Hemant Taneja, CEO, General Catalyst

Image: Cody Pickens for Forbes

Advertisement

India’s digital payment ecosystem has transformed how people transact - fast, simple, and cashless. The UPI (Unified Payments Interface) has played a significant role in this shift, facilitating billions of UPI payments each month through various mobile applications. UPI has made money movement seamless and accessible to anyone with a bank account and smartphone.

UPI has undergone several upgrades over the past few years, including features such as UPI Lite, UPI Tap & Pay, and UPI Circle, which simplify group payments. Another addition is the UPI Credit Line - a feature that brings short-term credit directly into the ecosystem.

With ongoing changes in digital payments, new features are transforming the way people pay, borrow, and manage their finances in everyday life. In this post, we’ll discuss the basics, key features, how to set up a credit line in UPI, and what it could mean for everyday users exploring newer ways to pay.

What is a UPI Credit Line?

A UPI Credit Line is a pre-approved loan facility that lets you (user) borrow money through UPI and use it for regular digital payments. It works much like a flexible loan, where you’re given a sanctioned credit limit by your bank, and can use as much or as little as you need. Interest is charged only on the amount used, not the entire limit.

What makes the credit line in UPI useful is how seamlessly it fits into everyday payments. Just like savings accounts or debit cards are linked to UPI, you can now set up a credit line as your payment source. It’s available in both secured and unsecured variants, with some banks offering it against fixed deposits.

Key features of UPI Credit Line

The UPI Credit Line combines the convenience of UPI payments with the flexibility of short-term borrowing. Here are some of the key features that make it useful for everyday digital payments:

Pre-approved: Banks assign a credit limit and allow you to borrow money as needed. Interest is charged only on the amount used, not the entire credit line.

Easy setup: You can set up a credit line using the registered mobile number and link it to any UPI-supported app, just like you do with savings accounts or wallets.

Real-time tracking: The UPI app displays details such as available credit, usage, EMIs, and repayment options. You (a borrower) can repay the loan in full or through instalments, with auto-pay options also available.

Merchant-only payments: UPI payments through the credit line are limited to verified merchants, either via QR codes or e-commerce platforms. Peer-to-peer transfers are not supported.

Secure transactions and support: Payments are authenticated through a dedicated UPI PIN for credit line use, and any disputes can be resolved directly through the app using UPI Help.

What are the advantages of using a Credit Line on UPI?

The UPI Credit Line brings several benefits:

Instant access to credit: Once you set up a credit line with your bank, it’s available instantly for UPI payments without extra paperwork or cards.

Flexible repayment option: The borrowed amount can be repaid in one go or via instalments, depending on what works best for your finances.

Simple and secure transactions: No need to swipe cards or carry physical documents - just use your UPI PIN to pay.

Lower-cost borrowing: The interest rates and fees can be more affordable than regular credit cards.

How’s it different from regular credit cards?

A UPI Credit Line gives you access to funds just like a credit card, but without the need for a physical card. It’s linked directly to your UPI ID, which means you can use it for UPI payments across supported merchants without carrying anything extra.

Unlike credit cards, there are usually fewer setup costs, and the process to set up a credit line is simpler. It also differs from Buy Now, Pay Later options that are often limited to specific platforms.

Who can apply for a Credit Line on UPI?

To apply for this loan via UPI, you must be at least 18 years old, hold an active savings account with the issuing bank, and have UPI activated on your registered mobile number. You should also have a clean history without any criminal record. Some banks may display pre-approved offers within their app or on your UPI app screen.

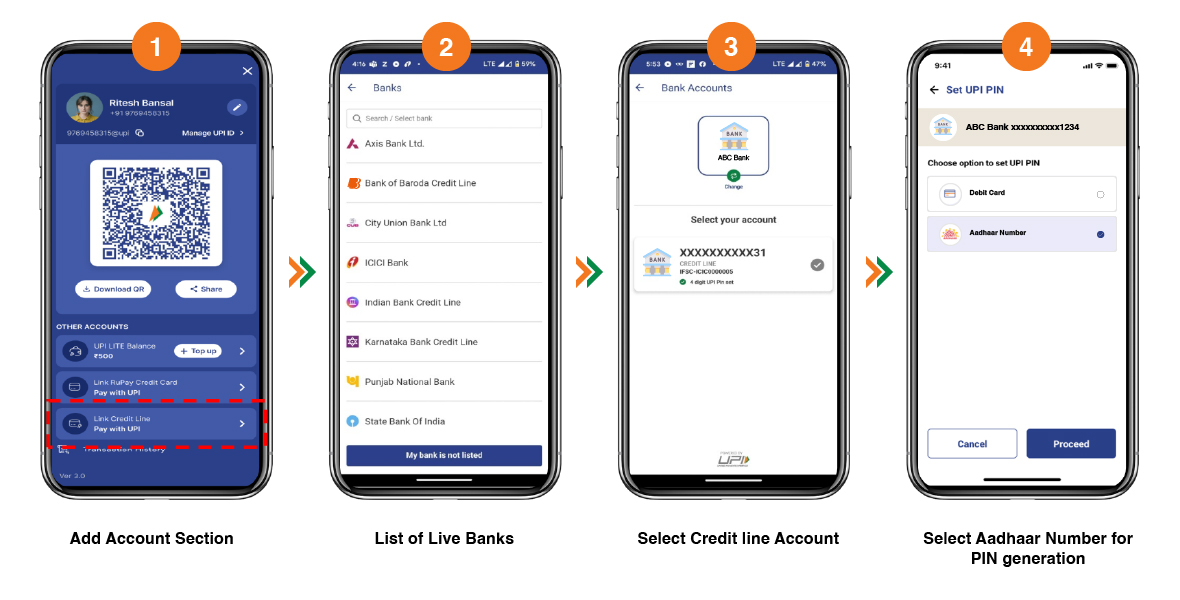

To set up a credit line, you may need to accept digital consent terms and agree to the repayment structure. Once approved, the credit line gets linked with your UPI account and can be used for digital payments.

Open any UPI-enabled app, such as Google Pay, PhonePe, or Paytm.

Head to the ‘Credit’ or ‘Loan’ section and tap on the ‘Credit Line’ option.

Fill in your personal and financial details and complete KYC if asked.

Choose your bank that offers a credit line in UPI.

Enter the required verification codes and complete the setup.

Set a UPI PIN, and your credit line will be ready for UPI payments.

Frequently asked questions (FAQs)

Can the Credit Line on UPI be removed after using the service?

Yes, you can remove the UPI Credit Line from your selected digital payment app after completing your transactions or once you no longer wish to use the service.

Which digital payment apps currently support the UPI Credit Line?

Several apps, including PhonePe, Google Pay, Paytm, BHIM, PayZapp, CRED, Lazypay, Navi, MobiKwik, and Tata Neu, support credit lines in UPI.

Which banks have gone live with Credit Line on UPI?

You can set up a credit line with banks like HDFC Bank, ICICI Bank, SBI, Axis Bank, PNB, Indian Bank, Kotak Bank, Karnataka Bank, and Federal Bank.