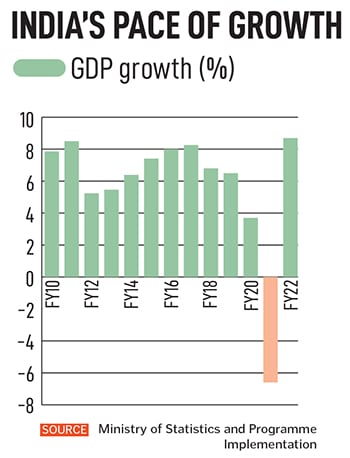

Is 6% growth possible? Nirmala Sitharaman has her work cut out

This is the first 'normal' budget since 2020 but challenges are still galore. Tight monetary policies, an impending recession, Russia-Ukraine, and China-US. But India has been an outlier, can it conti

Jet Airways has not flown since April 2019 and is now targeting to take off as early as April 2023.

Image: Ritesh Uttamchandani/Hindustan Times via Getty Images

Advertisement

In an election year, keeping expenses down will be tricky. As the government has shown with an extension of the free food scheme, there is every chance of the subsidy bill going out of control. At ₹532,446 crore, the subsidy bill for FY23 is the second highest since ₹706,006 crore was spent in FY21. The war in Ukraine is likely to add ₹2.2 lakh crore to the fertiliser subsidy bill for FY23. As a result, economists are unanimous in saying that there is little scope for the government to provide any relief in the form of lower taxes or a stimulus.

In fact, Shukla of Mahindra says there should be a concerted effort to not provide any stimulus assuming there are no external shocks or a monsoon failure. Barua is certain that the correlation between fiscal expansion and an election year will not hold true this time as “there is a deep realisation in the government that the debt situation is untenable".

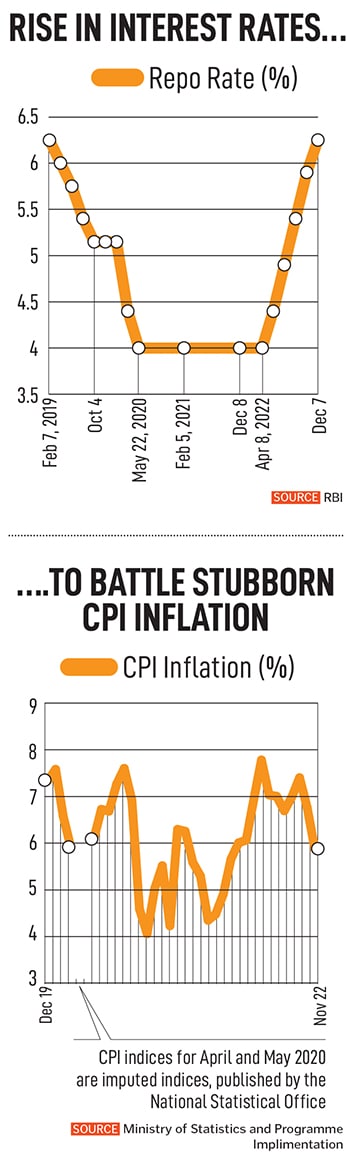

Interest Rate Cycle Close to Peak

In order to get growth up, there are few avenues the government could explore. First, ramp up capital expenditure. While there are signs that private sector capex is picking up, government capex will have to do the heavy lifting, as it has done in the past few years. Secondly, attract companies relocating from China with incentives for setting shop in India. This would again come with tax incentives. Third, keep the services engine running, with domestic tourism and hospitality being key drivers.

Barua believes one of the tricky issues of whether rates would continue to rise more in 2023 has been answered. “Most of the rate increases are done," Barua says.

Banks are sensitive to the fact that the demand for credit could contract and you could attract low-quality borrowers, something which the RBI and banks do not want. Barua is not ruling out a reversal in the interest rate cycle by mid-2023, where falling commodity prices and global recession are real factors to deal with.

One of the factors making Barua positive is that capacity utilisation rates for companies have increased to 74 percent from sub-70 percent. Cement, automobile, electronics manufacturers have been approaching banks seeking term loans, without being too sensitive to currently high interest rates. “They appear to have built-in margins on interest rates," Barua says. The strategy towards borrowing at this stage could be that by the time capacity comes on stream, the worst of global recession would have been behind them.

Whether this borrowing will translate into a deep and sustained private sector capex cycle is still unclear and a while away. Mahesh Vyas, the managing director and CEO of the Centre for Monitoring Indian Economy (CMIE), says “the saga of corporates remaining reticent of investing into new capacities has apparently continued into 2022-23", in a December 1, 2022, column on CMIE’s website.

“Financial statements of 3,110 listed companies show their net fixed assets grew by a meagre 3.5 percent year-on-year in nominal terms as of September 2022. It seems likely that 2022-23 would be the third fiscal year in which corporates will have stayed away from expanding their productive capacities," Vyas adds.

Domestic Consumption Story Intact

There are, however, some positives playing out on growth, particularly in fast-moving-consumer goods (FMCG) and the housing sector. Saugata Gupta, managing director and CEO of Marico, believes that the domestic consumption story for India remains intact after disruptions like the pandemic, and even inflation.

“The slowdown was inflation-led and food constitutes a significant portion of the consumption basket. Whenever there is food inflation, people tight rate or down trade on FMCG. During 2021 and 2022, the alternative channels of consumption were not available the share of wallet got transferred into healthy hygiene, immunity boosters. As the economy opened up, spending has shifted towards travel and hospitality," Gupta tells Forbes India. Marico, whose best-selling brands include Saffola cooking oil and Parachute coconut oil, is in a silent period and Gupta could not comment on the specific strategies being drawn out for consumer brands in 2023.

But in rural India, during the slowdown, families down trade in high consumption categories such as soaps, detergents and hair oil. In the case of low penetration items, they would usually tight rate on items such as nutrition drinks, or at least not up trade from non-branded to branded products. This trend which was seen for the past two to three quarters, is now easing.

“The consumption story is recovering and the worst of the inflation is mostly over. The consumption trends are gradually stabilising. I am fairly optimistic about growth in 2023," says Marico’s Gupta. It will be a gradual improvement in consumption, but the trend will not be a hockey stick graph. “Though not insulated, we are in a far better space then the rest of the world," he adds.

Despite rising interest rates—of 225 basis points for 2022—and costlier home loans, the demand for housing has rebounded across various segments of real estate, including high-end, from an obviously sluggish trend during the pandemic. The real estate market would normally appear challenged due to costlier home loans (where interest rates have ranged between 6.75 percent to 8.4 percent) and a delay in closure of transactions, as potential buyers would wait to determine home loan EMIs, as rates rise.

“The on-the-ground reality is slightly different. Demand for real estate is very high and people want to buy homes, and not remain limited to rental property. We saw bullish trends in 2022 and I am confident that it will continue into 2023," says veteran real estate developer Niranjan Hiranandani, who has co-founded the Hiranandani Group.

His optimism has been backed by the fact that home loans and loans against property have been some of the fastest-growing verticals within retail banking for most banks in the April to September 2022 period. HDFC, the country’s largest mortgage lender, reported a 20 percent growth in its individual loan book on an assets under management basis and a 36 percent growth in individual disbursements for the half-year ended September 30, 2022.

Hiranandani is confident that the real estate sector will grow at a “minimum of 10 percent in any of its segments" in 2023. He expects interest rates to rise a further 50 bps beyond which it would be counter-productive. “Any further increase in interest rates beyond 50 bps will be counter-productive and will cause inflation, as there is a cost input," Hiranandani says.

Business leaders and economists would wish that the interest rate cycle is near its peak, but the minutes of the last monetary policy meeting of the RBI suggested that the central bank will remain vigilant and, as per RBI Governor Shaktikanta Das, there was “no room for complacency" against inflation.

Sitharaman’s task to push further for growth is going to be an arduous one. She will have to hope for sustained push for growth from the services sector, even as manufacturing seeks to get its act right. The news from the Western economies is likely to impact her best intentions.

Barua believes one of the tricky issues of whether rates would continue to rise more in 2023 has been answered. “Most of the rate increases are done," Barua says.

Barua believes one of the tricky issues of whether rates would continue to rise more in 2023 has been answered. “Most of the rate increases are done," Barua says. But in rural India, during the slowdown, families down trade in high consumption categories such as soaps, detergents and hair oil. In the case of low penetration items, they would usually tight rate on items such as nutrition drinks, or at least not up trade from non-branded to branded products. This trend which was seen for the past two to three quarters, is now easing.

But in rural India, during the slowdown, families down trade in high consumption categories such as soaps, detergents and hair oil. In the case of low penetration items, they would usually tight rate on items such as nutrition drinks, or at least not up trade from non-branded to branded products. This trend which was seen for the past two to three quarters, is now easing.