Govt's divestment plans likely to flop in FY24, once again

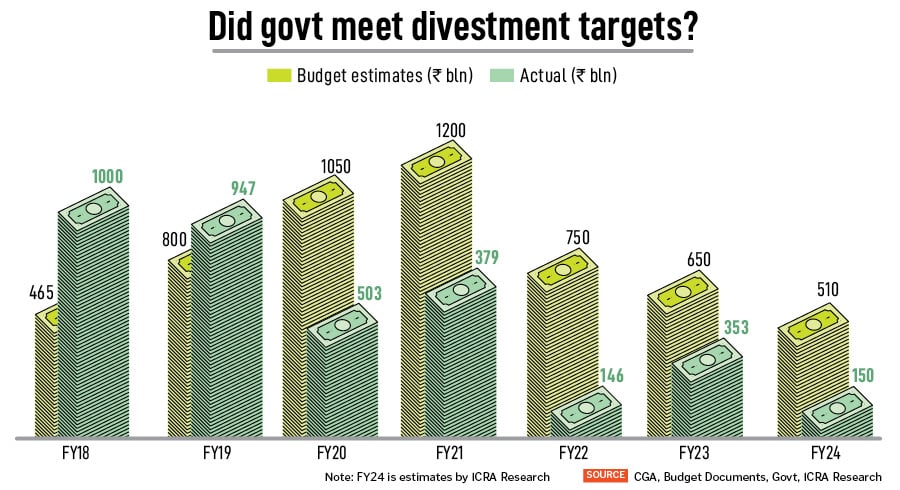

As the government is likely to miss its divestment target for the fifth consecutive year in FY24 by a wide margin, expectations for the new fiscal in the interim budget is not high as previous stake s

Without meeting the divestment targets, overall revenues for the government could be strained by the end of FY24

Illustration: Chaitanya Dinesh Surpur

Advertisement

Well, it is no more surprising, if the same thing is repeated for five years. There is no doubt that the government’s divestment plans laid out in Union Budgets is mostly ambitious, but it has hardly met its own target. For the fifth consecutive year, the government is unlikely to meet the divestment target of FY2024 by a wide margin, with hardly three full months left for the fiscal closing.

The government aimed to garner Rs 51,000 crore (Rs 510 billion) by end of March 2024 by selling stake in public sector undertakings (PSUs). However, that looks unachievable, considering from April to November 2023, the government has mopped up only Rs 8,860 crore, which is merely 17.4 percent of the budgeted estimates.

As on January 11, the total receipts from divestments for the government was Rs 10,050 crore, shows data provided by the Department of Investment and Public Asset Management (Dipam). This includes sales of the government’s stake in Coal India, Rail Vikas Nigam, SJVN, Housing and Urban Development Corporation Ltd, IRCON International and Hindustan Aeronautics through the offer-for-sale (OFS) route. There was just a single listing of shares of a PSU company called Indian Renewables Energy Development Agency in which the government sold a 10 percent stake for Rs 860 crore, through the initial public offering (IPO) route.

Garima Kapoor, economist, Elara Capital says that earlier in FY24, the economic environment was quite uncertain mainly due to the Russia-Ukraine crisis and a sharp rise in commodity prices like crude oil. She explains that while bids for the IDBI stake sale were received, the vetting from Reserve Bank of India (RBI) took a long time. Additionally, the ongoing political tension with Canada may delay the procedure as one of the bidders as per media reports was Prem Watsa-backed CSB Bank from Canada. Moreover, robust tax collections as well as surplus transfer from the RBI and other government-run companies meant that the central government will be able to achieve its FY24 fiscal deficit target, despite the underachievement on disinvestment. “As such, the urgency to conclude the process was not very compelling," she adds.

Without meeting the divestment targets, overall revenues for the government could be strained by the end of FY24, Kapoor fears. She expects the central government to undershoot FY24E fiscal deficit target by 10 basis points as net tax revenue growth of 16.3 percent versus 11.7 percent budgeted and non-tax revenue growth of 30 percent versus 15.24 percent budgeted would help offset the shortfall in disinvestment receipts and accommodate higher spending on account of food, fuel and fertiliser subsidy and higher allocation to MGNREGA.

In FY24, the government was also working on privatising PSUs like Shipping Corporation of India, NMDC Steel Ltd, BEML, HLL Lifecare, Container Corporation of India and Vizag Steel, besides IDBI Bank.

According to Indranil Pan, chief economist, Yes Bank the shortfall in achieving the divestment target for FY24 is likely due to the government’s decision not to pursue disinvestments aggressively, opting instead for proper valuations to maximise revenue. “This approach seems to stem from a comfortable revenue position, with tax collections exceeding budget estimates and certain non-tax revenues, like RBI dividends, also surpassing expectations," he elaborates.

With the upcoming election and the imminent implementation of the Model Code of Conduct (MCC) just months away, there appears to be limited scope for advancement in big-ticket divestment initiatives, says Care Ratings. “The big-ticket divestment initially planned for this year involving IDBI Bank now appears uncertain. Previous attempts to divest from BPCL and Pawan Hans were unsuccessful, and stake sales in the Shipping Corporation of India are currently hindered by the demerger of land assets. The projected Rs 36,000 crore shortfall in the non-debt capital receipts due to slow progress on divestment is expected to be covered by better-than-budgeted performance of tax and non-tax revenues," Care Ratings adds.

What about divestment in FY25?

Most economists expect the government to set a moderate target for divestment, keeping in mind the general elections starting in April. Aditi Nayar, chief economist, Icra estimates disinvestment target to be likely to be pegged at sub-Rs 50,000 crore for FY2025. “Given the uncertainties involved in market transactions, it would be prudent to set a moderate target of sub-Rs 50,000 crore for FY2025, instead of a higher aim that may disrupt the budget math if there is a large shortfall in such receipts by the end of the fiscal, based on the past year trends," she adds.

Kapoor agrees. She does not have high expectations from disinvestment in FY25 as it is an election year. By the time the full budget is passed, it will be well past July. “The government could target strategic sale of IDBI Bank since it is at an advanced stage of conclusion. Apart from that the government could accelerate sales via OFS in a few listed PSUs, especially since the performance of PSUs has improved. Overall, we do not expect more than Rs 35000-Rs 40000 crore worth of disinvestment proceeds," she says.

Rahul Bajoria, MD and head of emerging markets Asia economies (ex-China), Barclays, also sees divestment target for FY25 to be low as he feels this revenue stream is losing its relevance at the margin.

In FY24, the government was also working on privatising PSUs like Shipping Corporation of India, NMDC Steel Ltd, BEML, HLL Lifecare, Container Corporation of India and Vizag Steel, besides IDBI Bank.

In FY24, the government was also working on privatising PSUs like Shipping Corporation of India, NMDC Steel Ltd, BEML, HLL Lifecare, Container Corporation of India and Vizag Steel, besides IDBI Bank.