What went wrong at PharmEasy and can it find a cure?

The online drugs and medical services startup is reportedly raising Rs 2,400 crore in fresh funds at a 90 percent markdown to it previous valuation

Last Updated: Jul 11, 2023, 15:00 IST7 min

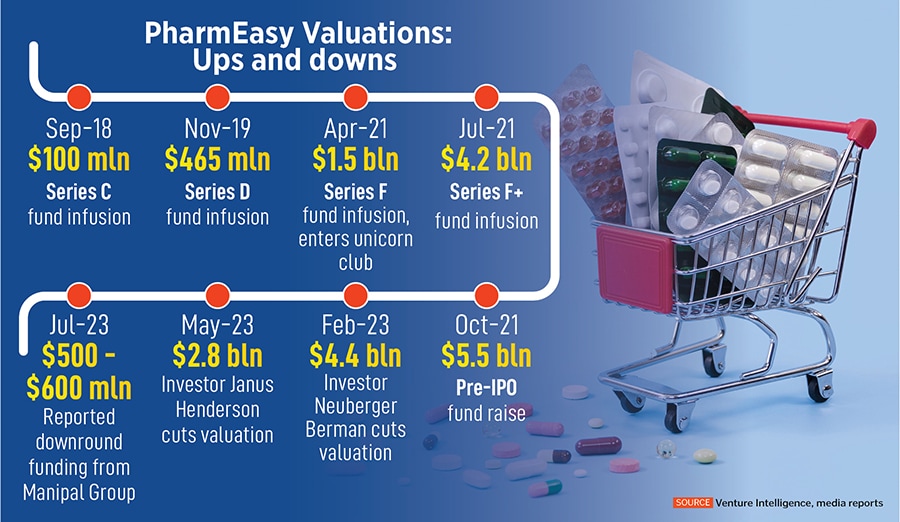

If PharmEasy’s reported Rs 2,400 crore rights issue plays out over the next few weeks, it would have taken less than two years for the online pharmacy’s valuation to plummet from its peak of $5.5 billion in October 2021 to around $600 million. That’s a 90 percent markdown.

Mumbai-based PharmEasy was once the largest online drugs and medical services platform in India. Backed by top investors like Temasek, TPG Growth, Prosus (formerly Naspers), Facebook co-founder Eduardo Saverin’s B Capital and Nandan Nilekani’s Fundamentum Partnership, among others, it raised a total investment of $1.2 billion across 16 funding rounds since its launch in 2014. It even bought Thyrocare Technologies, a profitable testing and diagnostics chain, in June 2021. Although PharmEasy paid a premium for it, the deal made sense at the time. It would help the online pharmacy move from peddling low-margin drugs to selling high-margin testing services.

Besides, the health care market in India is growing. The pharmaceutical sector is expected to grow at a CAGR of 37 percent between 2020 and 2025 to reach $50 billion, as per CARE Ratings.

So how did PharmEasy get here, from its vantage point? And can it recover?

“The business was doomed from Day 1," says a former employee speaking to Forbes India on the condition of anonymity. That’s because of the nature of the business.

Consider this: India’s pharma market is dominated by branded generics. There are around 200,000 brands in the country, constituting 75 percent of the $1 trillion pharma market, according to IMS. Patented drugs constitute just 7 percent of the market, while the remaining 18 percent comprises generics. India’s retail and distribution space is fragmented with over 600,000 retailers and 60,000 wholesale distributors. Plus, the government regulates the prices of medicines in India. Not only does the maximum retail price (MRP) of medicines have to be approved by the National Pharmaceutical Pricing Authority (NPPA), the government body in charge, but margins for each of the pharma supply chain players are largely fixed. Retail pharmacies have 20 percent margins, distributors have 10 percent, and cost and freight (C&F) have 4 percent margins.

PharmEasy tried to be the bridge between the fragmented offline sellers on one side and online buyers on the other. They tied up directly with over 3,000 manufacturers and over 90,000 retailers across India to deliver medicines to customers in the shortest time possible.

It succeeded to a large extent. With over 12 million registered users and 17 million monthly active users, API Holdings, PharmEasy’s parent, grew to become the largest online pharmacy, clocking revenues of Rs 2,361 crore for the year ending March 2021. Rivals 1mg, now owned by the Tata group, and Reliance-owned Netmeds, posted Rs 134 crore and Rs 151 crore in revenue, respectively, in the same period.

Even so, given the regulated prices and low margins of the pharma industry in general, coupled with the 20-odd percent discounts and cashbacks PharmEasy offered along with free delivery, its unit economics “were horrible", says the former employee.

“Everyone knew this and hoped scale would fix everything," says Kaushal Shah, co-founder and CEO of eVitalRx, an Ahmedabad-based pharmacy billing and inventory management software startup. “Unfortunately, the scale argument for negative unit economics doesn’t work in medicines. People don’t just consume more medicines. Besides, people in India prefer brands prescribed by their doctors," he says. Thousands of competing generic brands, medicine expiries, and logistics also negatively impact unit economics, he notes.

PharmEasy decided to strengthen its position through vertical integration, which would help it extract higher margins. Soon after a $350-million fund raise in April 2021, which shot the e-pharmacy to unicorn status valuing it at $1.5 billion, Pharmeasy went on a shopping spree.

It acquired around 15 regional distributors. It also mopped up two enterprise resource planning software companies, Marg and Redbook, to ensure frictionless logistics between its pool of distributors and end customers. It then bought Aknamed, a supply chain platform that enables hospitals to procure medicines online. But the biggest acquisition in that year was that of Thyrocare.

PharmEasy bought 66.1 percent of the profitable testing diagnostics chain from A Velumani, its promoter, for Rs 4,546 crore ($612 million) in June 2021. In turn Velumani invested Rs 1,500 crore ($202 million) to acquire a 5 percent stake in PharmEasy. It paid a premium for it, funding this and other acquisitions through a series of loans. Lenders included Kotak Mahindra Bank, Aditya Birla Finance, and Hero Fincorp interest rates ranged between 9 and 17 percent.

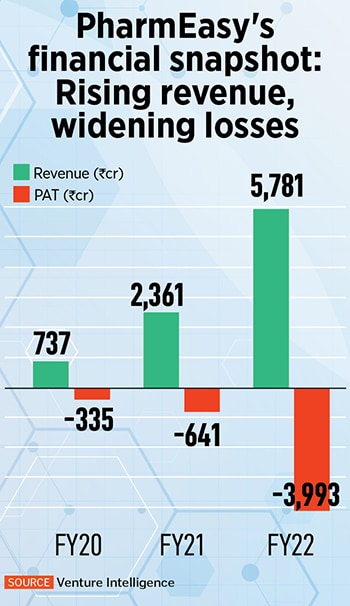

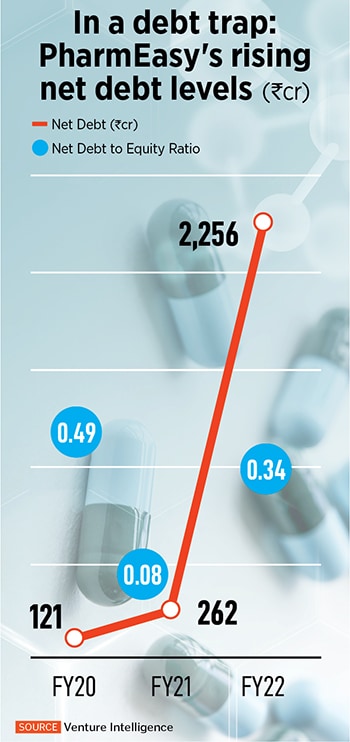

As a result, the net debt of API Holdings, PharmEasy’s parent, grew from Rs 262 crore in the year ended March 2021 to Rs 2,256 crore in the year ended March 2022, according to Venture Intelligence, a data provider. Its net debt-equity ratio worsened from 0.08 to 0.34 during the same period. Revenues grew 2.5x to Rs 5,781 crore in the same period, but losses widened more than 6x to Rs 3,993 crore.

As a result, the net debt of API Holdings, PharmEasy’s parent, grew from Rs 262 crore in the year ended March 2021 to Rs 2,256 crore in the year ended March 2022, according to Venture Intelligence, a data provider. Its net debt-equity ratio worsened from 0.08 to 0.34 during the same period. Revenues grew 2.5x to Rs 5,781 crore in the same period, but losses widened more than 6x to Rs 3,993 crore.

PharmEasy planned to repay the debt it took on by going for an initial public offering (IPO). In November 2021, API Holdings, filed its draft red herring prospectus with market regulator Securities and Exchange Board of India (Sebi), stating its intent to raise Rs 6,250 core (approximately $1 billion) at a $9 billion valuation. The IPO was supposed to hit the market in early 2022.

But the markets went rogue. The global meltdown of tech stocks and the lacklustre listing of Paytm and Zomato on the Indian exchanges made PharmEasy roll back its IPO plans, citing “market conditions and strategic considerations".

But it loan obligations still had to be met. So PharmEasy borrowed $285 million from Goldman Sachs in August 2022 to pay off its debt. The loan included a covenant to the effect that PharmEasy would have to raise equity of around Rs 1,000 crore (about $120 million), linked to its burn rate velocity, within a year of taking the loan, according to the senior employee quoted earlier.

While PharmEasy has not defaulted on any of its payment obligations thus far, it will soon be in breach of its covenant terms with Goldman Sachs. The terms of the covenant agreement allow Goldman Sachs to potentially take over the entire company or its most profitable arm Thyrocare as all the assets of API Holdings were used as security to obtain the loan, says the employee.

Also watch: From Byju-Aakash to PharmEasy-Thyrocare: Top 10 startup acquisitions of 2021 in India

“Basically, they [promoters Siddharth Shah, Dharmil Sheth and Dhaval Shah] bit off more than they could chew," says the senior employee. Hence the fresh rights issue at a 90 percent markdown. “Any money is better than no money at this point," says the investor quoted earlier.

The rights issue will be led by Ranjan Pai’s Manipal Group, which will reportedly be investing Rs 1,000 crore for an 18 percent stake in API Holdings. Existing investors Temasek and TPG Growth are also expected to contribute about Rs 1,500 crore to the funding round. Interestingly the latter two are also investors in Manipal Group.

“The investors are calling the shots at this point. The co-founders don’t have any say," says the senior employee. Pai declined a request for comment on the matter. PharmEasy did not respond immediately to Forbes India’s request for comment.

“The investors are calling the shots at this point. The co-founders don’t have any say," says the senior employee. Pai declined a request for comment on the matter. PharmEasy did not respond immediately to Forbes India’s request for comment.

Worryingly, the co-founders don’t have any skin in the game. Siddharth Shah held a 2.53 percent stake in API Holdings as of March 2021, Sheth had 0.12 percent stake, while Dhaval Shah held a mere 0.04 percent stake. Yet, says the senior employee, “they are the best people to run the company, as they know it from ground up," adding, “had the markets not soured, PharmEasy wouldn’t be in this situation."

In many ways PharmEasy’s troubles mimic those of Byju’s. The edtech giant also took on large pools of debt to fund acquisitions in India and abroad during the pandemic years. It’s now struggling to repay that debt as its plans to list offline tutoring business Aakash were shelved due to the unfavourable market conditions.

“A lot of these business models are coming under challenge," says the investor. “I still think PharmEasy is a great business. It will probably get bundled into a larger horizontal over time because I don’t think you need a specialised vertical only for medicine delivery as pharmacies are available across the road. So either they become a horizontal by bundling personal care delivery and say, FMCG products, or they get consumed by a horizontal."

The rights issue is expected to close in the next six to eight weeks.

First Published: Jul 11, 2023, 15:00

Subscribe Now