Buyback Math: Why Larsen & Toubro is returning cash to shareholders

The company has become a business that doesn't require too much cash to execute its core infrastructure projects. However, though it makes sense for the company, shareholders who stick it out (and don

L&T"s market cap hit an all-time high of Rs 3,73,000 crore. Image: Sankhadeep Banerjee/NurPhoto via Getty Images

Advertisement

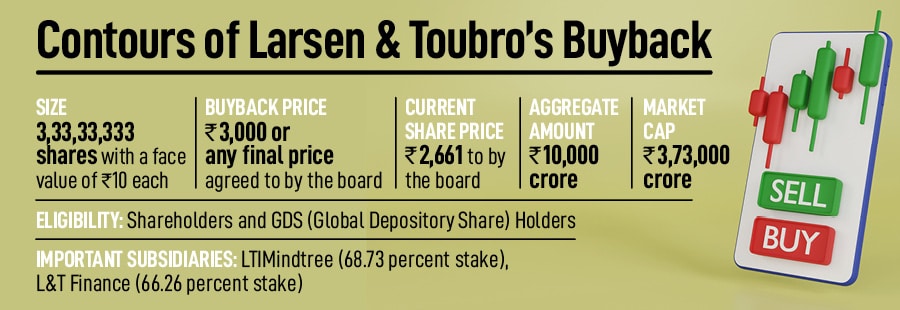

On 20 July shareholders of Larsen & Toubro (L&T) were in for a pleasant surprise. Four years after an abortive attempt at buying back its shares the company announced plans for another round. The market cheered and the company’s market cap hit an all-time high of Rs 3,73,000 crore.

The company plans to return Rs 10,000 crore to shareholders through the buyback of 3,33,33,333 shares at a price of Rs 3,000 or the final price agreed to by the board. The move will extinguish 2.3 percent of the share capital of the company. This is the first time the company has announced a buyback after its Rs 9,000 crore buyback attempt in 2019 failed on account of not being approved by SEBI as the company’s debt would be more than twice the net worth.

On the face of it the decision to buy back is a curious one. After all the company had been amply rewarding shareholders with rising sales and profitability, falling debt and a higher return on equity. And investors have taken notice. After spending a decade with a 4 percent annual return from its high hit in November 2007 the stock has been on a tear. The stock has since then returned 14 percent a year to shareholders between 2017 and 2023.

At the same time its financial metrics have improved. Inventory days are down to 41 days in March 2023 from 60 days in March 2012. Days payable (the number of days it takes to pay creditors) have climbed to 302 days from 244 days. This paints the profile of a company that is able to get suppliers to wait for payments and reduce capital blocked in inventory.

The buyback also comes at a time when infrastructure spends have been rising. In the Union Budget presented in February 2023 the government for the first time laid out a Rs 10,00,000 crore infrastructure spending target. L&T, with a portfolio that straddles civil engineering, hydrocarbons, urban transport systems, power plants and defence, is well positioned to benefit. Sales are up 9 percent a year in the last five years to Rs 1,83,341 crore in the year ended March 2023. Why then return cash to shareholders instead of deploying it?

The answer lies in the changing complexion of both L&T as well as the infrastructure business. On the infrastructure front there has been tremendous bidding discipline for projects. Take for instance the plan to minimise its exposure to Hyderabad Metro or the plan to exit its road assets announced in June 2022. The company has made it clear that it will bid for projects only where it sees a minimum return.

At the same time there has been a clear path to the payment of dues announced by both the central and state governments. This means that milestone-based payments are now available for infrastructure companies and delays on account of litigation are a thing of the past. “While there is a lot of stress in executing projects it is not a very capital-intensive business," said Shankar Raman, chief financial officer, L&T, in an interview to CNBC TV18. "While we have healthy profits and dividends whenever surpluses are higher money is best given back to shareholders."

“Separately there has also been a change in the texture of L&T as a company," says Amit Khurana, head of equities at Dolan Capital. “It is now also about LTIMindtree and L&T Financial Services both of whose numbers are consolidated into the company." To get a sense of the cash the subsidiaries bring in sample this. In the first quarter of FY24 the company made a profit of Rs 1,792 on a standalone basis but then LTIMindtree and L&T Finance numbers were consolidated the amount rose to Rs 3,095 crore. As a result, L&T has become a business that doesn’t require too much cash to execute its core infrastructure projects as well as one that needs to return cash to shareholders in order to ensure that its return on equity remains elevated. The company has set a 15 percent return on equity target for FY26.

While dividends are one route of rewarding shareholders buybacks are more efficient as shareholders need to only pay capital gains tax as opposed to tax at their marginal rate when cash is returned through dividends.

For shareholders the Larsen buyback brings to fore an important decision they would have to make. Would it be wise to tender now or would it best to wait for share price gains over the next few years? A similar story played out in the case of Hindustan Unilever’s 2013 buyback. Global parent Unilever had put down $5.4 billion dollars at a price that was 20 percent more than the prevailing share price. Shareholders who tendered made a quick 20 percent gain. The logic was that in India there are businesses that would grow faster than HUL.

What investors who tendered their shares failed to realise was that the earnings multiple of HUL would go on increasing. So while sales and profit growth chugged along at 11-14 percent as the multiple expanded the share price delivered gains of 15 percent plus.

A similar story could well play out at L&T. After a decade of low growth, infrastructure companies are becoming investable again. Take for instance IRB Infra that saw profits double to Rs 720 crore and its share price rise 20 percent in the last year. This is primarily due to bidding discipline.

At L&T the company is equally a play on India’s infrastructure cycle as it is on their holding at LTIMindtree and L&T Finance. As Raman clarified, a lot of the debt on their books is on account of L&T Finance whose numbers are also consolidated. Shareholders tendering now would get a quick 17 percent appreciation (the company would get 2.6 percent based on current earnings per share of Rs 80) but those not tendering would end up with a larger pie of the business and there may be a lot more to play for in the years to come.