Inox's mega-merger with PVR in 2022, Inox India's blockbuster listing in 2023, and a dashing report card of the listed entity in FY24... Siddharth Jain has hit a purple patch in his entrepreneurial jo

Siddharth Jain, Promoter, INOX Group

Image: Swapnil Sakhare For Forbes India

Advertisement

Mumbai, 2024. “It"s not that I bought a stock, I sold it, and I made a loss," stresses Siddharth Jain. “It was not a normal loss," he underlines, explaining the magnitude of the suffering that he endured for five years. “I just kept trying to fix, fix, fix, and then one fine day, I realised that it just can’t be fixed," rues the third-generation founder, who goes down memory lane to revisit the first big low moment in his entrepreneurial journey. “It was five years of torture… yeah, it was indeed torture," reiterates the mechanical engineer, who joined the family business of industrial gases, cryogenic engineering and entertainment in 2001. A few years later, he went on to study MBA from INSEAD in France, and then returned to India in 2006.

Three years later, in 2009, Jain was taking the boldest step of his life. “We must expand and take the brand global," he told his father Pavan Jain, who gave ample freedom to the young management grad to paint his dream on a wide canvas. “My father and family encouraged me to expand our geographical footprint," says Jain. It was a gutsy move by Inox Group which didn’t have any operations outside India till 2008.

Twelve months later, Inox India, the biggest maker of cryogenic storage and transportation equipment in the country, was all set to buy an asset in the US. “To go outside India and buy an operational plant in the US was a real bold move," reckons Jain, who was forewarned by a battery of experts, naysayers, and industry observers about the potential acquisition. “Nine out of 10 foreign acquisitions fail," they cautioned.

Jain, though, was fearless. And he had his reasons. First, he studied in America. He completed his mechanical engineering from the University of Michigan and worked in the US for two years. “So, I"d spent six years in the US. I knew the country," he reckons. Second, Jain finished his MBA from INSEAD. “I got tremendous international exposure," he says. When you deep dive into the case studies of dozens of successful and not-so-successful companies during your MBA days, he points out, they teach you one simple thing: You get to know the problems that they"ve had, and you know what to do and what not to do when you are running your venture. “I had no fear," says Jain.

Call it beginner’s luck or the firm conviction of a confident warrior, the gambit did start on a boisterous note. “We had a meteoric rise during the first few years," says Jain. In 2009, when the American company was acquired, it had 80 employees. In 2013, it had 700. “From 80 to 700 in just four years," says Jain, alluding to the pace at which the company was growing. During the same period, he points out, the revenue leapfrogged from $40 million to around $160 million. “I thought I was invincible," says Jain.

There was another prized catch for the warrior in 2012. Standard Chartered Private Equity reportedly invested Rs250 crore in Inox India. “Again, PE investment was something that our family had never done. I negotiated this deal," he says. Back-to-back heady success trapped the founder into a dangerous illusion. “I felt that am invincible… unstoppable," he says.

In five years, by 2018, the warrior was feeling vanquished. The US acquisition had become a horror show. The reasons were galore. First, when Jain bought the company in 2009, America was going through a shale gas boom. “We were making equipment that supported shale gas production," he says. In 2014, shale gas crashed in America. “Suddenly, all our orders vanished," recalls Jain, who had just doubled the capacity and ramped up investment in working capital, raw material and manpower.

Second, Jain let the original owners continue to run the show. “Though they were great guys, they were no longer the owners. We were the owners, and we were not too personally invested," he rues. “I didn"t control the business because I wanted to give operational freedom to the local people," he says. Though freedom was not abused, zero checks and balances had a serious flip side.

Third, Jain had never seen failure in life. And when you haven’t experienced failure, you are never prepared for it. “We have always seen good times," he says, adding that there was never a plan to hedge the company against loss. “We never had a bad day," he quips, adding that he tried hard to fix the problem for five long years. “This was my first big personal project," he says. Despite the writing on the wall, Jain persisted with the company because something else was also playing on his mind. “Our family is not built on the value of selling companies. We never sold a business in life," he says. “Letting it go was hard," he adds.

Two years later, the founder was gripped with a sense of deja vu. He found himself in a situation where he was emotionally torn between making a ‘hard’ and a ‘terrible’ choice. It was 2020, the country was in the grips of the pandemic, and travel, hospitality and cinema were the ones that bore the maximum brunt. All Inox multiplexes too were shut down. “We were shut for more than a year," says Jain. “We had to lay off hundreds of employees, take heavy pay cuts, and the worst part was that we didn’t have cash," rues the founder, who was faced with a grim and realistic reality of the end of the cinema business. There was too much uncertainty, and nobody knew when the viewers would flock back to theatres. Cinema was facing an existential crisis.

Meanwhile, a cruel irony was playing out in terms of the contrasting nature of the two crises. Cinema was running out of oxygen, but Inox Air Products had to continuously supply oxygen to keep people alive. On one hand, Jain had to brutally trim the headcount in the multiplex business, and on the other, he had to run his factories round the clock. “We were supplying 60 percent of India"s medical oxygen to over 800 hospitals directly," he says, alluding to the production work done by Inox Air Products, India’s largest industrial and medical gas manufacturer. Dealing with the pain of sacking employees who had been working for years, grappling with the disastrous reality of zero revenue in cinema, and ensuring that the workers in the Inox Air Products’ factories were safe was taking a heavy toll on the entrepreneur. “It was emotionally traumatic," he says.

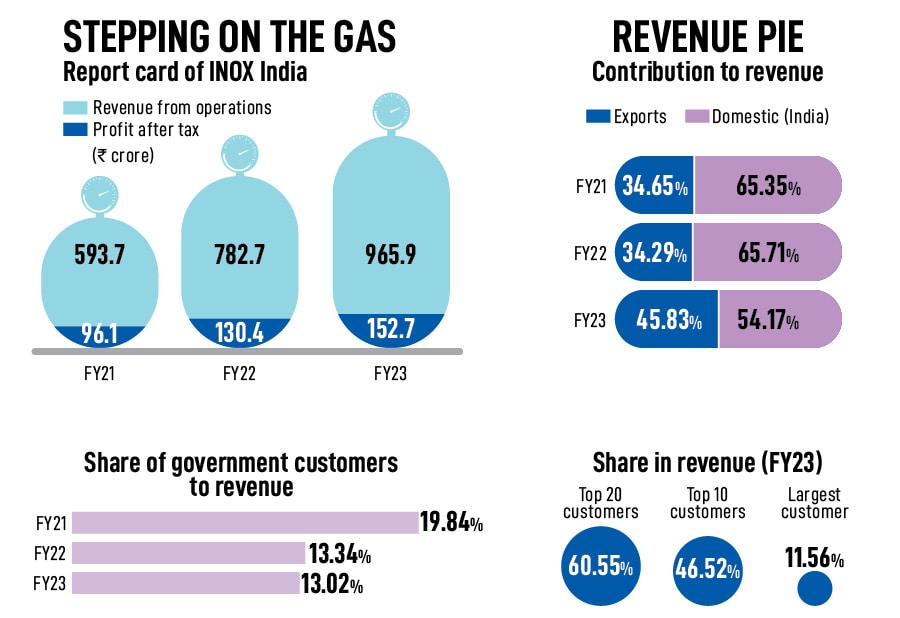

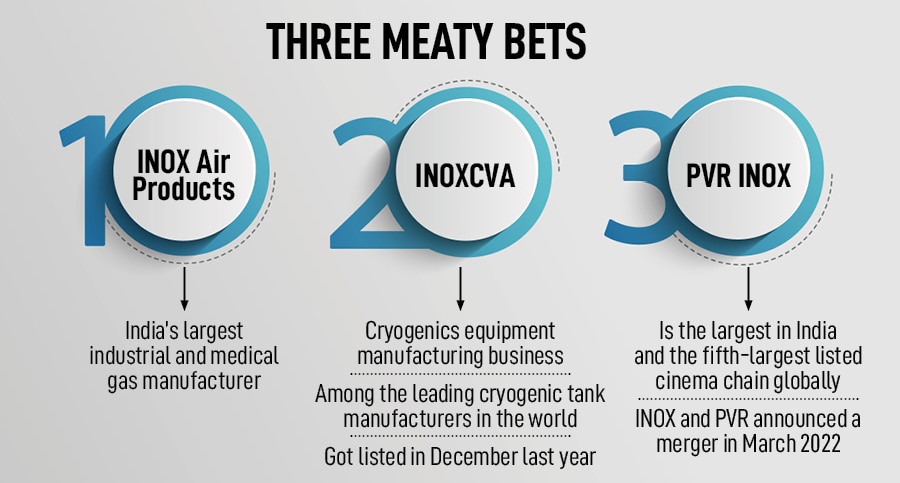

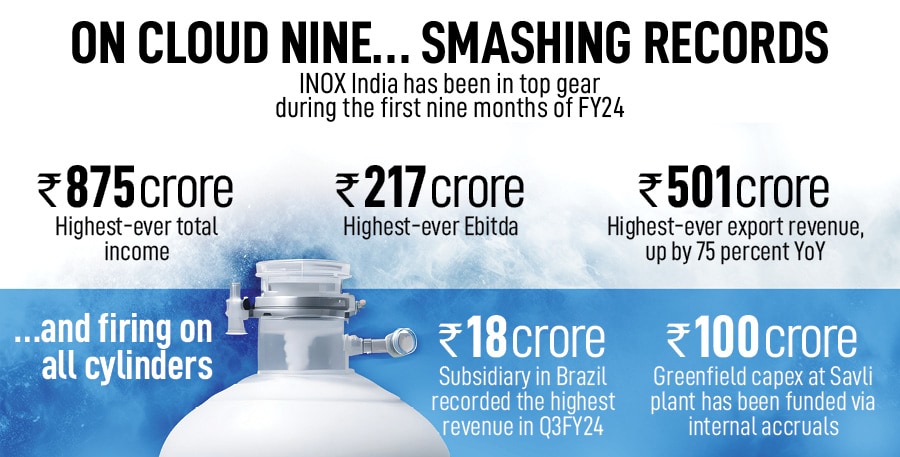

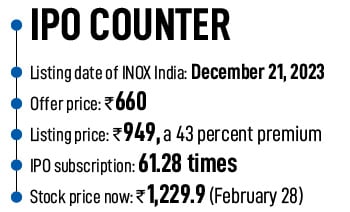

Fast forward to February 2024. Jain is in the midst of a dream run. Inox India had a blockbuster listing towards the fag end of the last year and has continued with its impressive performance by notching record numbers in the first nine months of this fiscal (see box). Inox Air Products has maintained its leading position as the biggest industrial and medical gas manufacturer in India. On the cinema front, Inox and PVR merged operations, and the combined entity is now the biggest in India and the fifth-largest listed cinema chain globally.

Jain, for his part, reckons that the dream run over the last three years has just whetted his appetite. “I have this deep desire to make a mark in whichever industry I"m a part of," he says, adding that his overwhelming instinct to become a leader in various categories will always remain pronounced. So, was that the trigger for the merger between Inox and PVR? The founder squarely blames the pandemic and takes us back to the untold merger story.

It all started with the shutdown. Cinemas were closed, OTT was booming, and theatres wore a deserted look. “I never thought in my wildest dream that a movie would ever be released on OTT," says Jain. But this is what was happening. The ‘first-day first show’ paved the way for streaming now on OTT, which became the new Friday, Monday, and all weekdays and weekends. Consumers got addicted to OTT, and there was a strong possibility of the addiction staying there for years.

The Inox honcho was faced with twin challenges. The first was the big issue of ‘how to de-couch the viewers’. They were hooked on to mobiles, and they had to be lured back to the big screen. It was not an easy task. The theatre didn’t have a cost advantage. Moreover, the pandemic transformed cinema lovers into Swiggy and Zomato users. Convenience became the key. The only way to go back to normal was to offer a better cinematic experience in the theatre, make it more accessible to the masses, and a compelling reason for viewers to go back to the big screen. It all needed heavy investments, which no cinema player had. So, it all boiled down to a merger.

But why a merger? Why not an acquisition? Jain laughs. “Which player had the money to buy the rival?" he smiles, underlining a string of similarities between the two potential merger candidates. “We were very like-minded," says Jain, talking about Ajay Bijli and himself. Both entrepreneurs are extremely passionate about the business of cinema and the consumers. “And we understood that unless we come together, we won’t have business going forward," he says. Yes, the merger made sense because survival was at stake. But were there apprehensions as well? After all, it’s one of the rarest of rare cases where two big players and families were joining hands and creating a common entity. Jain agrees that he did undergo moments of severe anxiety.

What, though, sealed the deal was a deep introspection, and an honest question. “Do we want scale or do we want control?" was the question that Jain asked himself. “That was a defining moment for us," he says, adding that the merger would not have been possible without the matching steps taken by PVR. “I will give full credit to Ajay Bijli and his brother for taking that big step," he says. The merger—from inception to conclusion—just took 14 days. “This might be one of the fastest transactions in the world," he smiles, adding that all three businesses—Inox Air Products, Inox India and PVR-Inox—are making money and are on a firm footing. “My business school professor taught me one thing: Cash flow is more important than your mother," he laughs.

Siddharth Jain, reckon marketing experts, has been remarkable in shaping the growth trajectory of the three businesses. There is nothing disruptive about cryogenics, industrial gases and cinema, says Ashita Aggarwal, professor of marketing at SP Jain Institute of Management and Research. But all three are tough businesses to be in. “You don’t stand a chance if you are not a leading player," she says. The third-generation entrepreneur has taken the story ahead and built on whatever he inherited from his father. “Some rest on laurels, some enjoy the legacy, but Jain has grown grit and resilience to carve out his own space," she says. The challenge now for the founder, though, would be do a balancing act as he goes on expanding and diversifying into new verticals and streams.

Jain, for his part, believes that what keeps him on his toes are new challenges. Over two decades into the business, Jain still swears by the golden mantra of building a sustainable business. “Our DNA is Ebitda and cash flow," he smiles. “I have always chased profitable growth," he signs off.

Fast forward to February 2024. Jain is in the midst of a dream run. Inox India had a blockbuster listing towards the fag end of the last year and has continued with its impressive performance by notching record numbers in the first nine months of this fiscal (see box). Inox Air Products has maintained its leading position as the biggest industrial and medical gas manufacturer in India. On the cinema front, Inox and PVR merged operations, and the combined entity is now the biggest in India and the fifth-largest listed cinema chain globally.

Fast forward to February 2024. Jain is in the midst of a dream run. Inox India had a blockbuster listing towards the fag end of the last year and has continued with its impressive performance by notching record numbers in the first nine months of this fiscal (see box). Inox Air Products has maintained its leading position as the biggest industrial and medical gas manufacturer in India. On the cinema front, Inox and PVR merged operations, and the combined entity is now the biggest in India and the fifth-largest listed cinema chain globally.