Credit growth from banks likely to pick up late FY26

Even as June-end data shows a decline in loan growth to its lowest level in three years, experts say concerns over unsecured retail lending and weak asset quality persist but an uptick can be expected

India’s banks across categories have in recent quarters seen the pressure of microfi nance hurt asset quality and quarterly margins.

Image: Shutterstock

Advertisement

Not all prudent actions translate into immediately positive results. After months of growing pressure to help pick up the pace of growth in India, the Reserve Bank of India (RBI), in 2025, started lowering interest rates—a reduction of 100 basis points in three policy meetings—to boost economic growth. It had kept rates on hold for two years prior to February to deal with stubbornly high inflation, which has now eased.

But some of the data emerging towards June-end indicates that loan growth has declined to 8.8 percent year-on-year (YoY)—its lowest level in three years (see data)—in the fortnight ended May 30. This has also been presented in RBI’s Financial Stability Report of June.

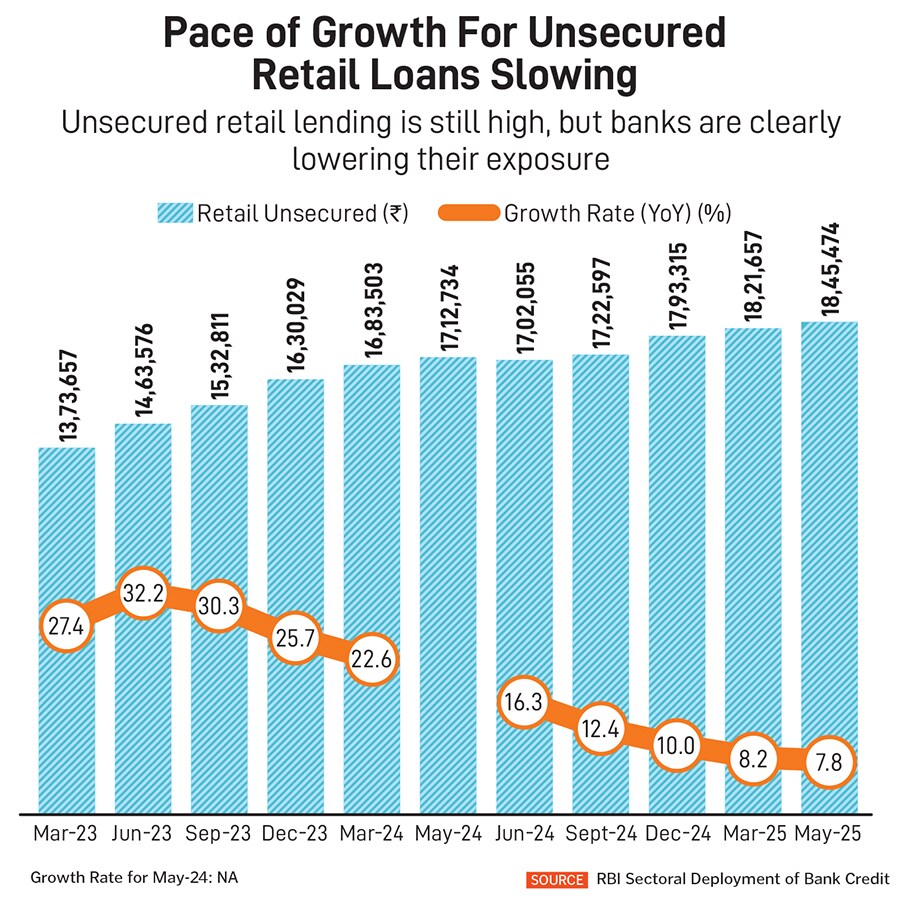

India’s banks across categories have in recent quarters seen the pressure of microfinance hurt asset quality and quarterly margins. The pressure of unsecured retail lending (which comprises credit cards, other personal loans and consumer durables) is being seen over the past three financial years. The growth rate of unsecured retail loans is now at 7.8 percent in May from a high of 32.2 percent in June 2023 (see chart).

All this means that we could see one of the most sluggish quarterly earnings growth for the April-June quarter, banking analysts say.

“Systemic credit growth slowed to around 9.6 percent as of June 13 amid demand moderation in the retail segment and a cautious growth strategy followed by banks in unsecured loans," says Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Securities, in a note to clients. They expect credit growth to sustain at 11.5 percent Y-o-Y in FY26, led by a recovery in the second half of FY26, he adds.

“1QFY26 would be the first quarter where the recent rate cuts start to hurt revenue growth," Kotak Institutional Equities said in a research note. Bank earnings are expected to decline 2 percent year-on-year in April-June, on the back of weak revenue growth.

“We have seen a lot of developments [from the RBI] which have provided impetus to credit growth but some of these have come in more recently. They will take some time to play out," Subha Sri Narayanan, director of Crisil Ratings, tells Forbes India. “Credit growth will be stronger in the second half than the first half," she adds. She estimates loan growth to be at 12 to 13 percent in FY26, from 11 percent last fiscal.

Narayanan says banks are a bit cautious to lend at this stage due to the risks to unsecured side of lending seen in non-banking financial companies (NBFCs), where there are concerns of asset quality.

But credit growth levels may not pick up to the levels we saw in the past growth had touched 16 percent for two consecutive years in FY23 and FY24. She says the ecosystem has now seen a clarification on project finance provisions which banks have to maintain. On June 19, the RBI told lenders to maintain 1 percent provision each on commercial real estate-residential housing (CRE-RH) and 1.25 percent provision on commercial real estate (CRE), during the construction phase.

In the earlier draft, the provision was proposed at 5 percent. Banks were earlier sitting on the fence, but now, with clarity emerging, there could be a pick-up in activity in 2HFY26.

Motilal’s Aggarwal also estimates that there could be a double-digit decline in net interest margin for all banks under their coverage in 1QFY26E.

On the credit-to-deposit levels, banks have started to reduce deposit rates for savings accounts and term deposits. But with deposit rates falling and the 100 bps CRR cut taking effect, liquidity will improve and help improve margins.

But net income for banks will see a muted growth at 1.7 percent YoY (down 0.6 percent QoQ). Profitability will remain largely flat for the quarter.

When the RBI continued to cut rates aggressively, the central bank said it was “imperative to continue to stimulate domestic private consumption and investment through policy levers to step up the growth momentum. This changed growth-inflation dynamic calls for not only continuing with the policy easing but also frontloading the rate cuts to support growth".