Sample this: A dealer of seeds and farm inputs or a tailor would run the business on the basis of informal records. Audited accounts don’t exist and neither do GST filings. At best, an income tax return would allow a loan officer to assess the income of the loan seeker.

Conventional wisdom reasoned that lending to this segment was inherently risky. Credit assessment was difficult, default rates were high and ticket sizes small. Add to that the challenge of setting up a large distribution network and most large banks reasoned it was not worth the effort.

But businesses like this number 64 million, and says Dhru, “This is huge whitespace waiting to be catered to." His travels across the country also taught him that borrowers were not habitual defaulters. Instead, it was an adverse event or the seasonality in their incomes that made them miss payments. Sure there would be some write-offs but he was confident a business that factored in a 2 to 2.5 percent default rate would be a viable one. If one could lend in exchange for a security the business had a chance of success. In 2017, Dhru had the chance to test his hypothesis.

Fast forward to 2024 and SBFC Finance is a listed entity worth ₹8,000 crore. The business which listed in August 2023 at ₹81, a premium of 44 percent to its IPO offer price of ₹54-57 per share. Since then, the stock has performed well on the bourses and traded at a market cap of ₹8,500-9,000 crore. And, in a sign of the quality of the business franchise, the market has placed a price-to-book multiple of 3 times.

![]() This has also been a time when investors are warming up to the idea that lending to small businesses is an investible proposition. The last decade saw the emergence of affordable housing finance companies with Aavas, Aptus and Home First building large franchises lending to borrowers outside the salaried class. They’ve managed to keep credit loss numbers in the 1 to 1.5 percent range and a return on equity of 14 to 17 percent.

This has also been a time when investors are warming up to the idea that lending to small businesses is an investible proposition. The last decade saw the emergence of affordable housing finance companies with Aavas, Aptus and Home First building large franchises lending to borrowers outside the salaried class. They’ve managed to keep credit loss numbers in the 1 to 1.5 percent range and a return on equity of 14 to 17 percent.

Now, the hope is that this could be repeated with small business lending as well. Lenders like SBFC Finance are tapping into a segment that didn’t have access to formal credit earlier. “These loans, which are usually made in smaller cities, are dependent on the agri business cycle and land rates," says Jindal Haria, co-founder, GreenEdge Wealth Service LLP. According to him, lenders are still skimming the segment and the true test will come once the market matures and they are forced to go down to less creditworthy borrowers.

On the other hand, proponents of the business argue that lending to small businesses has fundamentally changed as a trinity of GST returns, account aggregation and credit bureau records allow for lenders to make more robust credit assessment models. They point to Bajaj Finance and Cholamandalam Investment and Finance Company Limited, which have delivered return on equity of over 15 percent across the last decade over multiple cycles. This should be possible with small business lending in this decade they argue. The jury is still out on who is correct.

Setting Shop

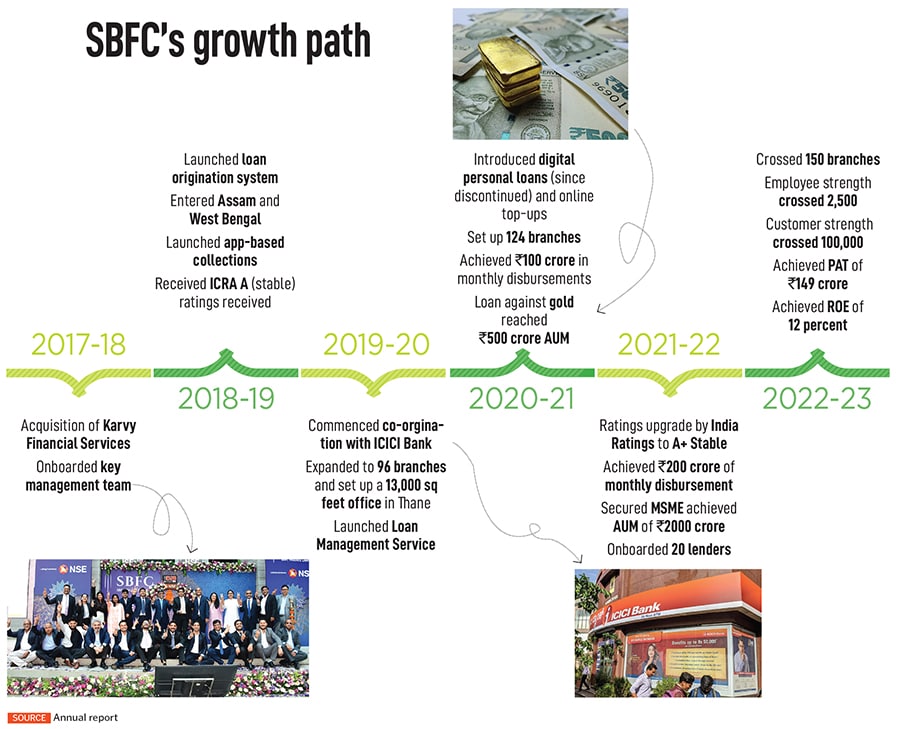

It was in 2017 that Dhru decided to set up a company dedicated to financing small entrepreneurs. He teamed up with Mahesh Dayani, who became chief business officer. The duo had worked together at HDFC Bank, and Dayani was with Kotak Mahindra Bank, lending to small businesses. They believed theirs was an idea whose time had come.

The first immediate challenge was to raise capital, which could be done either from private equity, corporates or family offices. At that point, they set themselves a target of $100 million in equity capital so that the business had a long growth runway. Family offices proved to be a non-starter as they weren’t able or willing to write out such large cheques. Private equity wasn’t able to provide access to long-term capital as their exits were dependent on the life of the fund. As Dhru elegantly puts it, “In a business where you take debt on rent, you don’t want to take equity on rent either."

SBFC’s main financier was to come in the form of the Clermont Group. Its chairman Richard Chandler had been an early investor in HDFC, HDFC Bank and IndusInd Bank. He wrote them their initial cheque of ₹750 crore and the business was capitalised. Clermont owns 58 percent of SBFC Finance. Another initial investor was Arpwood Capital.

![]()

SBFC defines its lending zone as borrowers with a loan ticket size of ₹5-30 lakh. This is a ₹2.5 lakh crore market, growing at 27 percent a year, according to Crisil. It is also 30 percent of the total market for MSME loans. These include small shop owners, restaurant owners, tailors, barbers who need money for business expansion. Their turnover is under ₹40 lakh, and they don’t file GST returns. SBFC chose this segment as loans under ₹5 lakh have a lot of competition from small finance banks and micro-finance institutions, and in the above-₹50 lakh segment banks play an active role.

Second, the company took the decision to lend only against a security. This is mainly in the form of property and they stay away from agricultural lands where enforcing the security could be problematic. For secured MSME loans, the loan-to-value ratio is 42 percent and for loans against gold, the loan to value ratio is 68 percent, leaving them with enough security against a fall in property or gold prices.

As its business has grown to 177 branches in 16 states, SBFC has honed its skills in verifying title deeds and has seen that enforcing its claim under the Debt Recovery Tribunals or SARFAESI Act is possible.

![]() SBFC’s borrowers include small shop owners, restaurant owners, tailors, barbers who need money for the expansion of their businessImage: Shutterstock

SBFC’s borrowers include small shop owners, restaurant owners, tailors, barbers who need money for the expansion of their businessImage: Shutterstock

Assessing risk

In doing their credit checks, SBFC believes that risk-based pricing works differently in India compared to the rest of the world. As one goes up the risk curve, borrowers are charged higher rates, but those rates don’t necessarily compensate for the probability of default, which can be adversely impacted due to a macro event. “The end use of money is a big determinant of the success or failure of the loan," says Dayani. “Whenever the lender doesn’t have control of the end use then the outcome is worse." As a result, in addition to taking property as security, the company has established a branch-led model where a loan officer can go and survey the business and make an assessment of its cash flows. Credit bureau scores, if available, allow them to access the past behaviour of the customer. One big change in the last three years is the increasing use of UPI payments by small businesses. This allows lenders to assess their cash flows. SBFC’s model also accounts for the fact that since these borrowers are not salaried employees, variations in income make it difficult for them to service their loans on a given due date.

In addition, the company has come up with a scoring system to assess loans with a ranking of 1 to 4. These track 200 variables: Is it a first generation business, is the property owned or leased, what is the age of the customer, is there an heir available, do their children work in the business, is it a manufacturing or trading business, what is the credit cycle, do they buy on credit and sell on cash, is there an inventory risk in the business. These questions allow them to reach a score, and this is then tracked real-time. For instance, if a customer has other loans running and has defaulted on them then the probability of default increases. With real-time monitoring, SBFC is able to get an idea of how the portfolio is likely to behave.

Dhru believes that as the data set increases, SBFC will become better at predicting the probability of default. This would happen at about the 50,00,000-customer mark. At present, the data set has 100,000 customers only, so it will take them time to get there.

This model has gotten SBFC to the ₹6,266 crore AUM mark in the quarter ended December 2023. The average yield on their portfolio is 16.8 percent and the spread (difference between yield and the cost of borrowing) 7.47 percent. In the last year, SBFC has seen an increase in its cost of funds from 8.53 percent to 9.4 percent. This is primarily on account of the rise in repo rates plus the increase in risk weights for banks lending to NBFCs. “With our rating upgraded, the cost of funds should be stable and we have recently borrowed through non-convertible debentures as well," says Narayan Barasia, chief financial officer.

![]()

Longer term success

Dhru and his team realise that businesses need to constantly innovate to stay ahead of the curve.

One such way is the collection business, where the company collects on loans. In India, loans are usually owned by the originators but with twhe advent of securitisation the originator of the loan may not necessarily be the same person whom the payments are due to. It was with the DHFL portfolio that was sold to banks—SBI, IndusInd—that SBFC saw a viable business opportunity. The next opportunity came with the Reliance Home Finance portfolio. This business, though small, represents an opportunity that can be scaled. The company does not break out revenue numbers for this part of its operations.

Another is co-lending and co-origination promoted by the RBI, whereby banks and NBFCs jointly make a loan. Here the loan can be made either simultaneously by banks and NBFCs or the NBFC can make the loan and the bank can take a part on their books within 30 days. This also gives the NBFC a robust steam of fee income as payment for the loan sourced for the banking partner.

The lending must be done 80:20, where banks take on 80 percent of the loan and NBFCs 20 percent. SBFC has tied up with ICICI and they have integrated their systems to make loans simultaneously. The loans made jointly by the two total ₹962 crore, or 18 percent of the ₹6,266 crore. Losses are also borne in proportion to the loan made by the bank and NBFC.

Third, is the risk of the business cycle and the macros turning bad. Haria who has studied these business models says the local economies of smaller cities depend on the agri value chain and real estate cycle significantly. It remains to be seen how the portfolio performs in the event of an adverse macro environment. Dhru agrees this is a fair point and the portfolio performance over a longer period (36 months or more) remains untested.

Also left unsaid is the industry view that the company has a key man risk. A fund manager who declined to be named said a fair amount of SBFC’s valuation is riding on Dhru and the team he has put together. Were he to leave it would be perceived negatively. At present Dhru has a 3.2 percent stake in SBFC, giving him skin in the game. Dhru, who has seen institutions built by Deepak Parekh and Aditya Puri, says he is in it for the long haul and it’s too early to rest on his initial laurels. “Our success or failure will only be determined a decade later," he says.

This has also been a time when investors are warming up to the idea that lending to small businesses is an investible proposition. The last decade saw the emergence of affordable housing finance companies with Aavas, Aptus and Home First building large franchises lending to borrowers outside the salaried class. They’ve managed to keep credit loss numbers in the 1 to 1.5 percent range and a return on equity of 14 to 17 percent.

This has also been a time when investors are warming up to the idea that lending to small businesses is an investible proposition. The last decade saw the emergence of affordable housing finance companies with Aavas, Aptus and Home First building large franchises lending to borrowers outside the salaried class. They’ve managed to keep credit loss numbers in the 1 to 1.5 percent range and a return on equity of 14 to 17 percent.