“It was, in a way, a sort of homage to where we had landed, this is where we had these events, it didn’t scare us off from investing in the country. And on the back of that, of course, we grew to be what we are today, $20 billion invested in India," says Ranjan, managing partner at the firm, who launched and headed Brookfield’s India operations. Last October, he was elevated as the global head of business development, head of Europe and Asia-Pacific private equity, and CEO of South Asia and the Middle East for BAM.

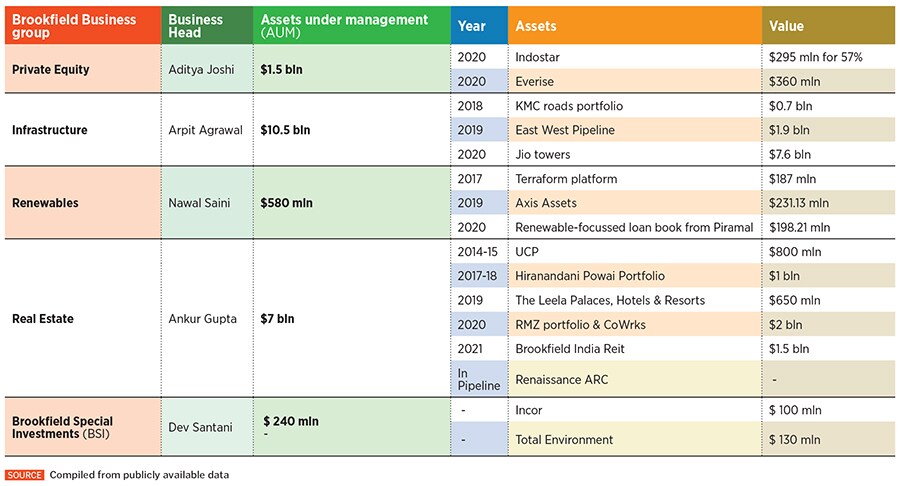

While Ranjan now spends his time between the Dubai and London offices, he can’t stop gushing about the fact that of the nearly $20 billion the firm has invested in India since it set up an office in the country officially in 2009 with three employees (including him), it has deployed over half of it (nearly $11.5 billion) amid the raging pandemic in 2020. Brookfield is an NYSE- and Toronto-listed firm and has deployed approximately"¯$600 billion"¯in AUM across real estate, infrastructure, renewable power, private equity, and credit."¯

“You know, we did not make a single major investment in India till 2014. Of course, we started working on things but our first big idea came in 2012 and by 2014 we closed that deal which was our first investment in the real estate space," Ranjan reminisces of one of the most complex deals in Indian real estate over a long Zoom call from his London office.

On June 12, 2014, Brookfield announced that it would acquire Unitech Corporate Parks Plc (UCP), a London Stock Exchange-listed India-focussed real estate investment firm, for around (£205.9 million) or ₹2,034 crore. What is interesting is how they zeroed in on this asset.

Brookfield runs a global programme called the Best Ideas Program. Every month, nearly 1,200 investment professionals globally log in to this call and critique the best idea. And if the idea is approved, that person is given a budget to buy some stock in that company as part of training. It is meant to be an exercise to get the best out of the youngsters in the company to demonstrate if their ideas are actually workable and it also gives them access to the senior management. And sometimes, some of these ideas turn into real transactions. UCP was one of those ‘best ideas’.

![]() (Left to right) Nawal Saini, Dev Santani, Ankur Gupta, Aditya Joshi and Arpit Agarwal of Brookfield at their office in Powai, Mumbai

(Left to right) Nawal Saini, Dev Santani, Ankur Gupta, Aditya Joshi and Arpit Agarwal of Brookfield at their office in Powai, Mumbai

Image: Neha MIthbawkar for Forbes India

Between 2006 and 2011, investments in Indian real estate were essentially in large greenfield developments, especially residential. The global financial crisis took a little sheen away from a lot of foreign funds (impacted back home, many folded in India) but domestic capital kept pouring in into residential projects.

“Watching the kinds of transactions that were happening, they were largely minority deals in greenfield developments. And that did not make sense to us. It wasn’t the kind of thing we wanted to do. We also didn’t want to come in and do completely greenfield development until we had built out a real operating capability, which came much later," Ranjan explains.

We didn’t make a single major investment in India till 2014. Our first big idea came in 2012 and by 2014 we closed the deal, our first investment in real estate."

Anuj Ranjan, Head of Europe and Asia-Pacific Private Equity, and CEO of South Asia and Middle East, Brookfield

What Ranjan wanted was a pie of the burgeoning office space in India—he believed there was significant opportunity for the rent yield to grow over the years. But the problem was they didn’t want to do a minority transaction. They started looking at platforms, larger companies, ready properties but there weren’t many in India back then that were large in size and scale. Meanwhile, in 2011, its global peer Blackstone Group swooped in and closed its first and the country’s largest commercial asset deal after flagging off its real estate arm in 2007. For an undisclosed amount, it went on to acquire a substantial stake in the Bengaluru-headquartered Manyata Business Park from Embassy Property Developments it continues to hold on to the asset.

The time for commercial had arrived. In the middle of all this was Delhi-based realtor Unitech, in its heydays of 2008 the second-largest realty company in India by market capitalisation, that had even managed to bag Lehman Brothers’ last India cheque of ₹740 crore. But times had turned rough and its Alternative Investment Market (AIM)-listed firm, where its commercial office properties were housed, was becoming an easy target for a sale process to pay off its lenders. UCP, at that point, was developing a mix of six special economic zones and IT parks across Noida, Greater Noida, Kolkata and other regions.

![]()

Ranjan recalls, “We did our best idea on UCP and showed it to the group globally. The group challenged it, we debated it. And in the end we said, ‘You know this stock does seem like great value. So why don’t we buy some stock’." And from buying some stock, they saw an opportunity. “After we became a small shareholder, we felt this could be something more meaningful. Let’s see if we can become a larger shareholder. And then, let’s see if there’s an opportunity to privatise the whole business."

But the problem was the complicated structure of UCP. The holding company for UCP was Candor Investments Ltd, which was incorporated in Isle of Man. UCP had formed a 60:40 joint venture with Unitech. Forty percent of the asset was held by Unitech and it had financing against it as well. So Brookfield had to work with the banks in India and Unitech to put the whole deal in place.

In 2012, Ankur Gupta was part of this summer project sitting in the Brookfield New York office. Over time, he became the head of the real estate vertical for India deals but it was only in 2019 that Gupta returned to India and started working in the Mumbai office located at the Bandra Kurla Complex (BKC). Gupta is the head of real estate and a managing partner at the firm. But at that time, the UCP deal literally had people spread across four continents trying to put the deal together.

![]() “We were able to put together a transaction that spanned four continents. It was a UK-AIM listed entity where while the assets were in India, the structure of the company was held in Mauritius and then there was the holding company. And a lot of the transaction work was being done in the New York office. And that’s the power of the firm that it really comes together when it comes to executing our ideas," says Gupta.

“We were able to put together a transaction that spanned four continents. It was a UK-AIM listed entity where while the assets were in India, the structure of the company was held in Mauritius and then there was the holding company. And a lot of the transaction work was being done in the New York office. And that’s the power of the firm that it really comes together when it comes to executing our ideas," says Gupta.

“The thing I’m most proud of and of that opportunity was the fact that over the two years from the first share we bought until we did 100 percent acquisition, we never lost our conviction. We were actually patient and it took us that long to convince all the stakeholders," adds Ranjan.

Brookfield went on to hire an entire operating team and, over the years, it has built all the under-construction projects of the portfolio, finally this year listing the assets as part of its real estate investment trust (REIT) on the Indian bourses. It had ended up with nearly 8 million sq ft of operating assets where some tenants were unhappy with the uncertainty around the asset, and another 3-4 million sq ft under construction where work had essentially stopped due to contractor and budget restrictions. To be able to put it all together and put the machine back in motion had been one of the biggest projects and challenges the firm had undertaken.

“When you’re standing on a half-built construction site, where contractors have left and the developer has thrown in the towel, it takes a lot of skill to revive those projects. I’m very grateful to the operating teams, [for the fact] that we have senior leaders who took on the mantle," says Gupta. From 8 million sq ft of projects then, UCP now has 16 million sq ft under its belt.

The firm also has a 400-person team that does nothing but run its office presence in the country. In February, Brookfield listed Brookfield India Real Estate Trust, India’s only institutionally managed public commercial (REIT) and the firm’s second listing globally of its REIT programme.

The ₹3,800 crore public issuance of its real estate portfolio, too, narrates the story of how the investment firm has differed from its global peers in how they operate their business in India. India currently has three listed REITs, two of which are led by Indian developers backed by Blackstone. But this is India’s first institutional REIT run by the firm. Which means BAM owns and operates these properties and is not dependent on any developers for the projects.

We were able to put togEther a transaction that spanned four continents. That’s the power of the firm.

Ankur Gupta, head of real estate and managing partner, Brookfield

On February 16, 2021, Brookfield offered its shares for ₹275 per share. The issue was oversubscribed 7.94 times. On June 7, the shares closed at ₹258.19 apiece. Since the second wave of the pandemic, the gains at India’s listed REITs have tapered as questions around demand for commercial space have once again picked momentum. However, while declaring its March quarter results for this year, BAM said it has managed to recover 99 percent rents from its tenants. Collectively too, Indian REITs saw strong rental collections of over 99 percent in 2021, which means tenants have continued to pay for their leases.

“India went from a very high interest rate market to a lower interest rate market. We’ve been able to see an entire journey and our investors are happy with the outcome," adds Ranjan.

Even as work from home (WFH) and hybrid models of work are being touted as the way forward, it is perhaps the best time for Brookfield to build a stronger commercial portfolio for the long term—in a world beyond Covid-19 and when offices start buzzing again.

According to Adhidev Chattopadhyay, vice president at ICICI Securities, who has a buy on the stock, even though overall portfolio occupancy levels have declined by 4-6 percent for the three Indian REITs (collectively), owing to WFH and the second wave affecting the leasing decisions, and the sector faces near-term weakness, BREIT has delivered a resilient FY21 performance with over 99 percent of rental collections. He expects an estimated distribution yield of over 8 percent in both FY22 and FY23 as per current prices. While leasing deferrals may increase leading into this financial year, Chattopadhyay expects demand to be back by second half of this financial year.

*****

Unlike other global private equity peers who either buy out ready assets or undertake joint ventures with developers, in Brookfield’s first India deal, it actually got its hands dirty building some of its assets ground up. Later, as developers looked for capital to consolidate their operations, the investment firm managed to acquire some key assets like a few of builder Hiranandani’s assets in Powai. As Gupta narrates, “If there was one project that caught our imagination, it was Hiranandani Gardens in Powai." BAM paid nearly $1 billion in 2016.

What had them excited was that Hiranandani had 25,000 condominiums, street retail walking tracks, jogging tracks, amenities, and an office business portfolio of 16 buildings that housed some of the biggest tenant profiles in the world like Credit Suisse, Nomura, Fidelity, Apollo Global. “What appealed most to us in this portfolio was the location it has in Mumbai, the ecosystem of live and play and our ability to add value in that ecosystem," says Gupta.

![]() “They came late to India like other Canadian funds but they had a special mandate of deploying capital in the entire gamut of real estate and infrastructure and they have demonstrated their commitment in India. Their commitment to India is enormous and they have deployed huge dollars," says Deepak Parekh, chairman at HDFC Ltd, also pointing out that their board visited India just before the pandemic.

“They came late to India like other Canadian funds but they had a special mandate of deploying capital in the entire gamut of real estate and infrastructure and they have demonstrated their commitment in India. Their commitment to India is enormous and they have deployed huge dollars," says Deepak Parekh, chairman at HDFC Ltd, also pointing out that their board visited India just before the pandemic.

He adds that Ranjan and Gupta have their ears to the ground and they have differentiated themselves by undertaking development and construction of projects, and now the Canadian investment firm is betting on the rental housing sector. “Overall, they have understood how to invest in India and know all the major players in the country," he says.

The firm’s global real estate business, one of the oldest practices, is slightly in excess of $200 billion and consists of grade-A offices, malls, hotels. It is now busy replicating the same model in India. It has deployed nearly $7 billion in the country as part of its real estate business, of which $6 billion has been committed towards commercial office assets, which include high-quality mixed use projects and office parks spanning more than 45 million square feet. It has also acquired the distressed asset the 2,600 keys-Hotel Leela from JM Financial Asset Reconstruction Company.

Gupta explains, “It’s not just the scale that matters. It’s a way of running our business that sets us up for growth in future. Otherwise, we could have done one deal and made money or not, but the processes that have been set up are here to stay and have created a business that should last for a very long time."

Last year, as the country was going through the first wave of the pandemic and everyone went remote when it came to work, Gupta and his team silently stitched together one of the largest commercial deals ever done in the country. It acquired Bangalore-based RMZ Corp’s 12.8 million sq ft commercial portfolio for $2 billion. From start to end, the team completed the RMZ deal in a little over three months. What helped their case was that they knew the developer well.

As Gupta explains, “…to be able to do diligence on 41 buildings, one of the largest portfolios in India, and to do that in a very short timeline, legal diligence, architectural diligence, physical diligence, etc. I would say that really proves how far along we are in our capability in India."

In India, it has been tough for foreign investors to acquire large assets but Brookfield seems to have the knack. And while the firm has been planning its road ahead, it believes Indian markets are at a stage where the overall market will exponentially grow.

While a major amount of capital has been deployed in commercial real estate, another deal that took a long time to fructify was the acquisition of distressed luxury property Hotel Leelaventures Ltd. The first time BAM got interested in Leela was in 2015 when the company was looking to do its debt restructuring to meet its financial obligations. But the deal didn’t go anywhere. While the firm has closed in on quite a few distressed deals in the last few years, this was one of the initial ones that intrigued them.

“I still remember a meeting I had with Vishal Kampani when he was in New York, this was in the summer of 2018, when the conversation restarted…," remembers Gupta about meeting Kampani, who heads JM’s distressed asset business.

![]() While Gupta and Ranjan had met various people over the course of 2015, 2016 and 2017 including the Nair family which owned the asset, in the summer of 2018, Gupta could visibly see that JM was now representing the banks and they were getting close to a resolution.

While Gupta and Ranjan had met various people over the course of 2015, 2016 and 2017 including the Nair family which owned the asset, in the summer of 2018, Gupta could visibly see that JM was now representing the banks and they were getting close to a resolution.

While several options were suggested that included buying a few properties to putting capital in the company, Gupta’s conviction was that Leela Hotels needed a wholesome solution. JM ARC, State Bank of India and HDFC Ltd were the largest lenders to the company.

Fast forward to 2019. Gupta was in India due to his relocation and the lenders met them, wanting a commitment from Brookfield. In October 2019, Brookfield acquired Hotel Leelaventure Ltd for ₹3,950 crore. Meanwhile, ITC Ltd, a minority shareholder at Leela, had filed a case against the sale and, in September 2019, Securities and Appellate Tribunal (SAT) had dismissed the case.

“Over the last two years, we have infused significant capital to make sure the properties have the capital structure that could sustain the business. We’ve put together a professional management team. We are creating efficiencies in the business to realise a luxury brand company that is at the core of the business," explains Gupta on how they are turning around the asset since the acquisition.

Despite the pandemic, BAM opened a new Leela Palace property in Jaipur recently, the first hotel to be opened under the Leela flag in nine years. It is opening two more hotels in the coming quarters in Gandhinagar and Bengaluru.

In the four years that it was chasing the Leelaventure deal, it also signed a $1 billion (₹7,000 crore) joint venture with state lender SBI to jointly acquire distressed assets in July 2016. The JV failed to take off. It has recently announced the launch of an asset reconstruction firm in partnership with lender HDFC Ltd to acquire stressed real estate asset situations. As part of the structure, 80 percent of the capital will be committed from Brookfield and the remaining will come from the bank. It is awaiting RBI clearance and once in place, it expects to do large deals in this space.

“With the ARC, we can actually mobilise a lot of capital in that strategy. The real estate sector needs that kind of capital," says Gupta as he explains that it is too early to comment on the deal size. Globally, BAM is in the market right now raising its fourth fund in its global series of real estate funds, which is targeted to raise almost $18 billion.

While BAM has been an active investor in real estate in India since its early days, apart from its Reit this year where it used the proceeds to reduce the asset’s indebtedness, it is yet to exit any of its transactions. But Ranjan isn’t worried, he says, “We are a long-term investor and India is still a market we are growing in. We are very pleased with the performance of our investments."

*****

One of the overarching themes for Brookfield has been to acquire and operate assets on a large scale, projects that are operationally intensive.

While it started its journey in India with investments in real estate and small infrastructure bets, Brookfield has deployed nearly $10.5 billion under its infrastructure asset class in the last three years. In August 2015, Gammon Infrastructure Projects had entered into an agreement with BIF India Holdings (Brookfield) to sell six road and three power projects for about ₹563 crore to the investment firm. After that acquisition, Brookfield took a back seat when it came to infra deals but in 2019, it went all out and acquired Reliance Group’s East West Gas Pipeline business for $1.9 billion.

If that wasn’t enough, in August 2020, BAM, through Brookfield Infrastructure Partners LP, acquired 100 percent stake in the telecom tower (Reliance-Jio Towers) business of Reliance Industries. Brookfield and its institutional partners have invested $7.6 billion in the asset.

“Infrastructure for us is like creating a pool of long-term stable cash flow assets, that are generally resilient to economic cycles, and are vital to the functioning of the economy," says Arpit Agrawal, managing director, infrastructure, who joined the firm four years ago.

And, Agrawal says, when it comes to due diligence, like in the road portfolio, the team physically goes and counts the number of vehicles on the road.

[qt]We are going to ramp down the nbfc corporate book to zero. our focus will be commercial vehicle lending, a great place to be in the nbfc space."

Aditya Joshi, managing director, private equity[/qt]

The first transaction BAM did after Agrawal joined the firm was an acquisition of two road assets from Hyderabad-based KMC Constructions in September 2017. Agrawal explains the rationale behind the deal. “These assets are fundamentally solid, but suffered from a mismatch in the capital structure. So, what we did was, we acquired the asset which was in financial distress, and then we deleveraged it. We completed the construction and now the payments are regularised, and the assets are performing really well."

But the mega deals in BAM’s India portfolio have been its two back-to-back deals with Reliance Industries. The relationship between billionaire Mukesh Ambani’s team and Anuj Ranjan’s team started off on a non-deal basis. But what really triggered the gas pipeline deal was the fact that Brookfield had recently acquired a gas pipeline system in Brazil, and Ranjan’s team was talking about the Brazil asset with them, their operational ability to be able to manage these kind of complex assets, what their learnings had been. On the other hand, it turned out Reliance was also looking to sell its gas pipeline. It only took the team three weeks to go from discussions to the term sheet stage—they started the process of due diligence and the transaction came into being.

Agrawal explains, “For this asset, we were able to leverage off teams in Houston, Calgary, and in Sydney, and they all sort of came together to undertake diligence and see this deal to completion. For example, there is a person in Calgary, who is our upstream expert, who did work on all of these new gas fields so he went into the details of each of those plans and gave us a view on how much gas will flow through that pipe. The person in Houston is an expert in energy investments, and he had worked on the Brazilian pipeline, and he gave inputs on what to look for when you’re doing technical diligence." While teams around the world pitched in to help, the team in Mumbai was usually in Reliance’s Maker Chambers office conducting financial due diligence.

While these deals were pure play infrastructure deals, its acquisition of the telecom towers in a mega $7.6 billion deal follows the more generic theme that Brookfield is betting on—growth of the country. It is trying to identify assets that can fundamentally benefit from the macro growth and for Agrawal and his team the answer lies in the Indian telecom story and the digital wave the country is riding. While 4G in India has been around for less than five years, the country has more than twice the subscribers as the US, which has had 4G for the last 10 years. The team plans to expand the telecom portfolio, which currently consists of 1,37,000 towers, to 1,75,000 towers across the country.

“We had built that comfort over the gas pipeline transaction with Reliance. The way we operate is, we’re extremely open and transparent with each other. Broadly, this deal would fit in three themes—the clean corporate structure, operationally intensive and it rides on the concept of macro growth that we believe in and that’s fundamental to how we look at new opportunities as well," adds Agrawal.

“I am impressed with Brookfield’s operational capabilities and collaborative approach to problem solving. Brookfield is a global enterprise that brings in its best practices to play for making an impact in India. Its talented team in India has been great partners, and our teams regularly engage to discuss various ideas. I look forwarding to further strengthening our partnership with Brookfield and wish them all the success in India and beyond," says Mukesh Ambani, chairman and managing director at Reliance Industries Limited.

*****

For now, the plan for Brookfield is to grow these portfolios in their verticals and expand the business lines around them. The other vertical that is taking shape slowly but steadily for Brookfield in India is its renewables business. In 2020 alone, Nawal Saini, managing director at the firm who oversees the renewables business, has led deals worth $200 million where it acquired the renewable-focussed loan book from Piramal Enterprises Ltd. Though Brookfield did not disclose the deal details, last year, it also acquired Emami Power Ltd, which has solar units in Karnataka, Gujarat, Tamil Nadu and Uttarakhand, and which plans to expand to other states. It currently has a capacity of around 50 megawatts (MW).

Currently, the firm has a 2.7 gigawatt (GW) capacity, including an operating portfolio of wind and solar assets of nearly 557 MW and 2.15 GW of assets under construction in India. Saini, who joined the firm in mid-2018, has managed to deploy nearly $580 million to build the renewables portfolio with his 60-member operational team.

Brookfield made inroads in the Indian renewables ecosystem in 2017, when globally it acquired TerraForm for $1.4 billion adding an over 5,000 MW portfolio of operating wind and solar assets to its existing platform, expanding its renewables footprint in its core markets and establishing operating platforms in new high-growth markets, such as India and China.

By virtue of that deal, it got access to 300 MW in India—200 MW of solar power and 100 MW of wind assets. After Saini joined, until May 2019, he spent time building the operational team, hiring a CEO, a head of commercial department and other department heads. As Saini says, “We wanted the basic building blocks of the team to be in place. After we did that, we acquired a 200 MW wind portfolio in May 2019, which is a very interesting transaction. The way we differentiated ourselves is that we said we will not only buy this asset, we’d also get into a JV agreement through which we will do greenfield development with the partner going forward. This JV today has 1.7 GW of high quality renewable assets in construction and development phase."

Hence, the 200 MW ended up providing BAM a developing portfolio of over 2 GW.

*****

While building assets is one part of the story, in the middle of last year, when the Piramals were looking to sell their renewable debt (mezzanine debt) from the company’s books, Brookfield rushed in to buy it. It gave them an exposure to renewable developers like ReNew Power and Acme Power. It still has an exposure to Acme Power.

“The deal essentially makes us a partner of choice for them. We will use this as an entry point to engage with Acme for their operating and upcoming renewable assets," adds Saini.

Unlike other private equity firms, BAM is hoping to first buy debt and then get a seat at the table to do equity deals. While renewables as an asset class has seen some headwinds over the last few years due to a drop in merchant prices, large firms like Brookfield are confident that renewables is the future.

Another concept where Brookfield is betting big globally is transition funds. These differ from a typical ESG fund in that a transition fund helps companies in the traditional sector to change their input and output materials to green resources, basically transitioning, say, the power source to become net carbon zero through use of this capital.

“We are going to actively participate in the global trend of transitioning into a net carbon zero economy, which we think is a $100 trillion opportunity over the next couple of decades. We can buy into businesses that are carbon emitters, as long as we can underwrite the thesis that we can facilitate the transition of these businesses to a net carbon zero emission, leveraging our operating expertise, clean energy knowledge and access to capital. This opens up a plethora of opportunities," says Saini.

As definitions for sustainable financing and bonds expand to include social bonds, transition bonds and sustainability-linked bonds, renewables isn’t just about solar, wind or hydro anymore. As Saini keeps repeating, “We have to be creative."

Besides these control transactions, Brookfield in India also has a special investments unit which takes care of large-scale structured capital solutions, with equity-linked and equity-like returns. Unlike all the other investments of Brookfield across the sectors it is present in, the special investment team is focussed on non-control situations. The investment mandate is sector and instrument agnostic with solutions for structured growth capital, rescue financings, distressed recapitalisations and hard asset financing.

“We are looking for typically complex situations where you’ve got to underwrite large businesses, which may have complexities around business or legal situations, where you need somebody to move really fast and provide a structured solution for that situation or that environment," says Dev Santani, managing director at the firm who looks after special situations. Santani has deployed $240 million across two deals, including a $130 million investment in Bengaluru-based realtor Total Environment.

“We align our interests with the shareholder or the business owner and add value by giving time and acting like an equity partner," he adds.

*****

In India, Brookfield has dabbled in large deals across asset heavy sectors but, in 2020, it made its first bet in pure play private equity deals. Led by Aditya Joshi who joined as the managing director for private equity at the firm, Brookfield has already deployed $1.5 billion across two deals over the last year or so. It first went and acquired a majority control in Everstone-backed non-banking financial services firm IndoStar Capital Ltd and took over its management. The vertical’s focus will be on buyout and joint control opportunities in financial services, tech services,"¯healthcare"¯and industrials.

Joshi, who joined the firm after working for Apax Partners, read all of Brookfield’s investment committee memos to understand the firm before he started working on the deals. It’s when he realised that Brookfield looks at three to four things in any company anywhere in the world. “How durable is the sector? Is the company providing an essential service? Are there barriers to entry? Is the Ebitda to cash conversion high and can Brookfield add value starting day zero of the investment?" says Joshi. And that’s how he devised his strategy called ‘four by two’—four core sectors and two types of deals (buyouts and equity control deals) with cheque sizes north of $200 million.

And after getting a go-ahead on this strategy from the global head of private equity at Brookfield, Cyrus Madon, Joshi created a heat map to identify their initial target and finally zeroed in on IndoStar Capital.

“They had a very strong strategy towards small-ticket retail lending for commercial vehicles and affordable housing, which are the two segments in the NBFC space that we actually like," says Joshi.

It was a Saturday morning breakfast at Taj Land’s End in Bandra that kicked off this deal in July 2019. And after a long, stringent, due diligence process, Joshi and Ranjan were convinced that this was a platform they wanted to buy into. On January 30, 2020, they closed the deal. Since Brookfield has taken over the management, the NBFC, which earlier had an 80-20 corporate to retail loan book ratio has reversed it to a 70-30 retail to corporate book ratio.

Joshi adds, “We are going to ramp down the corporate book down to zero. Our focus will be commercial vehicle lending, mainly used commercial vehicle lending, affordable housing and SME lending. All three categories are secured lending categories, which is a great place to be in the NBFC space. We will make this into a 100 percent small-ticket retail lending book very soon."

While Joshi took time to close the deal, it wasn’t the first time he was going through the company. At his previous firm, he and IndoStar had been collectively looking at buying another home finance NBFC. While that deal didn’t go through, the learnings remained.

“With respect to IndoStar, Everstone did not sell any shares and was looking for a partner to make a primary investment and buy out other minority shareholders. We have a strong relationship with Anuj and his team at Brookfield. We experienced that they don’t cut corners, are aggressive when they identify what they want, and are long-term commitment partners," says Sameer Sain, co-founder and CEO of Everstone Group.

Sain, who has known Ranjan for over a decade, says that most of their relationships have led to repeat transactions at Everstone. While it bought its first asset in January, by December Brookfield had ended up buying another of Everstone’s asset, Everise, a Singapore-headquartered, next-generation customer experience (CX) solutions and technology company.

“The case with Everise was slightly different. We were eyeing an exit while looking to roll over a small stake in the business. We also realised that given our rollover stake, we were choosing a partner and not just an exit, and once again, the partnership with Brookfield has been extremely positive," says Sain.

Everise first acquired C3, a US-based BPO company, from Stone Point Capital in December 2016.

Over the years, Everise has diversified from a pure-play call centre business into an end-to-end vendor of customer experience management and digital services.

Currently, the platform offers services in healthcare, emerging technology and smart home segments with customers primarily in the US.

“And it’s probably one of the most exciting businesses we’re involved in today. We are looking at other similar types of businesses in the country, I think bolt-ons give an opportunity where we can buy businesses, but also separately operate investment opportunities in the space," says Ranjan, though he adds that the firm is still in its early days with respect to investing in tech start-ups, companies which typically have evolving business plans and lesser visibility on revenues and cash flows.

Though it does not invest in start-ups, to support the ongoing Covid-19 relief efforts across India, it has committed funds towards a non-profit —United Way Bengaluru that is partnering with ACT Grants, a non-profit coalition created by the Indian startup ecosystem to fight the pandemic. These funds will be directed towards the procurement, deployment, and distribution of oxygen concentrators to public medical centres across India.

“But there are incredible cash flow, generative technology businesses, both in software and tech services, that exist in India. And these are companies that can have significant growth, but generate a real yield today. Those are the kind we’re interested in. We’ve learned a lot about the space. And our team in India has done a lot of activity in the sector and I think we will grow pretty dramatically in that space."

As Brookfield taps into various verticals, one question that has come up over time in the Indian deals ecosystem is that big companies have managed to raise more capital, something Ranjan agrees with. According to him, a combination of factors has led to this—the first being few funds can write such large cheques and investors want to go and invest in what they believe is going to be the best in the space.

While Brookfield’s team has been busy working on deals, where does the future lie in terms of investments? Gupta answers after a pause, “We are looking at assets like data centres. While these are still early days in the country, I think the data economy and data infrastructure will be built out in India over the coming years."

While most global firms bring in their expert knowledge to India, in the case of Brookfield, it has taken learnings from India. The firm’s technology capability has actually been built in India and it is now continuing to build that expertise in New York and elsewhere. It is now looking at tech services businesses all over the world with the help and support of the India team as that business model was developed and scaled in India.

As Brookfield readies itself for bigger deals, Ranjan believes the firm is now ready to tackle almost any sector, as it has done deals in varied sectors and that too by cutting the largest cheques in each one of them. Before rushing off to his next meeting, Ranjan says, “Just the fact that India, which did not exist for Brookfield in 2014, and only had a small office in a hotel in 2009, is now approaching half our size in Canada, where the company actually started its operations, is pretty phenomenal."

(Left to right) Nawal Saini, Dev Santani, Ankur Gupta, Aditya Joshi and Arpit Agarwal of Brookfield at their office in Powai, Mumbai

(Left to right) Nawal Saini, Dev Santani, Ankur Gupta, Aditya Joshi and Arpit Agarwal of Brookfield at their office in Powai, Mumbai

“We were able to put together a transaction that spanned four continents. It was a UK-AIM listed entity where while the assets were in India, the structure of the company was held in Mauritius and then there was the holding company. And a lot of the transaction work was being done in the New York office. And that’s the power of the firm that it really comes together when it comes to executing our ideas," says Gupta.

“We were able to put together a transaction that spanned four continents. It was a UK-AIM listed entity where while the assets were in India, the structure of the company was held in Mauritius and then there was the holding company. And a lot of the transaction work was being done in the New York office. And that’s the power of the firm that it really comes together when it comes to executing our ideas," says Gupta. “They came late to India like other Canadian funds but they had a special mandate of deploying capital in the entire gamut of real estate and infrastructure and they have demonstrated their commitment in India. Their commitment to India is enormous and they have deployed huge dollars," says Deepak Parekh, chairman at HDFC Ltd, also pointing out that their board visited India just before the pandemic.

“They came late to India like other Canadian funds but they had a special mandate of deploying capital in the entire gamut of real estate and infrastructure and they have demonstrated their commitment in India. Their commitment to India is enormous and they have deployed huge dollars," says Deepak Parekh, chairman at HDFC Ltd, also pointing out that their board visited India just before the pandemic. While Gupta and Ranjan had met various people over the course of 2015, 2016 and 2017 including the Nair family which owned the asset, in the summer of 2018, Gupta could visibly see that JM was now representing the banks and they were getting close to a resolution.

While Gupta and Ranjan had met various people over the course of 2015, 2016 and 2017 including the Nair family which owned the asset, in the summer of 2018, Gupta could visibly see that JM was now representing the banks and they were getting close to a resolution.