Meet the players blossoming despite the edtech winter

Platforms offering test preparation, certification and skilling are flourishing in a sector that largely faces slump as students head back to classrooms

Last Updated: Oct 17, 2022, 16:41 IST9 min

India’s edtech growth has been through a rollercoaster ride since the pandemic first rattled the education ecosystem. With extreme highs and substantial lows, the perception of the sector has been changing among investors, stakeholders, and in the public eye. The platforms that became unicorns and others that garnered profits during the stay-at-home period of the pandemic are today finding it challenging to meet the changing demand.

Byju’s, for instance, announced last week that it’ll be laying off 5 percent of its 50,000 workforce, translating to 2,000-2,500 employees. The behemoth in the K-12 sector reported a loss of Rs 4,588 crore, almost twice its FY21 revenue of Rs 2,428 crore. With this, as per media reports, around 7,000 employees have been laid off in the edtech sector so far this year.

With schools now operating through physical classes and their own online material, edtech players, especially in the K-12 segment, are having a hard time attracting new customer base, and some like Udayy and Lido Learning, SuperLearn, and Crejo.Fun have had to shut shop.

In 2022 alone, WhiteHat Jr. sacked 300 employees, Toppr, owned by Byju’s, fired 350, and more than 1,000 employees resigned collectively. Vedantu let go of 724 workers in three tranches, and Unacademy laid off 1,000 employees. Around 3,000–4,000 employees have received pink slips from edtech businesses in recent months.

Vamsi Krishna, CEO of Vedantu, says layoffs are a response to staying relevant. “These were cyclic layoffs that have been a response to staying on track and aiming for profitability," he points out. Byju’s and Unacademy declined to respond for the story.

“The pandemic had been a unique occasion where the concept of online got acceptance. Hence, many online players had an unprecedented acceptance of their products and a disruptive growth," says Narayanan Ramaswamy, national leader, education and skill development of KPMG in India. “While the edtech market will continue to grow, it will be difficult to have another situation that can spur growth. Even so, the future spikes cannot have the same magnitude and impact that the pandemic had in a nascent market," he says.

However, while the K-12 segment is impacted due to the reopening of schools, the test preparation, and certification and skilling segments still have many takers for online content, especially in Tier II and Tier III cities where good teachers are scarce. Among all its acquisitions, Byju’s test preparation platform Aakash, for instance, has seen the highest growth throughout the year. Aakash is confident of growing at 60-70 percent by the end of 2022, with its business momentum driven by market demand, hirings, the addition of new centres, and an increase in student count.

Besides, corporate learning companies, too, show a significantly greater growth in job listings, indicating that the category is continuing to grow despite the edtech sector’s recent troubles. Companies such as Pluralsight, Skillsoft, Udemy, and Simplilearn offer a range of instructional video courses for developers, business professionals, and several other roles that are performing better than their K-12 counterparts.

Krishna Kumar, founder and CEO of Simplilearn, says they are seeing an increase in interest in upskilling among professionals through and post the pandemic. “Simplilearn witnessed a 63 percent overall growth in the global consumer business, and 103 percent in the India market in Q1 FY23 (vs. Q1 FY22). Given the industry relevance of our programmes, Simplilearn’s website continues to see consistent learner interest. Additionally, we have noticed a lot of visibility, with a steady rise in users, on our free resources" platform, SkillUp launched in 2020 the platform allows learners to explore in-demand topics in top professional and technology fields," he says.

The platforms targeting higher education are also faring better than K-12 players. Eruditus, for instance, hasn’t been hit bythe reopening of schools or coaching centres, says Ashwin Damera, co-founder and executive director. The company has reported a revenue growth of 70 percent in FY21. “We continue to grow given we operate in a large, growing segment of higher education that will continue to move online for many years to come," he says.

“I think online higher education is a big opportunity. India’s gross enrollment ratio is only 27 percent. If we want that to go to 40 percent in the next 10 years, nearly 15 million new seats in higher education will need to be created. This can’t be done by brick-and-mortar models. So online is going to be a big opportunity and it’s gladdening to see the government is also enabling this through policy framework," adds Damera.

“With K-12, the demand for online picked up when in-person classes were shut. If you look at higher education, nothing shut down, because there was no alternative available. We saw a relatively smaller bump in numbers," says Mayank Kumar, co-founder and managing director, upGrad.

“Besides," adds Kumar, “with the K-12 space, the focus is not on outcomes, it is on access to content. In higher education, you can measure if someone got a job or a promotion for instance, which is why we weren’t hurt badly. This isn"t possible with K-12. Over a period of time, it is difficult to scale an access-led model."

UpGrad has acquired Impartus Innovations, KnowledgeHut, Talentedge, Work Better Training as well as Global Study Partners to expand its offerings, and is looking at the US as its next big growth opportunity. Last August, it closed a $185 million funding round from Temasek Holdings Ltd, International Finance Corp (IFC), and IIFL Group, at a valuation of $1.2 billion.

Outcome is a play that K-12 players now seem to be turning to, Kumar feels, to tide over loss-making times. “Most K-12 players are moving more and more towards outcome-led models," he says. But, in the early days of the pandemic, a lot of these players didn"t anticipate what would happen once schools began.

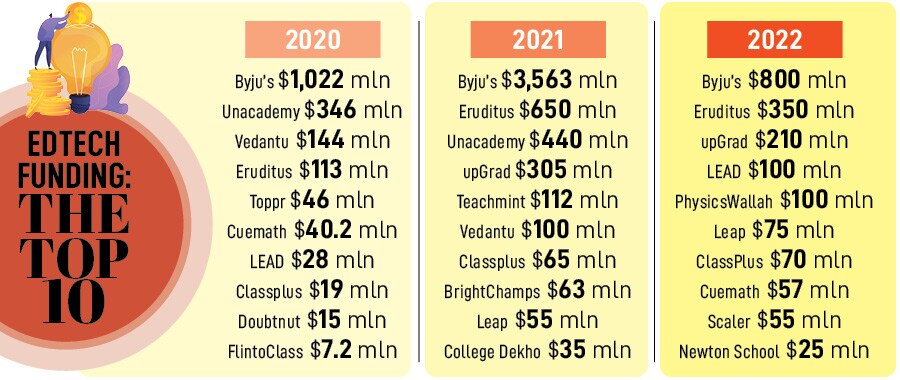

The online education market, which includes K-12, higher education, and upskilling in India is, at present, worth around $1.9 billion. By the end of 2021, edtech was riding on an unprecedented funding boom. With more than $4.7 billion in funding across 165 deals, it was the third most favourite sector for investors.

This, however, changed in 2022. According to Fintrackr’s data, around 17 edtech startups, including Byju’s, upGrad, Teachmint, Classplus, LEAP, Quizizz, Eupheus Learning, and Leverage Edu, scooped up two or more rounds in 2021. However, the number of startups doing so dwindled to zero by August end.

Investor enthusiasm for the sector is also slowing down. Until August 15, funding for edtech businesses fell precipitously from $5.82 billion to $2 billion. Only two edtech agreements were completed in August.

“There is a marked slowdown in investor interest in the market in 2022. While this is primarily due to the reduced rate of expansion of many companies and increased costs in customer acquisition, it is also due to the absence of any noticeable innovation by existing players," says Ramaswamy of KPMG.

Adds Aditya Arora, CEO of Faad Network Private Limited, an investor network that assists early-stage startups: “Investors are now looking at more specific use cases that edtech players are solving the problem for. Increasing questions on customer acquisition cost and burn rate, especially in the light of the downturn in the economy, are becoming central to investment decisions. Investors are now grilling about the numbers more than ever."

Why has K-12 become the worst-affected in the industry? Because, with social interactions and in-class learning being prioritised by the parents of school-going students, the interest in taking up online aid for schooling has substantially gone down. Media reports claim thousands of customers are engaged in prolonged tussles with companies to cancel course subscriptions and retrieve the fees paid by them. There are also some complaints regarding the misuse of data pertaining to students.

Udayy, launched right before the pandemic in 2019, was one such company that saw surging adoption in the early months of the pandemic. “The product was doing great then, we saw a lot of adoption and we raised a lot of capital as well on the back of those numbers," says Saumya Yadav, the co-founder. But adoption went south once schools reopened.

In April, after close to nine months of figuring out other business models, Udayy closed operations. “We were spending effort and a lot of money in figuring out different kinds of pivots and changes to the business model that could make it more viable. And once we ran out of those options, we realised that the core product is just a vitamin and not a painkiller. And in this environment when there’s no pandemic, the other options we were thinking about were just stop-gap solutions," she says.

Yadav and her team did consider turning hybrid, but, she says, “It made sense for certain players who were in the test prep segment. But our target group was kids from grade 1 to grade 5, and going to a coaching class wasn"t common behaviour. From a business perspective, it didn"t make too much sense."

Interestingly, it wasn"t that the business ran out of money. Yadav adds, "When we were making this decision, we still had $10 million in our banks and weren’t raising more money. So the decision was coming from a place of strength, not desperation."

Says Ramaswamy: “In general, the growth in customer acquisition—particularly in newer markets—has been challenging. So some players have stopped their foray into newer domains. Many of them have also trimmed costs—including manpower costs—which resulted in retrenchment in certain cases. There has also been a trend to get some foothold into the physical classroom space by some of the larger players who were hitherto focussed only on the online market."

As a response to meet the changing demand, most of the edtech unicorns ventured into the offline market through acquisitions or opening up of physical centres. Vedantu, for instance, has physical centres along with its online-first approach. “The idea is to increase the options available to the student," he says. Byju’s, too, has opened offline centres.

Some of the K-12-centric players are also expanding offerings to include AI/VR, leading to the prominence of subjects like robotics and coding. Vedantu, for instance, has been focussing on creating AI-focussed courses. “There is a huge scope for innovation in edtech. Just like any business cycle, there are going to be ups and downs. Where online education for K-12 triumphs is the fact that good educators aren’t easily accessible in Tier II and Tier III cities. So there will always be the scope of growth, because online education bridges the geographical gap," says Krishna of Vedantu.

“Conventional K-12 online learning platforms are shifting to methods and offerings that are practical and have a specific use case for students," says Arora. “Byjus, Unacademy, Vedantu, among other giants, have introduced coding and robotics, and increased focus on AI with a shift to the 3D user experience are all steps to stay relevant. Only a blend of conventional schooling and newer subjects can help edtech players sustain in the long run," he adds.

“Edtech could be an answer to address the needs of equity and reach required in the Indian market," says Ramaswamy. “Edtech companies need to reinvent themselves beyond the digitisation of content, video-based learning, and online channel. Innovations across the value chain – including in key areas such as customer acquisition, retention, and reach is the need of the hour."

First Published: Oct 17, 2022, 16:41

Subscribe Now