How Fibe built a profitable story in online lending

In 2015, Akshay Mehrotra and Ashish Goyal planned a heady brew with their 'cheaper than one beer' proposition. The VCs, however, didn't get intoxicated, and EarlySalary (rebranded as Fibe) had 127 rej

Akshay Mehrotra, co-founder and CEO, Fibe. Image: Madhu Kapparath

Advertisement

Jaipur, 2015.

The mavericks from Pune exuded thrilling vibes. And this is what the celebrated doctor-turned-investor in Jaipur was looking for. “I don’t understand the idea of your venture," confessed Dr Ashok Agarwal of the Transcorp Group who was fascinated by the glittering professional track record of the rookie founders. Akshay Mehrotra was a management grad and Ashish Goyal was a chartered accountant, and both were pitching for funding for their yet-to-be-launched online lending venture, which had an outrageous genesis and a disruptive proposition.

Sample this. “What if someone lends you money for seven days?" Mehrotra offered this interesting proposition to a battery of young executives who were compelled to lead a plain vanilla life towards the end of every month. “Salary almost khatam ho jaati hai month-end pe (salary gets exhausted towards the end of every month)," was their grouse, which Malhotra thought was a fabulous business opportunity. “Okay, tell me how much you would pay as interest?" he tried to find the sweet spot. “It should be cheaper than one beer," was the unanimous reply, which triggered the business idea: Take ₹20,000 for seven days and pay just ₹128. “Well, that was the price of a bottle of beer in Bengaluru," recalls Mehrotra. “That’s the price. Iske andar loan dena hoga (we will have to offer a loan within this range)," he decided and roped in his friend Goyal.

Back in Jaipur, the duo was making a maiden funding pitch. And technically, there was nothing that brewed in favour of the entrepreneurial newbies. Let’s start with age. The greenhorns were 34. A decade ago, the startup world warmly embraced the 20-something young ones. If age was a red flag, then the move to dabble into a venture that was outside their experience zone—lending and insurance were as distinct as apple and cheese—was a red herring for any potential investor.

Mehrotra and Goyal had their longest stint at Bajaj Allianz where they became friends, and both had close to 15 years of professional experience under their belt. Both, though, had one big plus. While Goyal had mastered risk, portfolio and debt, Mehrotra had an in-depth understanding of sales, products and consumers. When combined, the duo did possess a deadly combination which was tough for a funder to ignore.

Agarwal, though, found a different reason to back the new kids on the block. Mehrotra was the youngest CMO (chief marketing officer) at Bajaj Allianz and Big Bazaar. His friend, meanwhile, was the youngest CIO (chief investment officer) at Bajaj Allianz. “If you are quitting the best-paid marketing job, and your friend is leaving a profile that includes managing an $8 billion portfolio, then you guys will crack something for sure," reasoned Agarwal and cut a cheque of $1.5 million.

The funding information fanned out, EarlySalary launched operations with an early seed investor in 2015, but what grabbed the eyeballs was the news that a girl borrowed money to celebrate her dog’s birthday party. “That’s how it started, but we were quick to realise that lending is a serious business," he underlines.

The realisation was swift. Quite early in its innings, EarlySalary ran out of money. And if you thought that the funds were exhausted due to cash burn, then you are wrong. The business was brisk, the loan business to the salaried class picked up like hotcakes, and there was little money left for operations. The friends scrambled for funding, reached out to countless venture capitalists, and flaunted the business metrics: The bounce rate is 10 percent, and the net default is just 1 percent.

The VCs, though, were not impressed. “Nobody will fund you on this business model. Change it," recommended a set of VCs. Another group raised a different kind of red flag. “Don’t you think your target addressable market—only salaried—is too niche? Why don’t you add self-employed and students," they gave their two cents. There was another cohort of funders who were apprehensive about the idea of lending money over a mobile app. “Real-time loan on mobile is fraught with high risk," they cautioned, and pointed out another vexing issue. “Why are you losing money in a lending business?" they probed, alluding to the first four years of loss posted by EarlySalary. The dejected founders were rejected by 127 VCs, scouted for their knight in shining armour, and for somebody who could give them something more valuable than money: Mentorship. Also read: Paytm, BharatPe and the fintech turmoil: What"s the way ahead?

Hemant Jalan, the founder of Indigo Paints, was the answer. “He taught us two priceless things," recalls Mehrotra. The first was the founders must learn to say a firm ‘no’. “We still quickly shut any experiment that has the potential to go south," he says. The second learning became the core of the company. “Never lose a dollar," Jalan underlined. Lending business is not a business of equity.

“It’s a business of debt, and no debt investor should feel that you will lose his money. If you lose money, no one will ever give you money," he warned.

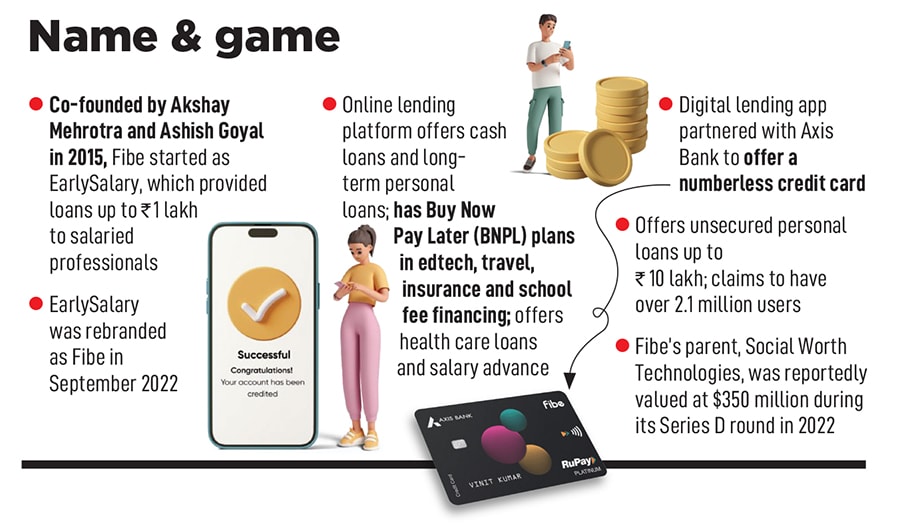

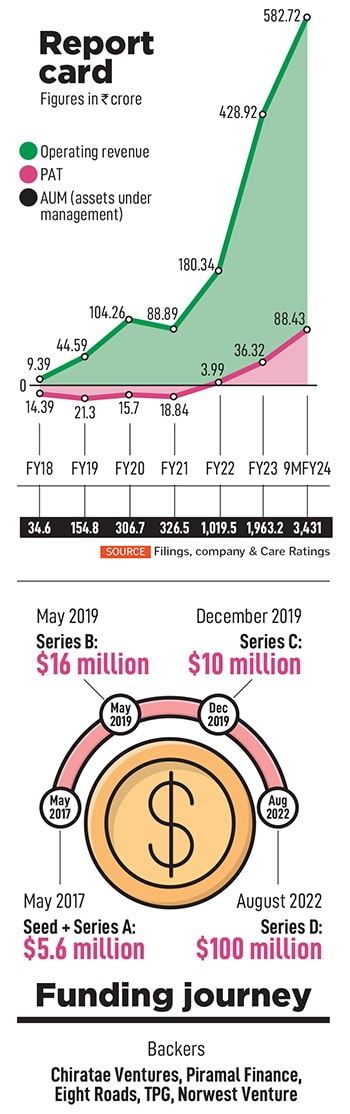

Fast forward to 2024. The founders are still in the business of lending, but they are not losing money. “We never lost any money except seed capital," claims Mehrotra, who counts Chiratae Ventures, Piramal Finance, Eight Roads, TPG and Norwest Venture among its backers, rebranded EarlySalary to Fibe in 2022, and the parent company—Social Worth Technologies—was reportedly valued at $350 million during its Series D round of funding in 2022. The online lending platform has grown at a brisk rate: From ₹9.39 crore in operating revenue in FY18 to ₹428.92 crore in FY23 (see box). What, however, is most gratifying for the founder is the profitable track record. Fibe has remained profitable for the last 12 quarters.

The backers know the value of betting on a profitable venture. “We believe that companies who adopt a customer-centric approach and who are focussed on building an institution are the ones always ahead of the industry peers," reckons Niren Shah, managing director and head of Norwest India. “Fibe has grown more than 20x since the time we first met them three years ago," he underlines, claiming that Fibe has one of the best asset quality performances in the segment, enjoys robust leverage and credit ratings, and the founders are focussed on governance, risk and compliance. What started as an ‘advance salary’ platform has morphed into a preferred destination for personal loans to young working professionals.

Despite an intoxicating growth, there are challenges that Fibe has to contend with. The biggest being a rising write-off rate. The write-offs stood at ₹44.46 crore during FY23 as against ₹15.48 crore during FY22, according to data accessed from Care Ratings. “This (write-offs) further increased to ₹94.17 crore during nine months of FY24," the report added, underlining that high write-offs remain inherent to all the entities operating in the unsecured lending segment. On a consolidated basis, credit costs as a percent of average AUM (asset under management) stood at 8.89 percent during FY23 as against 4.87 percent during FY22. “It continued to remain high at 8.43 percent during 9M FY24," the report highlighted.

Mehrotra, for his part, reckons that the default rate is nothing to lose sleep over. “Today 99.2 percent of people give back money," he claims, adding that the core of Fibe is made of repeat users. “Eighty percent of our money is given to repeat customers," he says. For repeat customers, he lets on, there is a predictability built into the system. “I have the highest repeat rate in the financial services industry in India," he claims, adding that there is a fine line between science and art.

“Lending is a science backed by art," he sums up his journey as a fintech entrepreneur.

The funding information fanned out, EarlySalary launched operations with an early seed investor in 2015, but what grabbed the eyeballs was the news that a girl borrowed money to celebrate her dog’s birthday party. “That’s how it started, but we were quick to realise that lending is a serious business," he underlines.

The funding information fanned out, EarlySalary launched operations with an early seed investor in 2015, but what grabbed the eyeballs was the news that a girl borrowed money to celebrate her dog’s birthday party. “That’s how it started, but we were quick to realise that lending is a serious business," he underlines.