Far from Ghaziabad, at the Mumbai headquarters of billionaire Sajjan Jindal’s JSW Energy, the top management had been working for months to launch its debut green bond issue in the overseas market. It hired Deutsche Bank late last year as the left-lead and structuring agent to raise money against its hydro power assets. After all, the investment bank had previously worked on six fund raising initiatives of JSW Group, and this time the stakes were higher as JSW Energy has been transitioning into a renewable energy company from being a traditional power generator.

On May 11, JSW Energy’s subsidiary JSW Hydro Energy Ltd (JSWHEL) raised $707 million by issuing US dollar-denominated green bonds in the overseas markets, due in 2031. The company managed to raise this capital by offering a coupon of 4.125 percent per annum and it is payable semi-annually. It is listed on the Singapore Exchange.

“For a debt trade like this, you have to get ratings from international rating agencies, and green certification for international ESG advisory entities. This was our first green bond trade, and that too a first hydro issue from Asia, so we had to educate people about hydro power generation assets," explains Pritesh Vinay, chief financial officer at JSW Energy. The bonds were issued by JSWHEL to repay the existing debt on its two operational hydro projects—the 1,000 MW Karcham Wangtoo on the Sutlej river, and the 300 MW Baspa 2 on the Baspa river, both in Himachal Pradesh.

“From 2013-14, when globally ESG issuances were around nearly $30 billion, it has now accelerated to nearly $500 billion by the end of 2020. Corporates are now far more conscious, and they are thinking about their business objectives through the lens of sustainability and are also tying themselves to specific goals," says Hardik Dalal, MD and head of loans and bonds at Barclays Bank India.

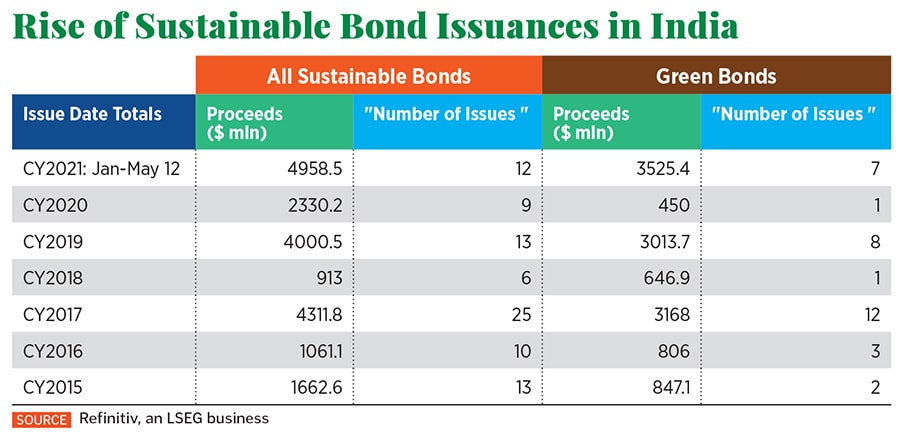

Issuing green bonds opens up a new pool of liquidity for a company’s funding requirements. Data from Refinitiv, a London Stock Exchange Group business that provides financial data, shows that between this January and May 12, a dozen companies in India issued sustainable bonds and raised $4.96 billion. Of these, seven were green bonds, one was a social bond, and another was a sustainability-linked bond. The companies include ReNew Power, Greenko, Hero Future Energies, Continuum Green Energy Pvt Ltd, Shriram Transport Finance, and UltraTech Cement Ltd. The amount raised in the last four-and-a-half months is double of what Indian companies had raised in the whole of 2020, or any year before that. In 2020, nine companies had collectively raised $2.33 billion by issuing sustainable bonds, especially green bonds.

“The market for sustainable investment banking activities took on growing prominence around the world in the first quarter of this year, accounting for a record 11 percent of global debt capital markets activity and setting all-time quarterly records for equity capital markets and syndicated lending," says Matthew Toole, director of deals intelligence at Refinitiv.

![]()

Globally sustainable finance bonds totalled $286.5 billion during Q1 2021, more than double the issuance levels in Q1 2020 and an all-time quarterly record. “European issuers accounted for the largest regional market for sustainable finance bonds, with 62 percent market share during Q1 2021, compared to 18 percent from the Americas and 15 percent from Asia-Pacific [$43.9 billion]," Toole adds.

With government policy focus on climate change, and sovereign states and corporates committing to sustainable development and net zero carbon goals, sustainable finance, especially in the form of bonds and loan financing, has witnessed a sharp growth over the last few years.

Sustainable bonds are a form of fixed-income instrument that is specifically tied to raising capital for climate and environmental related projects of a state or company. Since they are linked to the environment, these issuances, on a case to case basis, sometimes help them borrow at a cheaper rate compared to normal bonds. Sustainable financing includes green bonds, sustainability-linked bonds, social bonds, blue bonds, forest bonds, pandemic bonds, gender-diversity bonds, and transition bonds.

Sustainable bonds are usually classified in two categories: Use-of-proceeds bonds and sustainability-linked bonds or KPI-linked bonds.

“In a use of proceeds bond, the money is allocated for a specific purpose, which it identifies at the time of raising the capital like green investment (renewable projects/ green building etc), whereas the actual money can be used for paying off an existing debt (which was originally used for that eligible project), or construction of an eligible project," says Anjan Agarwal, executive director and head of debt capital market origination at JP Morgan India, who has managed multiple overseas sustainable issuances for Indian companies, including UltraTech Cement Ltd’s $400 million sustainability linked bond.

Agarwal explains, “In a sustainable target linked bond, the company does not have any restriction on how it uses the capital but during the bond’s tenure the company has to meet its sustainability-linked goal which it had committed to while issuing the bond, else they face a penalty on the same.

For example, UltraTech, under its sustainability performance target, aims to reduce 22.2 percent of carbon emissions for every tonne of cementitious material it produces by March 31, 2030, from the levels of March 2017. The company listed its bond on the Singapore Exchange and it was oversubscribed more than seven times. If UltraTech misses its target, the coupon will increase by 75 basis points in the penultimate year. The company did not respond to queries from Forbes India.

In another first from India, this January, Shriram Transport Finance (STF) raised $500 million at a coupon rate of 4.4 percent via social bonds. Sustainalytics, which conducts ESG and corporate governance research, deemed the social framework as credible under the social bond principles of 2018. The underlying story for STF’s social bond was driven by its positive social impact through improved financial access for MSMEs that are unable to access conventional financial services.

“We have seen quite a few debut issuers from India in the first quarter. Historically, a lot of renewable companies have tapped the green bond market and have done repeat issuances over the last five years," says Sajal Kishore, head of Asia-Pacific infrastructure and project finance at Fitch Ratings. “Barring one, the rest are five to 10-year issuances and typically rated in the BB category. Post-pandemic, we have seen stronger demand for green bonds."

The fund-raises have been skewed towards larger renewable energy companies like Azure Power, Greenko, ReNew Power and Adani Green Energy. But in this round of capital raise, a number of new issuers are identifying ways of securing a portion of the capital through greener ways. Companies are ring-fencing assets for this purpose.

One of the reasons behind Indian companies raising capital through sustainable bonds is this route allows them to raise capital at a fixed rate as against a loan which has a floating rate. In most cases, companies raised capital in the range of 4 to 4.8 percent, for a tenure of five to 10 years.

“On the bond versus loan debate companies have a whole host of factors to deliberate on: Existing cash flow, duration of bond versus completion of project, market conditions, rates, hedging costs," says Amrish Baliga, managing director and head of financing at Deutsche Bank India. Baliga’s team has led over nine bonds since the start of this year and has raised over $5 billion for clients.

Baliga explains that a simpler approach could be that the bond market offers an alternate source of liquidity that can be tapped into when requirements arise. “Redemptions could be structured to back-end cash flow allowing for equity release. It is not the 100-150 basis points arbitrage alone that goes into this thinking. The raising of bonds could positively affect a client’s stock price as well," he adds.

On the other hand, bond investors are looking for papers that are backed by ready operational projects, rather than those under construction. Usually, Indian companies raise debt from domestic banks to finance their project construction costs. These rates are charged as ‘marginal cost of funds based lending rate’ (MCLR), plus a spread structure.

[qt]Corporates are now thinking of their business objectives through the sustainability lens."

Hardik Dalal, MD and Head of loans and bonds, Barclays Bank India[/qt]

For example, in the case of JSWHEL, the asset has debt of ₹5,200 crore with an interest cost of 8.3 percent (overall JSW Energy debt cost is separate). JSWHEL plans to repay its debt of the operational hydro power generation assets and then raise fresh capital for projects under construction. It is setting up 2,600 MW of hybrid wind and solar capacity over the next three years.

While bankers are creating different payment structures, Kishore explains that there have been very few transactions where bonds were directly raised by the Indian entity. Usually the bonds have been raised by a foreign subsidiary under a two-tiered structure. The rated transactions have had a number of structural features and protections. In some transactions, a mandatory cash sweep takes place which helps in reducing the refinancing risk and in others there is a component of partial amortization woven in the structure to help mitigate the refinance risk.

“The market is evolving very fast on both the demand and supply side. Increased asset under management (AUM) dedicated to ESG is evident from over subscription that was received on all ESG labelled issuances from India," says Dalal. He adds that one cannot ignore that companies will get better pricing and execution. During this calendar year alone, Barclays has participated in seven transactions and raised $3.8 billion for Indian clients from international debt capital markets.

Agarwal of JP Morgan agrees and says that 12-15 months back, ESG investors would form single digit percentage points of an issuance but now it’s not uncommon for 30-40 percent contribution from ESG investment pool. “They are very sticky investors that has resulted in price tightening. Companies are thinking if there is a pricing benefit while they are being environmentally and socially responsible, then why shouldn’t we look at it?," he explains.

Global investment banks like JPMorgan Chase, Deutsche Bank, Morgan Stanley, Wells Fargo and Barclays have committed to net zero emission goals by 2050, and have committed to align their financing in all sectors to the goals of the 2016 Paris Agreement. They are creating sliced structures, which help commit to their goals.

Baliga says the pipeline for deals for this year is very strong, and so does Moody’s, as it expects a record $650 billion in global sustainable bond issuances in 2021.