IPO listings disappoint on debut

Market flotations are at an all-time high but the party seems to be fizzling out

Last Updated: Aug 24, 2021, 12:56 IST3 min

For a certain set of investors, it’s all about the listing-day pop. Bid aggressively, corner a chunk of shares, and sell on the day it becomes accessible to the wider public via the stock market. Repeat this over a myriad bunch of businesses across sectors, and the chances of a 20 to 50 percent gain (on listing day) are in your favour.

That pretty much sums up the initial public offer (IPO) market over the last six months. As the chances of a quick buck have grown, an increasing number of speculators have rushed in. The market is divided among retailers (anyone who bids for shares worth up to Rs 2 lakh), high net-worth individuals (HNIs, anyone who bids for shares of more than Rs 2 lakh) and institutions.

“We have seen that whenever the secondary market does well for a while, the primary market also picks up," says Sunil Damania, chief investment officer of Marketsmojo.com.

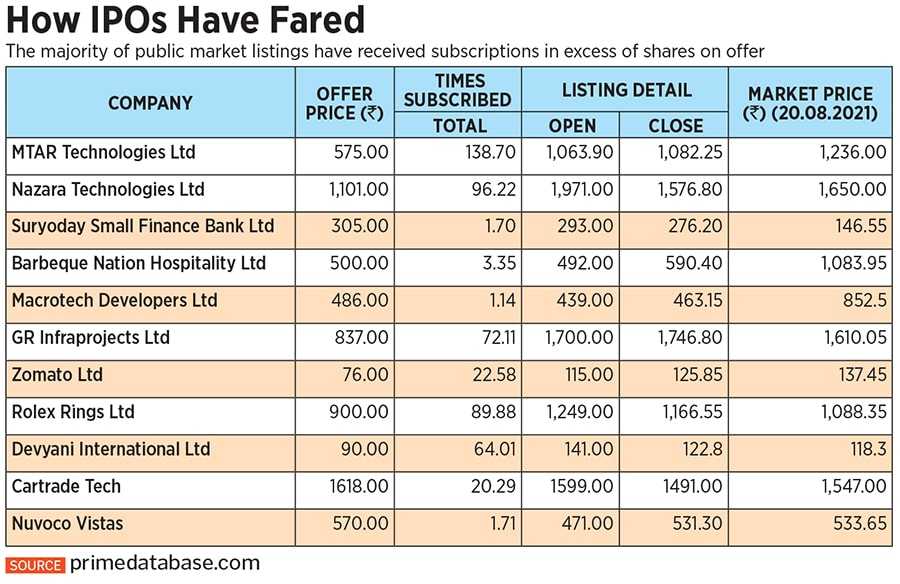

However, there are now some signs that the party is fizzling out. The last four issues listed haven’t had a listing-day pop. Take the recent listing of Cartrade Tech. It listed at Rs 1,599, a 1 percent discount to its offer price. Nuvovo Vistas is also trading at a discount to its offer price, while Aptus and Chemplast Samnar, which opened for trading today, are within their offer price band.

The IPO market frenzy is partly a result of easy liquidity and the fact that financing for IPOs at a rate of 7 to 9 percent is the lowest in a decade. As a result, it’s not surprising to see sought-after issues receiving bids far in excess of the number of shares on offer (see "How IPOs have fared").

Once the allotments are out, HNI investors typically receive no more than 1 to 2 percent of the shares they bid for. So, a Rs 100-crore bid would work out to an allotment of Rs 1-2 crore. Money borrowed at 7 to 9 percent would attract an interest of 0.4 percent for those 10 days or a payout of Rs 40 lakh for the Rs 100 crore borrowed. This is why allotment numbers and listing-day gains are eagerly watched. An allotment of 1 percent or Rs 1 crore for a Rs 100-crore bid would mean no gains for the first 40-percent pop. A 2 percent allotment would need only a 20-percent pop for gains to be made. On the other hand, a 100-percent pop can easily allow an HNI to make 18 percent annualised gains in a 10-day span for which the money has been borrowed.

Issues that are heavily oversubscribed are usually the ones that see a large listing-day pop. Nazara Technologies, which listed on March 30, was oversubscribed 96 times. HNIs bid for 387 times the number of shares on offer. Its shares listed at Rs 1,971, a 79 percent premium from the offer price of Rs 1,101. MTAR Technologies—oversubscribed 136 times—listed at 84 percent premium.

There have, however, been some laggards. Suryoday Small Finance Bank, Barbeque Nation and Macrotech Developers saw oversubscription of 1.7 times, 3.35 times and 1.14 times respectively. They all opened for trading on listing day at below their offer price. Leveraged investors would have lost money here.

As time goes on and market valuations rise, investors need to take into account the falling odds of the listing-day gains strategy succeeding. Damania points out that a key risk to the market, both primary and secondary, is inflation. Like in the past when money supply is tight and central banks start the rate hike cycle, some issues may struggle to get even one-time subscription. It’s still early days, but the absence of a listing-day pop may drive a lot of speculators out of the IPO market.

First Published: Aug 24, 2021, 12:56

Subscribe Now