As of now, there are 98 countries that are in the process of exploring CBDCs, according to the Atlantic Council tracker. Of these, 11 countries have launched a CBDC, including the Bahamas, Eastern Caribbean islands and Jamaica. China, Russia, South Korea and Thailand have conducted pilots for their respective digital currencies, but are yet to officially launch them, while the people of Nigeria have rejected their country’s digital currency.

Given this scenario, the RBI is, in typical manner, taking calibrated steps to launch CBDCs. It is currently exploring the option to implement CBDCs in two forms: Account-based wholesale CBDC, and token-based retail CBDC. On November 8, the RBI will end its week-long first interbank pilot for the wholesale segment of the digital rupee (e₹-W), for settlement of secondary market transactions in government securities (G-Secs).

Trading volumes in the pilot project ranged between Rs 260 crore and Rs 530 crore daily between November 1 and 7 on the NDS-OM-CBDC platform, operated by the Clearing Corporation of India (CCIL), indicating that it has been well received. Other wholesale transactions, cross-border payments and a separate retail CBDC pilot will be launched shortly, the central bank has said.

Nine banks participated in the recent wholesale pilot, with the aim to reduce transaction costs and make transfer of money possible in real-time. The monthly billing from each bank to the CCIL is substantial, considering the normal transaction charge of Rs 200 on a Rs 5-10 crore transaction.

The wholesale CBDC pilot process required the banks to fund their wholesale CBDC e-rupee wallet, existing with the RBI. Once the bank decides to buy government bonds on the CCIL NDS-OM (negotiated deal system order matching CBDC) system, it selects the bonds it wants to buy at a particular price. If the counter party (another bank) likes the price requested, it puts in a counter offer to match the deal on the platform. One bank’s wallet gets debited by the particular amount and the G-Sec gets credited with the subsidiary general ledger (SGL) account of the other bank, almost in real-time.

![]()

Currently, all banks buy and sell bonds to and from the CCIL, which sends details of debits and credits to each bank daily and settlement is done the next day. “CBDCs’ biggest positive is that G-Secs get settled on T+0 and not the current T+1," says Amit Sureka, Yes Bank’s financial markets country head. Yes Bank is one of the nine banks—alongside State Bank of India, HDFC Bank, ICICI Bank, IDFC First Bank, HSBC India, Bank of Baroda, Kotak Mahindra Bank and Union Bank of India—identified for participation in the pilot project.

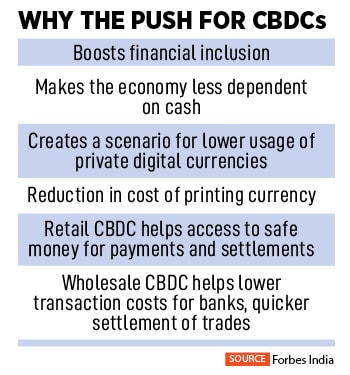

Aman Cheema, head of Global Real Time Payments and CBDC at Florida-based fintech FIS, says, “Many central banks are looking to address country-specific policy objectives, such as financial inclusion. Some central banks globally are also responding in part to the potential threat to monetary sovereignty arising from cryptocurrencies and stablecoins, while others with dwindling cash usage are looking to maintain public access to central bank money."

“CBDCs will be a major source of innovation and will have new payment and money features and functionalities, such as programmability. The larger aim is to bring the nation within the fold of the wider digital economy, and move cash into digital form," Cheema tells Forbes India.

Why RBI needs CBDCs

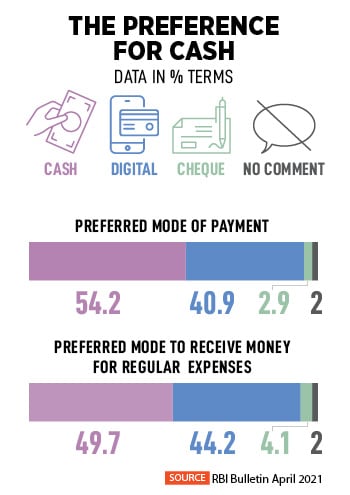

Over the past few years, India has been on an overdrive to go paperless (cashless), starting with the demonetisation move in 2016, which was followed by the introduction of the real-time payments system called Unified Payments Interface (UPI) in the same year. The contradiction in the current ecosystem, however, is that while digital transactions are gaining acceptance, cash has not lost its popularity in India.

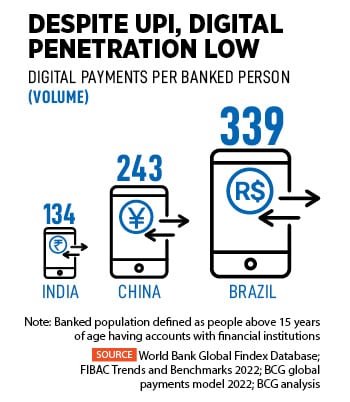

UPI processed 7.3 billion transactions worth Rs 12.11 lakh crore in October, a record high in terms of value of transactions. Transaction values have jumped 56.6 percent year-on-year while volumes have grown 73.3 percent in the same period.

![]()

But while digital transactions are on the rise, cash in the economy has also increased. “The growing use of electronic medium of payment has not yet resulted in a reduction in the demand for cash," said RBI’s fintech department in a CBDC concept note released in October.

India’s volume of bank notes in FY22 rose 4.95 percent to 13,053 crore from 12,436 crore a year earlier. Similarly the volume rose 7.2 percent in FY21 to 12,436 crore from 11, 597 crore a year earlier, according to the RBI’s 2022 annual report. Similarly the value of bank notes in FY22 rose 9.86 percent to Rs 31,057 crore from Rs 28,268 crore a year earlier in FY21, the value rose 16.7 percent to Rs 28,268 crore from Rs 24, 209 crore.

Cash management cost in also rising. The RBI says that the total expense incurred on security printing in FY22 was Rs 4,984.8 crore compared to Rs 4,012.1 crore in the previous year (July 1, 2020 to March 31, 2021).

Several central banks have also started getting worried about the growing usage of cryptocurrency stablecoins, which peg their value to an existing currency or asset. RBI officials have, in 2022, told a Parliamentary Committee of finance that cryptocurrencies can lead to “dollarisation" of a part of the economy, which could be against the country’s sovereign interest, according to a Press Trust of India report. The majority of cryptocurrencies are dollar-denominated and the initial trade could be in stablecoin USDT, which is bought to help purchase cryptocurrencies. Cryptocurrencies have the potential to become a medium of exchange, the officials have added. Income from cryptocurrencies is being taxed heavily in India, but its trading is yet to be regulated.

The RBI has expanded on the concerns surrounding cryptocurrencies in its October concept note, saying: “Central banks seek to meet the public’s need for digital currencies, manifested in the increasing use of private virtual currencies, and thereby avoid the more damaging consequences of such private currencies."

The note says that while cryptocurrencies are being hailed as “innovations that would usher in de-centralised finance and disrupt the traditional financial system", the “inherent design of cryptocurrencies is more geared to bypass the established and regulated intermediation and control arrangements that play a crucial role of ensuring integrity and stability of monetary and financial eco-system."

Bringing blockchain to banking

Blockchain startups, fintechs and cryptocurrency exchanges are not just appreciative of the RBI’s pilot, they are also confident that the central bank will explore types of blockchain technologies to achieve different functions and goals.

Although the wholesale CBDC pilot used the distributed ledger technology (DLT) type of blockchain, RBI has said it is “deliberating on the various aspects of technological choices available, which includes, suitability of tech architecture (DLT/centralised/hybrid open source/proprietary), security of the token creation process and central bank node, standards and protocols to be followed by each stakeholder."

FIS’s Cheema says, “At the moment, it is unclear whether it [RBI] will use DLT-based infrastructure or a centrally-controlled database. Although blockchain is one of the core technologies for CBDCs, the selection will be based on various factors such as India-specific policy objectives, sustainability and security."

FIS has created CBDC-connected ecosystems and virtual labs, in collaboration with M10 Networks’s digital money platforms, which allow central banks to carry out pilots, test rollout strategies and accelerate implementation of a live CBDC. The digital money platform can tokenise central bank money and commercial bank deposits in the form of CBDC and digital regulated money. Cheema adds that M10’s enterprise-grade DLT supports over 1 million transactions per second, at less than one second latency.

Pratik Gauri, co-founder and CEO of blockchain startup 5ire is “thrilled" with the RBI’s pilots for CBDCs. “Digital currencies are a good move for financial inclusion, a great step to bridge the gap between the digital and physical world, and they put India at the epicentre of a Web3 revolution," he tells Forbes India.

![]()

Gauri adds that the RBI move signals that India is ready to adopt blockchain. It is like putting banking on the blockchain, using technologies and ensuring regulation and security. Experts indicate that India’s government could announce more moves in the FY24 Union Budget.

Crypto exchange CoinSwitch’s CEO Ashish Singhal answers the often-posed question of whether CBDCs can coexist alongside the crypto ecosystem. “CBDCs are different from public cryptos. It is like stocks versus money both can and will coexist, as they solve different problems." Singhal says the biggest advantage of CBDCs will be “making things real-time", whether it is related to remittances or settlement of trades.

“As a user, money may seem real-time to us, but it is not actually real-time. That is where CBDC adds amazing value. It is the next step of any economy, to have real-time systems through blockchains," says Singhal.

Rival crypto exchange chief Sathvik Vishwanath, co-founder and CEO of Unocoin, says, “Money transfers from smartphones will be fast and hassle-free. Most importantly the digital rupee will help get rid of fake currency problems." Vishwanath is talking, in particular, about retail CBDC, which, when introduced, will provide easy access to safe money for settling transactions, as it is the direct liability of a central bank.

FIS’s Cheema says the benefits of adoption of the CBDC in the wholesale sector (CBDC-W) are significant and risks proportionately lower compared to the “more complex" area of retail CBDC (CBDC-R). Going forward, CBDC-R will complement—and not replace—existing payment structures. “An Indian CBDC should be able to utilise current payments infrastructure like UPI and digital wallets like Paytm and Google Pay," the RBI concept note says. It will also have to ensure interoperability between all these payment systems.

Bankers say the RBI has been the most serious participant in the entire ecosystem, getting banks up-to-date and providing technical, infrastructure, support and guidance, and has to be lauded for intent. The RBI is likely to experiment heavily in the retail space before launching this product. But if the bank wants to stay ahead of others in a rapidly evolving payments space, it will have to bite the bullet soon.