RBI Governor Shaktikanta Das expects headline inflation to rise in the coming months due to supply disruptions, volatile food and energy prices, geopolitical tensions, and extreme weather conditions

Reserve Bank of India (RBI) governor Shaktikanta Das (C) arrives along with deputy governors to address a press conference in Mumbai on August 10, 2023. - India"s central bank again left interest rates unchanged on August 10 but warned that higher food prices, caused in part by extreme weather, had impacted household budgets and halted a downward inflation trend. Image: Indranil Mukherjee / AFP

Advertisement

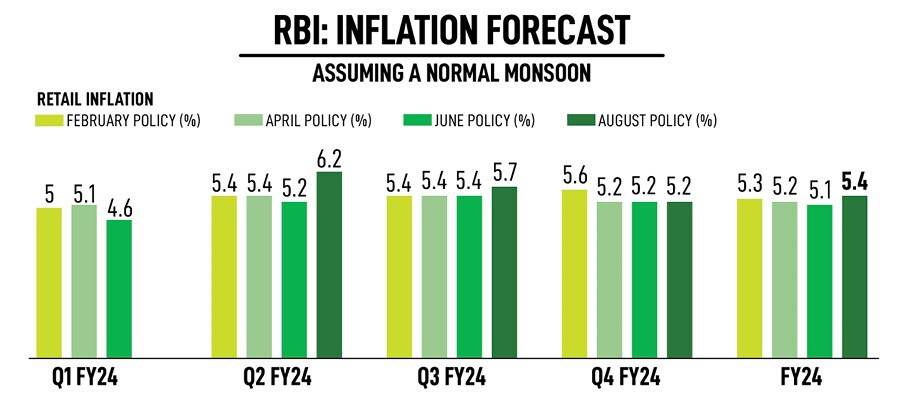

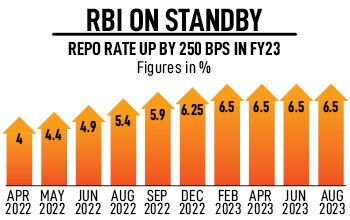

On Thursday, the six-member rate-setting panel decided unanimously to hold the benchmark repo rate at 6.5 percent. Excluding Jayanth Varma, all other members voted to remain focussed on withdrawal of accommodation to align inflation to the target of 4 percent while supporting durable growth in the economy. Importantly, the central bank raised its inflation outlook for the July-September quarter to 6.2 percent from 5.2 percent earlier (see table), signalling that the war against inflation is not over and interest rates may be higher-for-longer, and retained its growth estimate for FY24.

“We have made good progress in sustaining India’s growth momentum. While inflation has moderated, the job is still not done. We continuously assess the impact of our past actions, the evolving inflation dynamics and the implications of incoming data for the economic outlook. We do look through idiosyncratic shocks, but if such idiosyncrasies show signs of persistence, we have to act," RBI Governor Shaktikanta Das said as he unveiled the bi-monthly monetary policy.

Das cautioned that headline inflation is likely to witness a spike in the near-term on account of supply disruptions due to adverse weather conditions. “It is important to be vigilant about these shocks with a readiness to act appropriately so as to ensure that their effects on the general level of prices do not persist. There are risks from the impact of the skewed south-west monsoon so far, a possible El Nià±o event and upward pressures on global food prices due to geopolitical hostilities," he explained.

Retail inflation rose from 4.3 percent in May to 4.8 percent in June, and most economists predict CPI will breach RBI’s upper threshold of 6 percent in July. The pick-up in inflation is largely on account of higher prices of vegetables, eggs, meat, fish, cereals, pulses and spices. Overall, core inflation was stable in June. The central bank is worried that the spike in vegetable prices—led by tomatoes—will add upside pressures on the near-term trajectory of retail inflation.

However, RBI is hopeful that fresh market arrivals of fruits and vegetables will ease price pressures. The improvement in the progress of monsoon and kharif sowing could help to cool prices to some extent. Furthermore, the outlook for crude oil prices is unclear given the possibility of production cuts by some OPEC members.

Lakshmi Iyer, CEO-investment and strategy, Kotak Alternate AMC, says, “While status quo on rates wasn’t much of debate, the key thing to watch out for was the tone of the MPC [Monetary Policy Committee] guidance. Here, the RBI seems to sound cautious and ready to act as and when the situation warrants, but not as hawkish as the markets would have expected. It also suggests that much of the possible negative outcomes were already in bond prices."

On the growth front, the central bank was less worried in light of improvement in investment activity largely led by government capital expenditure, higher level of business optimism, and strong construction activity driven by growth in cement production and steel consumption. In the first quarter, capacity utilisation in the manufacturing sector stood at 76.3 percent against the long-term average of 73.7 percent.

“These underlying developments and the upcoming festival season are expected to provide support to private consumption and investment activity. The spillovers emanating from weak external demand and protracted geopolitical tensions, however, pose risks to the outlook," Das observed. Weak global demand and volatility in global financial markets, geopolitical tensions and geoeconomic fragmentation pose risks to the central bank’s GDP growth outlook for FY24 at 6.5 percent. The RBI did not revise its growth estimates and believes risks are evenly balanced.

Aurodeep Nandi, India economist, Nomura says, “The dilemmatic issue for the RBI in the run-up to the August policy meeting was that on the one hand, the sharp rise in vegetable and broader food prices has led to a sharp increase in the inflation outlook, which risks impacting the RBI’s inflation targeting credibility if it sounded too dovish. But on the other hand, the supply side nature of these shocks, and softening core inflation limits the need for monetary policy tightening in response. In the meeting, the RBI struck a fine balance between the two—by retaining policy interest rate and ‘withdrawal of accommodation’ stance and stating that it is ready to look through the inflation increase ‘for some time’, but also expressed the readiness to act in case inflationary pressures generalise."

ICRR: The surprise element

If the RBI’s decision to keep rates and policy stance unchanged for the third straight time was on expected lines, trust Governor Das to add an element of surprise. In an unexpected move, the central bank announced a temporary imposition of incremental cash reserve ratio (ICRR) of 10 percent on NDTL (net demand and time liabilities), for the period of May 19 to July 28, to absorb excess liquidity.

“Hiking the CRR would have had monetary policy connotations, so the temporary increase is aimed to be a non-disruptive way of dealing with the issue of excess liquidity in the system in the backdrop of the recent demonetisation of the Rs2,000 notes," Nandi adds.

Since the RBI announced its decision to withdraw Rs2,000 currency notes from circulation, as of July 31, about 88 percent or Rs3.14 lakh crore has been deposited in banks. Madhavi Arora, lead economist, Emkay Global, says the immediate impact of RBI absorbing liquidity via ICRR will be mild hardening of money market rates for borrowers, including NBFCs and corporates.

“For banks also there will be slight impact on their net interest margins (3-4 bps) depending on the instruments where they were parking the money—assuming 14.5 percent effective CRR. Overall, this would also lead to some interest loss for banks as banks were parking the short-term liquidity into STPL (short term personal loans) and money markets, instead of parking with RBI in variable reverse rate repo (VRRR) which also helped in some softening of CP/CD rates," Arora says.

Iyer points out that ICRR hike will suck out around Rs95,000 crore from the system. “This could dampen short-term bond yields in the near term. Bond prices could see relief buying as the mood was quite sombre assuming a very hawkish commentary." RBI stated the overall daily absorption under the liquidity adjustment facility (LAF) was Rs1.7 lakh crore in June and Rs1.8 lakh crore in July.

Pankaj Pathak, fund manager-fixed income, Quantum AMC, believes that despite the 10 percent ICRR, the banking system liquidity is likely to remain in surplus of more that Rs1 lakh crore for the next one or two months. “This should not have any durable impact on the bond yield curve though money market yields might inch up 10-15 basis points over the coming weeks. We expect the Indian bond yields to remain in the broader range of 7 percent to 7.3 percent over the coming months, tracking crude oil prices and the US treasury yields. Longer term outlook looks more favourable as the rate hiking cycle is nearing its end in most economies around the world and rate cutting cycle can start early next year," he says.

In June, India’s central bank followed the script and kept rates unchanged. The six-member rate-setting panel unanimously voted to hold the benchmark repo rate at 6.5 percent and five members voted to continue with the policy stance and focus on withdrawal of accommodation. RBI marginally lowered its inflation forecast to 5.1 percent from 5.2 percent, but kept its growth estimate unchanged at 6.5 percent for FY24. As last time, Das reiterated, “Let me re-emphasise that headline inflation still remains above the target and being within the tolerance band is not enough. Our goal is to achieve the target of 4 percent, going forward."

Iyer points out that ICRR hike will suck out around Rs95,000 crore from the system. “This could dampen short-term bond yields in the near term. Bond prices could see relief buying as the mood was quite sombre assuming a very hawkish commentary." RBI stated the overall daily absorption under the liquidity adjustment facility (LAF) was Rs1.7 lakh crore in June and Rs1.8 lakh crore in July.

Iyer points out that ICRR hike will suck out around Rs95,000 crore from the system. “This could dampen short-term bond yields in the near term. Bond prices could see relief buying as the mood was quite sombre assuming a very hawkish commentary." RBI stated the overall daily absorption under the liquidity adjustment facility (LAF) was Rs1.7 lakh crore in June and Rs1.8 lakh crore in July.