped their entrepreneurial journey for nearly a decade, embraced value, shunned valuation and befriended KPIs that remain alien to most new-age founders. The re

(left)Sahil Vora, founder, SILA and Rushabh Vora, Co-founder & Managing director, SILA

Image: Mexy Xavier

Advertisement

Mumbai, 2015. For the seasoned squash players, it was a grave unforced error. It was 2015. Brothers Sahil and Rushabh Vora were in the fifth year of their bootstrapped entrepreneurial journey with their maiden venture SILA, a real estate platform with facility management at its core. “When we started in 2010, the world of angel investing was not institutionalised," recalls Rushabh, a national squash player and an investment banker who had stints with Lazard, UBS and BGS Partners. The brothers, therefore, tapped into their network of friends and family, an uncle chipped in with an initial corpus of ₹50 lakh, and paid the amount in multiple tranches of ₹5 lakh.

The staggered payment did wonders on multiple counts. First, it reinforced the value of navigating a tight ship. Second, it underlined the urgency of running a profitable business. Third, it underscored the need to build a sustainable venture. Months passed by and the brothers stayed firm on the proven entrepreneurial path of slow and steady progress. By 2015, SILA clocked an operating revenue of ₹30 crore, the B2B business continued to grow profitably, and the siblings squashed all temptations to play a valuation game. “We were not burning and growing. It’s not in our DNA," recounts Sahil, adding that the B2B venture never needed extra money. The brothers were happy with their B2B drives and volleys.

Then, sometime in 2015, the duo did something uncharacteristic: An unforced error. Rushabh goes down memory lane and recounts the lone forgettable blip. “There was this one ‘comment’ from a friend, and we yielded to the temptation," he says. The remark from a well-wisher was meant to jolt the brothers from their inertia of a bootstrapped life. “You have over 1,800 employees, your revenue is around ₹30 crore, and you haven’t raised a single VC penny," was the innocuous-yet-provocative taunt. “Guys, what are you doing? Look, what is happening around you," was how the well-wisher exhorted the Vora brothers to make the most of the funding boom.

The siren song charmed the brothers. “We started a B2C business—Mr Homecare—for home cleaning and deep services," recounts Sahil. The plan was to replicate the magic of the B2B venture, but with a twist: Raise VC money, grow aggressively, and scale furiously. Within three weeks, the duo raised money from friends and family, were in talks with a bunch of venture capitalists for institutional funding, and over the next few months, the B2C blueprint unfurled itself in full glory. After six months, the siren song morphed into loud warning bells. “We quickly realised that B2C is not in our DNA," he underlines. Reason? High burn and insane customer acquisition cost. The cost per click on Google was around ₹170! “The economics didn’t sit well with our bootstrapped genes," he says, adding that the venture was shuttered in nine months. “Continuing with it didn’t make any sense," Rushabh chips in with his take. The KPIs (key performance indicators), he underlines, were negatively and heavily skewed. “We would not have made money at all," he says.

Cut to November 2024. The brothers have made money—and it’s not paper money—and built a profitable and sustainable real estate platform. “We chase value and not valuation," says Sahil. Look at the report card of SILA. Started in 2010, the company reached ₹30 crore in topline in the first five years. Four years later, by FY19, the operating revenue increased to ₹96 crore. Patience paid off, the grunt work reaped rich dividends as the much-awaited inflection point came after the pandemic in 2020. Revenue leapfrogged from ₹230.7 crore in FY22 to ₹514.4 crore in the next fiscal.

SILA soon hit a purple patch. The juggernaut continued for the Mumbai-based real estate platform that provides facility management, advisory, and contracting solutions to clients across BFSI (banking, financial services, and insurance), retail, manufacturing, housing, and hospitality sectors. The revenues pole-vaulted to ₹713 crore in FY24 and are now striking a run-rate of ₹900 crore in FY25. The bottom line too charted a positive trajectory during the period (see box). “As a B2B business, we may not look or sound sexy, but for us, the numbers do the talking," says Sahil. His brother chips in. “It (nature of the business) may be boring, but it makes a lot of sense," reckons Rushabh.

The numbers are indeed impressive. What is fascinating though is that the brothers didn’t raise much venture capital to fuel their business. SILA had a nominal first round of institutional funding in 2019, and then added some more dry powder to the kitty in 2022 when it bought Forbes Facility Management Services from the Shapoorji Pallonji Group reportedly for ₹42 crore. “We’re a B2B business. And we didn’t spend heavily on marketing, advertising and customer acquisition," says Sahil. All that the brothers were supposed to do—and they did it diligently—was to ensure a high quality of service and a razor-sharp focus on customers. What also helped in the process was sound financial knowledge. “We knew how to read a balance sheet and we were also prudent," he says.

Other ingredients too came in handy. Take, for instance, a large TAM (total addressable market). “Luckily for our business, the market size is big," says Rushabh, as he decodes the magical growth of SILA. From large multinationals to domestic corporates—small, mid-sized, and big—to an R&D centre, a manufacturing unit, and anybody with an office—all needed facility management, advisory, and contracting solutions. High-quality work resulted in wide word-of-mouth marketing as a lot of customers came from referrals. “We slowly built those blocks which helped in keeping marketing dollars low," he says, adding that the big TAM was also helped by another strong trend of the unorganised sector moving towards the organised counterparts. Labour compliances were becoming critical and the contracting world saw the disappearance of mom-and-pop and cottage players.

Two more factors shaped the journey. First, the brothers maintained fiscal discipline in running a tight ship. There was no point in throwing money at the business and the problem. “There was and there is no reason to believe that doing so would make the business more efficient," says Rushabh. Second, befriending a clutch of alien KPIs during the journey proved beneficial. Sahil explains. ROE (return on equity), ROCE (return on capital employed), OCF (operating cash flow), and D/E (debt-to-equity) ratio became as crucial as operating revenue and profit after tax. These terms, he underlines, may sound jarring but these are what make or break a business. While the first five years of the journey were focussed on building trust, and credibility, and garnering revenue, the next five years were spent on fine-tuning profits. Over the next few years, he underscores, the focus will shift from profit to generating more cash flow.

Okay. But how does one explain wafer-thin PAT? On revenue of over ₹713 crore, the PAT (profit after tax) in FY24 was just ₹9.1 crore. In fact, the PAT has remained low in previous fiscals as well. Rushabh explains. FY24 PAT, he underlines, had several one-time adjustments for non-cash/non-operating items such as ESOP expenses and restating accounts. “This is not a true representation of the actual operating business," he says, sharing a quirky intrinsic aspect of the facility management business. “It’s a low margin, high volume, annuity business," he says, adding that the margins perpetually remain thin. SILA’s contract retention rate is north of 95 percent, the company doesn’t have to fight for a contract every year, and it has been growing incrementally. “The compounding nature of our business is what makes it fascinating and lucrative," he adds.

The backers are delighted with the sustainable and profitable growth of SILA. “The company has delivered around 10x revenue growth during our hold period," says Shiv Chaudhary, managing director of Norwest India. The brothers, he adds, have built the company profitably and with high capital efficiency. Having played squash for India at a young age, the siblings have demonstrated grit and hard work early in their lives. What, though, is commendable about the growth is a holistic approach. Corporate governance, risk management, systems, and processes have been the core areas of focus at SILA. “What’s more important is the longevity of growth and the reliability of growth," says Chaudhary, adding that while longevity provides investors the opportunity to compound their money, reliability provides safety and security. The challenge, though, for SILA would be the manpower-intensive nature of the business. “They will have to continue to invest in systems, processes, and technology," he reckons.

The brothers, meanwhile, point out a different challenge. “What we want to do is to continue doing a boring and predictable business," says Sahil. Reason? The public markets value such companies. They want predictability, profitability, and sustainability. “We’re planning to go public in six to eight quarters," he says, adding that SILA would continue with its high compliance and governance. The brothers don’t want to reinvent the business wheel. “Revenue is vanity, profit is sanity, and cash reality… and we want to stick to these basics," says Rushabh as he signs off with an intent to double down on his ‘boring’ business.

Cut to November 2024. The brothers have made money—and it’s not paper money—and built a profitable and sustainable real estate platform. “We chase value and not valuation," says Sahil. Look at the report card of SILA. Started in 2010, the company reached ₹30 crore in topline in the first five years. Four years later, by FY19, the operating revenue increased to ₹96 crore. Patience paid off, the grunt work reaped rich dividends as the much-awaited inflection point came after the pandemic in 2020. Revenue leapfrogged from ₹230.7 crore in FY22 to ₹514.4 crore in the next fiscal.

Cut to November 2024. The brothers have made money—and it’s not paper money—and built a profitable and sustainable real estate platform. “We chase value and not valuation," says Sahil. Look at the report card of SILA. Started in 2010, the company reached ₹30 crore in topline in the first five years. Four years later, by FY19, the operating revenue increased to ₹96 crore. Patience paid off, the grunt work reaped rich dividends as the much-awaited inflection point came after the pandemic in 2020. Revenue leapfrogged from ₹230.7 crore in FY22 to ₹514.4 crore in the next fiscal. Other ingredients too came in handy. Take, for instance, a large TAM (total addressable market). “Luckily for our business, the market size is big," says Rushabh, as he decodes the magical growth of SILA. From large multinationals to domestic corporates—small, mid-sized, and big—to an R&D centre, a manufacturing unit, and anybody with an office—all needed facility management, advisory, and contracting solutions. High-quality work resulted in wide word-of-mouth marketing as a lot of customers came from referrals. “We slowly built those blocks which helped in keeping marketing dollars low," he says, adding that the big TAM was also helped by another strong trend of the unorganised sector moving towards the organised counterparts. Labour compliances were becoming critical and the contracting world saw the disappearance of mom-and-pop and cottage players.

Other ingredients too came in handy. Take, for instance, a large TAM (total addressable market). “Luckily for our business, the market size is big," says Rushabh, as he decodes the magical growth of SILA. From large multinationals to domestic corporates—small, mid-sized, and big—to an R&D centre, a manufacturing unit, and anybody with an office—all needed facility management, advisory, and contracting solutions. High-quality work resulted in wide word-of-mouth marketing as a lot of customers came from referrals. “We slowly built those blocks which helped in keeping marketing dollars low," he says, adding that the big TAM was also helped by another strong trend of the unorganised sector moving towards the organised counterparts. Labour compliances were becoming critical and the contracting world saw the disappearance of mom-and-pop and cottage players. Okay. But how does one explain wafer-thin PAT? On revenue of over ₹713 crore, the PAT (profit after tax) in FY24 was just ₹9.1 crore. In fact, the PAT has remained low in previous fiscals as well. Rushabh explains. FY24 PAT, he underlines, had several one-time adjustments for non-cash/non-operating items such as ESOP expenses and restating accounts. “This is not a true representation of the actual operating business," he says, sharing a quirky intrinsic aspect of the facility management business. “It’s a low margin, high volume, annuity business," he says, adding that the margins perpetually remain thin. SILA’s contract retention rate is north of 95 percent, the company doesn’t have to fight for a contract every year, and it has been growing incrementally. “The compounding nature of our business is what makes it fascinating and lucrative," he adds.

Okay. But how does one explain wafer-thin PAT? On revenue of over ₹713 crore, the PAT (profit after tax) in FY24 was just ₹9.1 crore. In fact, the PAT has remained low in previous fiscals as well. Rushabh explains. FY24 PAT, he underlines, had several one-time adjustments for non-cash/non-operating items such as ESOP expenses and restating accounts. “This is not a true representation of the actual operating business," he says, sharing a quirky intrinsic aspect of the facility management business. “It’s a low margin, high volume, annuity business," he says, adding that the margins perpetually remain thin. SILA’s contract retention rate is north of 95 percent, the company doesn’t have to fight for a contract every year, and it has been growing incrementally. “The compounding nature of our business is what makes it fascinating and lucrative," he adds.