We do not wait for the house to catch fire and then act: RBI Governor Shaktikant

The RBI governor says policymakers have to be mindful of the risk of being carried away with a few months of good data and also be watchful of the risk of overtightening

RBI Governor Shaktikanta Das

Image: Reuters/Susana Vera

Advertisement

In the last policy meeting of this calendar year, the Reserve Bank of India’s (RBI) six-member rate-setting panel voted unanimously to keep the repo rate unchanged at 6.5 percent and five of the six members voted to remain focussed on the withdrawal of accommodation. The central bank raised its GDP growth forecast from 6.5 percent to 7 percent for FY24. It held its inflation projection at 5.4 percent for the current fiscal year.

“The fundamentals of the Indian economy remain strong with banks and corporates showing healthier balance sheets fiscal consolidation on course external balance remaining eminently manageable and forex reserves providing cushion against external shocks. These factors, combined with consumer and business optimism, create congenial conditions for sustained growth of the Indian economy," RBI Governor Shaktikanta Das said.

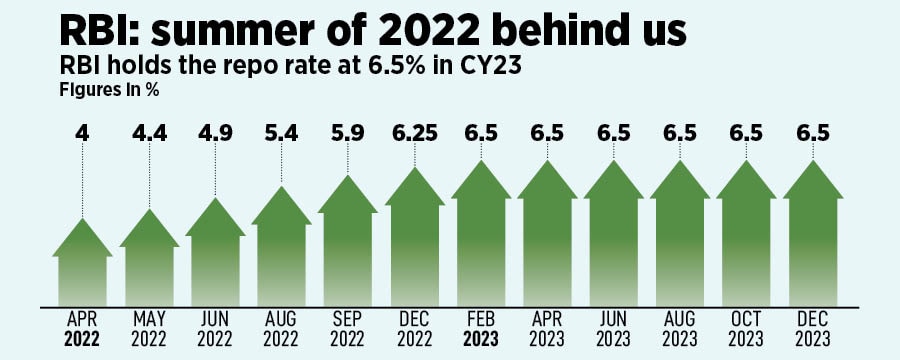

The central bank was not as hawkish as anticipated by markets. Between May 2022 and February 2023, the monetary policy committee (MPC) increased the benchmark lending rate by 250 basis points from a historic low of 4 percent. Since its first credit policy meeting this calendar year, the MPC has held the repo rate at 6.5 percent (see table).

“Our policy of prioritising inflation over growth, hiking policy rate by 250 basis points in a calibrated manner and draining out excess liquidity have worked well, alongside supply-side measures taken by the government, to bring about this disinflation," Das added.

But inflation is still a concern. In its December meeting, the RBI projected inflation at 5.6 percent and 5.2 percent in the third and fourth quarter of this fiscal respectively. In the first quarter of the next fiscal, it estimates inflation at 5.2 percent, 4 percent in the second quarter, and 4.7 percent in the third quarter.

The RBI governor is watchful of possible second round effects largely on account of uncertain food prices: “There has been broad-based easing in core inflation which is indicative of successful disinflation through monetary policy actions. The near-term outlook, however, is masked by risks to food inflation which might lead to an inflation uptick in November and December. While monetary policy would look-through such one-off shocks, it has to stay alert to the risk of such shocks becoming generalised and derailing the ongoing disinflation process."

On the growth front, the central bank was more confident. It raised its growth forecast for the current fiscal by 50 bps and projected GDP growth in third and fourth quarter of FY24 at 6.5 percent and 6 percent respectively. It sees GDP growth at 6.7 percent, 6.5 percent, and 6.4 percent in Q1, Q2, and Q3 respectively in the next fiscal.

The RBI noted a gradual turnaround in rural demand and said investment activity continued to be supported by strong public sector capex. It also expects the impact of weak external demand to moderate on the back of higher goods and services exports.

“Looking ahead, private consumption should gain support from gradual improvement in rural demand, strengthening of manufacturing activity and continued buoyancy in services. The healthy twin balance sheets of banks and corporates, high-capacity utilisation, continuing business optimism and government’s thrust on infrastructure spending should propel private sector capex," Das explained.

But the RBI governor cautioned that the global economy is showing signs of slowdown. “The protracted geopolitical turmoil, volatility in global financial markets and growing geo-economic fragmentations, however, pose risks to the outlook," he added. “The long-awaited normality still eludes the global economy. The years 2020 to 2023 will perhaps go down in history as the period of ‘Great Volatility’, comprising a host of black swan events in quick succession."

Given the range of uncertainties, Das reiterated the need to ensure that the monetary policy remains actively disinflationary to ensure a durable alignment of headline inflation to the target of 4 percent while supporting growth.

“Policymakers have to be mindful of the risk of being carried away by a few months of good data or by the fact that CPI inflation has come within the target range. They have to be also mindful of the risk of overtightening, especially when large structural changes, geopolitical and geoeconomic shifts are taking place. On top of this, they have to be watchful of the risks from new shocks that could hit the economy from anywhere anytime," Das said.

Equities and bond markets were trading in the green. The S&P BSE Sensex was up by nearly 160 points and the ten-year bond yield was higher by 0.1 percent at 7.24 at 1 pm on Friday.

Akhil Mittal, senior fund manager, Tata Asset Management, says the policy outcome seems to be positive for markets: “With policy largely in line with expectations and no mention of Open Market Operation (OMO) sales, which led to sell-off in last policy review, we expect markets to perform better and yields to come-off 5-10 bps across the curve."

Lakshmi Iyer, CEO-Investments and Strategy, Kotak Alternate Asset Managers, says the upside in bond prices may be limited given India’s CPI data and impending US FOMC decision: “The upward revision in GDP growth estimates would mean continued momentum in equities as well as interest rate sensitive (sectors). The RBI has not sounded as hawkish as the markets expected hence bond yields may ease a tad. Rates seem to have peaked out and hence rise in yields could be an opportune time to add duration to one’s portfolio."

Most economists and analysts expect the RBI to stay the course and keep rates unchanged for the next two quarters. Brokerage firm Nomura predicts 100 bps of cumulative rate cuts from August next year as inflation moderates and growth tapers.