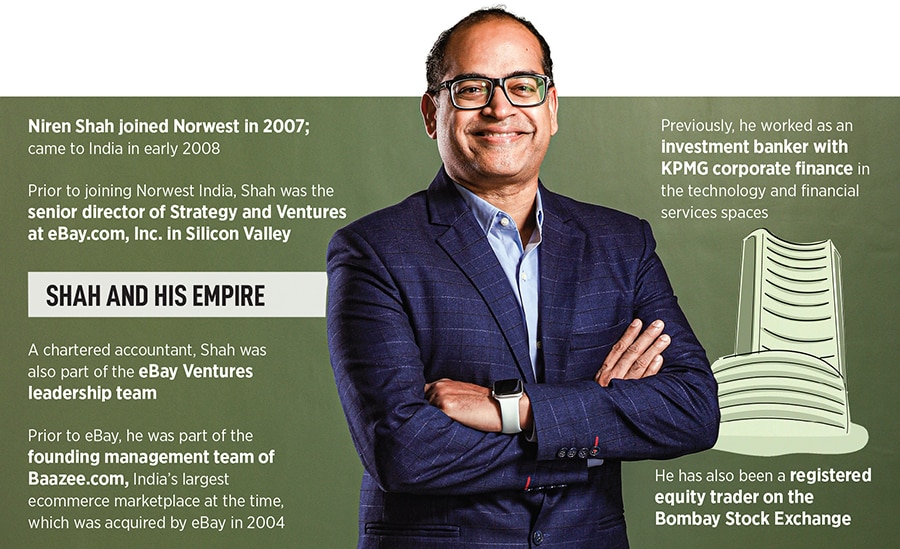

Shah indeed was quick. “Kitna revenue hai, kitna profit hai and management kaun hai (how much is the revenue, profit and who all are in the management)?" he asked in one go. A chartered accountant and investment banker, Shah joined American investment firm Norwest Venture Partners (NVP) in 2007 and came to India in early 2008. Mohapatra was equally brisk in his reply. “We will start posting revenue from next month. So there is no question of profit," he underlined. Shah paused for a while, glanced at the rookie founder and continued munching. The meeting ended. Shah passed on the opportunity.

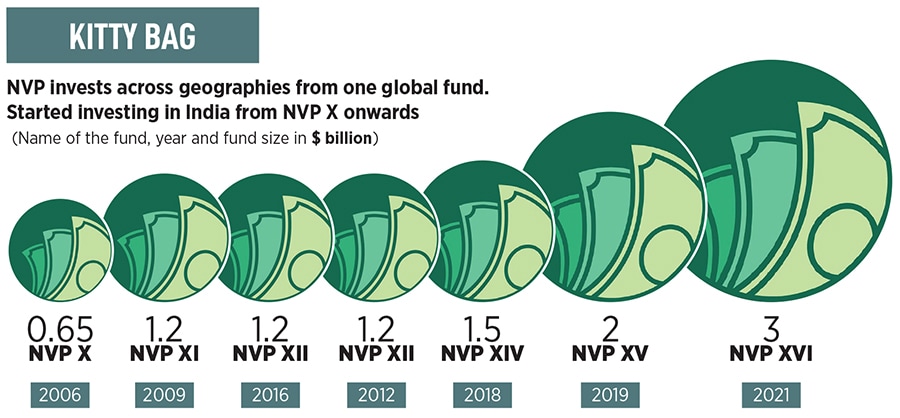

Back in 2008, Shah was camping in one of the villages around Alibaug, around 95 km from Mumbai. It was an age of microfinance, which had fast emerged as the darling of investors. “Back then, it wasn’t cool if you didn’t have exposure in microfinance," recalls Shah, who decided to test the waters. The VC was taking tentative steps in his formative days at Norwest, which made its first investment in India when it backed Persistent Systems, a leading offshore product development company based out of Pune, in December 2005. Three years later, in January 2008, the American firm set up its India team, and now Shah was scouting for his maiden bet. The herd instinct in the market was strong, the temptation to pluck a low-lying fruit was equally compelling and Shah was busy testing his own investment thesis.

Fast forward to 2012. The funder, along with his young team, was standing outside a huge garbage dump. There was an opportunity to invest in a waste management company which had grown at an amazing clip and had ticked all the boxes in terms of revenue, profit and cash flow. A comforting barometer for any firm looking to invest was the fact that the company had borrowed money from a bunch of reputed banks. What this meant was the business was clean. “We were counting the number of garbage trucks visiting the site every day," recounts Shah, who was in the midst of his regular due-diligence exercise. “The numbers were not adding up," he says, alluding to an expected mismatch in revenue quoted and reality. “Where are the trucks? They were missing. Looked like something was fishy," he adds.

Meanwhile, six years later, in 2018, Shah was close to hitting a jackpot. An opportunity came knocking at one of the top-valued startups in the country—Shah refuses to divulge the details—which was raising its umpteen round of growth capital. Shah’s eyes lit up, and he decided to pursue the opportunity. The entrepreneur, though, hurled a weird requisite. Shah was not allowed to do the due diligence. “But why?" asked an inquisitive VC. “People bigger than you have not done it. So you too can’t," was the reply. “Either follow them and enter, or be out," came the parting remark.

![]()

Back in Mumbai, Mohapatra decided to try his luck again in November 2017. OfBusiness had closed FY17 at an operating revenue of ₹216 crore. “This time the meeting lasted for over 20 minutes," smiles Mohapatra, who had raised $12-13 million in funding by now. Two things, though, didn’t change. First, was the same three questions. And second was the result. “We have healthy revenue," the co-founder underlined. The burn too, he stressed, is under control at ₹40 lakh per month. Shah declined to fund.

A year later, Mohapatra was back. “This time I had ticked all the boxes," he says. Shah completed his Q&A ritual, and decided to invest. “After that he never asked any questions," laughs Mohaptra. OfBusiness closed FY22 with an operating revenue of ₹6,363.83 crore, a profit of ₹125.63 crore, Ebitda margin of 2.98 percent and a cash outflow from operations of ₹798.85 crore. “Shah looks for stability, profitability and sound management," he says, adding that the investor will continue to stay away as long as he is not 100 percent convinced. “It’s not easy to get his money, but is a great guy to have on your cap table," underlines the entrepreneur whose venture is headquartered out of Gurugram.

![]()

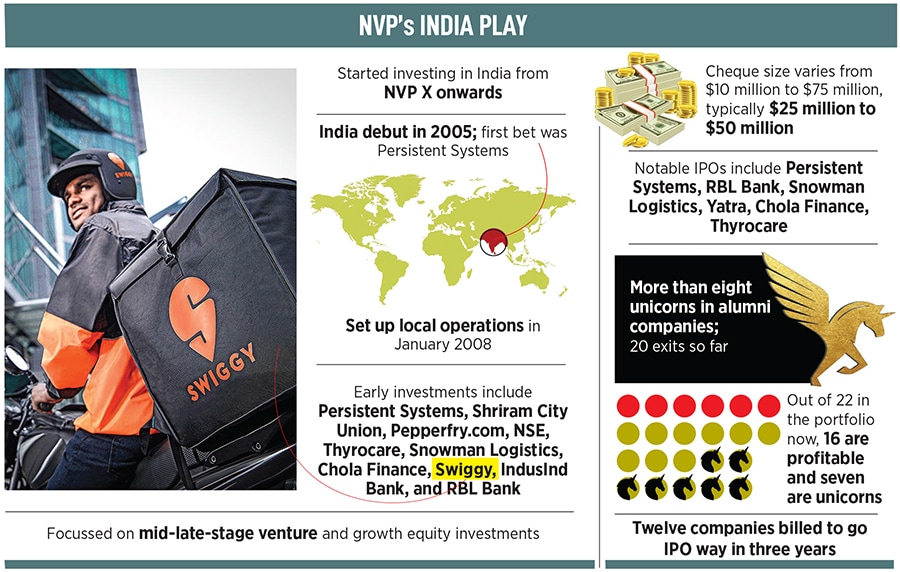

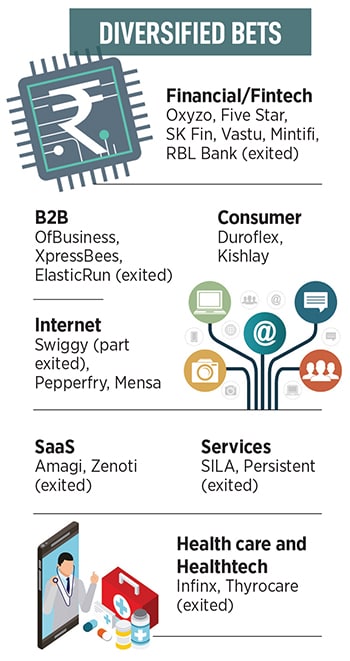

Meanwhile, in Mumbai, Shah shares the track record of Norwest. “We have the highest slug ratio," says the managing director and head of Norwest India. In baseball, slug ratio is how many hits one has had as compared to misses. “I can guarantee you that that amongst venture capital, we will have by far the highest slug ratio," says the investor. His expansive office on the 15th floor of the Express Tower at Nariman Point is as quiet as the overlooking sea. Out of the 22 companies in the portfolio, 16 are profitable, and seven are unicorns. While a bunch have had their public market debut—RBL Bank, Thyrocare and Snowman Logistics to name a few—around a dozen are billed to hit the IPO street in three years.

![]() So what’s the secret sauce? Shah explains. “You have to dodge a lot of bullets," he reckons. The first seven years of the fund’s operations in India, he underlines, was all about dodging as many bullets as possible. “We only did the deals which were so compelling that we could not say no," he says. “And that has really worked for us," he stresses, adding that the investment in Sriram City was his first deal with a cheque size of $28-30 million.

So what’s the secret sauce? Shah explains. “You have to dodge a lot of bullets," he reckons. The first seven years of the fund’s operations in India, he underlines, was all about dodging as many bullets as possible. “We only did the deals which were so compelling that we could not say no," he says. “And that has really worked for us," he stresses, adding that the investment in Sriram City was his first deal with a cheque size of $28-30 million.

Two things stood out in the first bet. First, by any standards, the cheque size was huge for the American firm. Second, Norwest was not used to place bets on companies in financial segments. Given the professional and academic background of Shah—he was the CFO and part of the founding team of Baazee which was bought by eBay in 2004—looking for sectors where returns were most likely guaranteed made sense. A cursory look at some early investments made by Norwest will reveal a strong financial bias: Persistent Systems, Shriram City Union, Chola Finance, IndusInd Bank and RBL Bank. There were other big bets as well such as Swiggy, Thyrocare and Pepperfry.

![]()

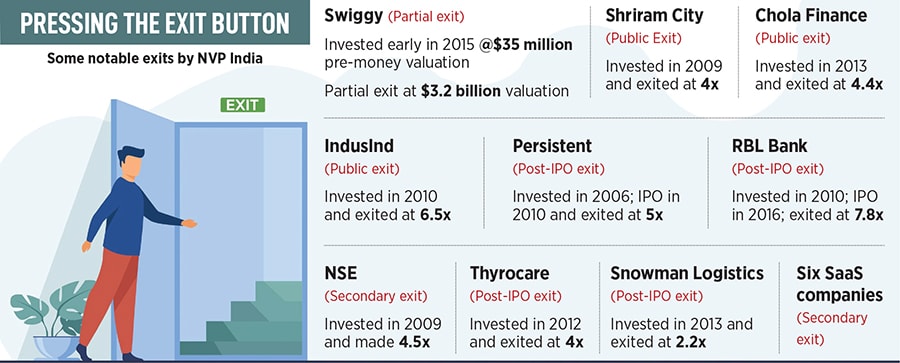

In the early years, having a sedate approach made sense for Norwest. “Not only were we conservative, we’re very thoughtful and contrarian," contends Shah. Back in 2008, India was a different country and the ground realities too were distinct. One of the investment thesis, Shah explains, was built around India’s low GDP per capita. This meant that monetisation would take longer than usual. Having a control over unit economics made a hell lot of sense, especially because the GDP per capita was not like China or the US. “To create value in such environment, one must have high exits," he says. The amount Norwest sold and exited by 2017 was more than one-and-a-half times or so which the fund invested. “No other fund has done that," he claims. Last year, Norwest invested around $380 million in India. “We realised that this is going to be a very long and patient game," he says.

![]()

Shah, interestingly, laid down his own set of rules to play the game. “We set a very high bar on ethics and integrity," he points out. Rolling out operations in a new country came with a lot of unexpected variables. The best way to deal with uncertainties, Shah underlines, was to play with a straight bat. While vetting deals, three things were sacrosanct. First, the level of governance among the companies must be quite strong. Second, the companies must be transparent. Third, the business fundamentals and model have to be unquestionable. “It’s easy to drop your bar because something is hot," he says, alluding to the numerous investment opportunities that Norwest ignored. Take, for instance, it didn’t fund the waste management company that it was evaluating. It also didn’t back the ventures where diligence was not allowed. It stayed away from sectors where the possibilities of making money looked slim because of inherent issues plaguing the segment, such as microfinance or payment tech companies. “The books have to be clean, the founders have to be exceptional," he says.

Realising the right role of an investor also brought about immense clarity in functioning. “India is like a boxing ring. It’s hard. It’s competitive," says Shah. Not getting confused, he lets on, about who is fighting in the ring is crucial. “Our founders are donning the gloves, and we are standing outside with a towel," he says. An investor, he reckons, might suggest how to throw the best punch, but the call is always with the fighter. Having loads of empathy and not trying to change something midway is what differentiates the fund, he adds. “We are backing amazing founders, not normal founders," he underlines.

![]()

Ananth Narayanan happens to be one such entrepreneur. “In our case, Niren had bet on the founding team," reckons the former chief executive officer (CEO) of Myntra, who joined Medlife as co-founder and CEO in August 2019. The company got eventually acquired by Pharmeasy and in May last year, Narayanan rolled out Mensa Brands, an ecommerce unicorn. “I know him since my Medlife days," he says, adding that Shah didn’t invest in Medlife. When Narayanan decided to launch a new venture, Shah was one of the first funders to call him. “His backing was more out of his conviction of for the founder and team," he says.

![]() When asked to select a single quality which sets Norwest apart in a cluttered VC space, the entrepreneur talks about the freedom that the fund brings in. “They will get involved only when you want them to," he says. What also clicked between Shah and the founder was the common belief in building a sustainable business. “After my Myntra and Medlife experience, I wanted to build a business for the long term," he says. “This resonated with Norwest. They are very thoughtful investors," he adds.

When asked to select a single quality which sets Norwest apart in a cluttered VC space, the entrepreneur talks about the freedom that the fund brings in. “They will get involved only when you want them to," he says. What also clicked between Shah and the founder was the common belief in building a sustainable business. “After my Myntra and Medlife experience, I wanted to build a business for the long term," he says. “This resonated with Norwest. They are very thoughtful investors," he adds.

But is there a flip side to his strategy? Has staying ultra conservative—Shah though labels it as ‘thoughtful’—meant that the fund has missed out on some opportunities which it could have easily lapped up? Shah does a candid assessment. He takes us back to one of the early rounds of Flipkart funding. Shah was putting in money at a valuation of $150 million. Flipkart, interestingly, was seeking $200 million. Shah reluctantly decided to stretch to $160 million, which was then eight to nine times the GMV (gross merchandise value). The deal didn’t happen. “Look where they went. I regret missing out on it," he rues.

Another interesting miss was Nykaa. The investor looked at a wide spectrum of beauty companies that couldn’t make the mark. “The math didn’t add up," he says, explaining why he let the opportunity pass. Each lipstick then, he underlines, used to cost around ₹80, and one had to spend ₹50 for delivery as well. “How would you make money," he wondered. What, though, he failed to estimate was the enterprising quality of the founder. “Falguni Nayar did a great job," he says. The company, he points out, ended up selling packs of five and 10. “I got it wrong," he says.

![]() From left: Ankit Prasad, vice president, Norwest Venture Partners India, Shiv Chaudhary, managing director, and Nikhil Kookada, who is vice president

From left: Ankit Prasad, vice president, Norwest Venture Partners India, Shiv Chaudhary, managing director, and Nikhil Kookada, who is vice president

What about wrong bets? Shah claims that Norwest doesn’t have too many companies where the story went wrong. Quikr, though, happens to be one such muted bet. It had a great team, good founder, and a perfect market opportunity. An internal fraud in 2019 turned out be devastating. Though Norwest managed to get back its capital through secondary sale, the company decided to not exit in full. The strength of a VC, Shah reckons, is best judged by how they react during bad times. A fund always comes in with an equity risk. “And a part of equity risk is that some things will go wrong. You can’t do much," he says. What’s crucial, though, he underlines, is to have loads of empathy. “The startup ecosystem is blessed with critical thinking. But I think we need much more empathy," he says.

So is it easy being a VC? A venture capital world, Shah reckons, is a brutal industry. One has to keep performing day after day, and treat every deal as the last deal. The moment one starts cracking good deals, the threat of bringing the bar down becomes high. “At Norwest, we keep saying, ‘keep the bar high’," he says. The fund, he points out, has never exhibited haste and recklessness. “We are not spray and pray. We don’t have to do 20 deals a year," he says, adding that there have been years when the fund just managed to close two deals. “The bar has to be kept very high," he says, sharing his biggest learning. “The VC world is very hard to get in, but it’s very easy to get kicked out," he reckons. “The magic lies in dodging bullets."

So what’s the secret sauce? Shah explains. “You have to dodge a lot of bullets," he reckons. The first seven years of the fund’s operations in India, he underlines, was all about dodging as many bullets as possible. “We only did the deals which were so compelling that we could not say no," he says. “And that has really worked for us," he stresses, adding that the investment in Sriram City was his first deal with a cheque size of $28-30 million.

So what’s the secret sauce? Shah explains. “You have to dodge a lot of bullets," he reckons. The first seven years of the fund’s operations in India, he underlines, was all about dodging as many bullets as possible. “We only did the deals which were so compelling that we could not say no," he says. “And that has really worked for us," he stresses, adding that the investment in Sriram City was his first deal with a cheque size of $28-30 million.

When asked to select a single quality which sets Norwest apart in a cluttered VC space, the entrepreneur talks about the freedom that the fund brings in. “They will get involved only when you want them to," he says. What also clicked between Shah and the founder was the common belief in building a sustainable business. “After my Myntra and Medlife experience, I wanted to build a business for the long term," he says. “This resonated with Norwest. They are very thoughtful investors," he adds.

When asked to select a single quality which sets Norwest apart in a cluttered VC space, the entrepreneur talks about the freedom that the fund brings in. “They will get involved only when you want them to," he says. What also clicked between Shah and the founder was the common belief in building a sustainable business. “After my Myntra and Medlife experience, I wanted to build a business for the long term," he says. “This resonated with Norwest. They are very thoughtful investors," he adds.