A curious case of short-term risks and long-term potential of the Indian economy

From finding a remedy for stagflation to focusing on supply-side reforms, what are the prospects for the Indian economy in the short and long run? Professor at IIM Kozhikode breaks down several factor

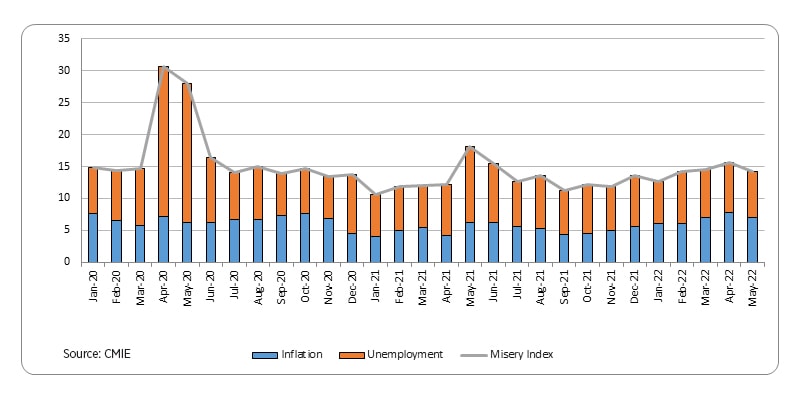

The latest misery index value for India (14.1 percent) is not pretty but is nevertheless the lowest since January 2022 <br>Image: Shutterstock

Advertisement

The Indian economy was all set to turn the corner at the beginning of 2022. Despite the Omicron wave, unemployment at 6.6 percent in January was the lowest in 10 months. Inflation at 6 percent was just at the upper end of the RBI’s target band. But the global economy received an unexpected jolt with Russia invading Ukraine in February. As global oil prices surged, inflation in India shot up to an 8-year high of 7.8 percent in April. With the unemployment rate also clocking 7.8 percent in April, stagflation whispers grew louder. How serious is the risk of stagflation? What are the prospects for the Indian economy in the short and long-run? Let us start with the ‘misery index’.

Stagflation is a combination of high inflation and low economic growth. Since growth data is not available on a high-frequency basis, the unemployment rate can be used to proxy (the lack of) economic activity. Adding the two figures, we arrive at the ominously named misery index. The latest misery index value for India (14.1 percent) is not pretty but is nevertheless the lowest since January 2022. The misery index sharply deteriorated during the two major lockdowns mainly due to high unemployment but has now returned to the pre-Covid levels. The unemployment rate of 7.1 percent in May is the lowest since January 2022. This is in line with the robust performance of several other high-frequency indicators of economic activity such as tractor, two-wheeler and four-wheeler sales, electricity consumption and industrial production.

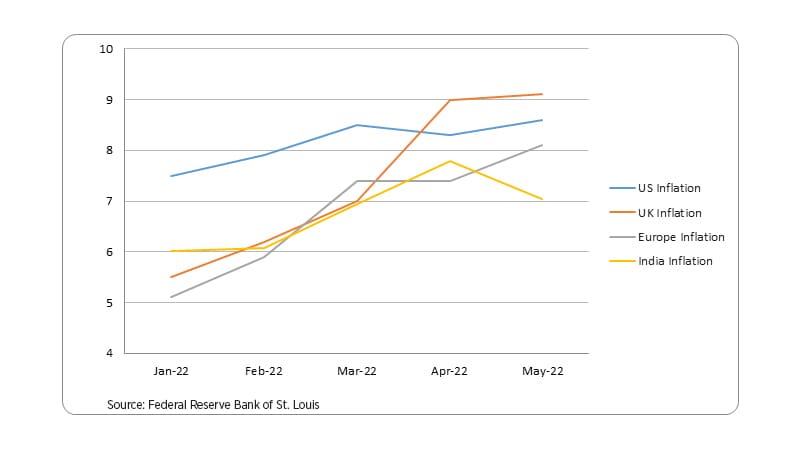

Inflation came down in May thanks to the government’s duty cuts on oil. But prices will depend on exogenous factors such as crude, global supply chains and monsoon. With the RBI sharply raising its key lending rate (the repo rate) in two quick bursts, prices may cool down over the next few quarters. India’s inflation rate is already lower than it is in the West. Advanced economies are grappling with the inflationary consequences of massive fiscal stimuli during the pandemic. India’s recovery package was smaller in comparison and has not hurt prices as much. Discounted crude purchases from Russia are helping to keep down import costs. With deft policy interventions and a bit of luck, inflation does not seem as big a worry as it is elsewhere. With economic activity chugging along, it does not appear that the misery index will worsen much, barring new shocks. The fears of stagflation seem overdone.

Long term potential

While the short-run jitters can be managed, a bigger concern is the damage that Covid-19 inflicted on India’s long-run potential. Consider the three essential ingredients of long-run economic growth—physical capital, human capital and technology. Physical capital (comprising machines, tools, equipment and so on) is created by business investments. Gross fixed capital formation went up by 15.8 percent in FY22, but the increase is merely 3.8 percent compared to before Covid-19. Notably, the financial savings of households as a share of their disposable income have gone up along with corporate sector profits. If this trend continues, then with a larger GDP base in the coming years, the economy will be able to generate a higher quantum of savings for channelling into capex spending. Expansion of the production-linked incentives scheme and continuing interest from foreign investors will aid the recovery of private investments.

The loss of human capital formation in the last two years will be harder to recover from. The recently released National Assessment Survey shows that average scores of school children have fallen in all subjects in 2021 compared to 2017. This indicates severe learning loss that may compromise productivity and earning potential in the coming years. Schools must adopt strategies to recoup the learning losses before attempting to complete the new academic year’s syllabus. One can imagine that similar losses would have occurred in the skilling sector hampering the growth of a skilled workforce. The education sector must leverage technology to complement in-person teaching and training. Another aspect of human capital is health where India lags the global averages in parameters such as life expectancy, mortality and physicians per capita. An updated national health policy will help to enhance the health of the workforce.

Technological progress is determined by investments in R&D and startups. India’s R&D expenditure peaked in 2008 at 0.86 percent of GDP and since then has steadily fallen. The ratio is substantially lower than in the middle income to rich countries, where average figures are in the range of 1.5-3 percent of GDP. Patent applications per capita are way below that in other countries. The silver lining is the startup ecosystem which is now the 3rd largest in the world after the US and China. India has witnessed a jump in the World Competitiveness Index ranking from 43rd to 37th out of 63 countries in 2022. There has been good progress in digitisation and the adoption of new technologies like AI, robotics, and IoT. If the government increases its allocation towards R&D, simplifies the patent approval process and provides fiscal incentives to the corporate sector for innovation, it can quicken the pace of technological progress.

Physical capital, human capital and technology are the necessary conditions for long-run growth. But they are not sufficient. The secret sauce that explains why rich countries are rich is the quality of their institutions such as laws, property rights and dispute resolution mechanisms. The Indian government launched several structural reforms such as the GST, IBC and RERA in the past few years. Indirect tax collections have reached record-high levels, although partly helped by inflation. Indian banks have cleaned up their books with gross NPA ratio falling below 6 percent, the lowest in 8 years. New labour laws are set to kick in from July 1 bringing flexibility in work arrangements that will help formalisation of the workforce.

Going ahead, the government has to be relentless in supply-side reforms. The many strengths of the economy include demographic advantage, natural resources, a diversified economy, political stability and cheap labour. But leveraging them requires improvements in the business environment through refinements in regulations around trade and investments, land acquisition, energy pricing, business-related approvals, and financial markets.

Rudra Sensarma is a Professor of Economics at the Indian Institute of Management Kozhikode. Views are personal.