Financial inclusion: How the India Mortgage Guarantee Corporation ensures low-ri

Mortgage guarantees ensure risk of lending to certain consumers is reduced, promise to make home loans more accessible

Last Updated: Feb 10, 2023, 14:54 IST5 min

Sample this: Two borrowers with similar age, income profiles and credit scores put in an application for a home loan. One is granted a loan with a 20-year tenure and at an 8.25 percent interest–the same rate the bank offers to customers with a high credit score. The second is sanctioned a lower amount and at a higher rate. He’s also made to provide further documentary evidence of his creditworthiness. Simply put, the bank is wary of the loan going bad.

This is a situation faced regularly by borrowers without a regular salaried income. Banks and other mortgage finance institutions find it hard to assess their repayment capability and err on the side of caution. Such customers are at a disadvantage and find themselves shut out of the market for home loans. They end up going to institutions that charge higher interest rates to take on the additional credit risk. Those in the informal economy–vegetable vendors, truck drivers, daily wage labourers–find it hard to get any mortgage finance at all.

Globally mortgage guarantees provide a workaround to this problem. This concept has begun to gain traction in India as well through the India Mortgage Guarantee Corporation (IMGC), which works with banks and mortgage finance companies to ensure that the risk of lending to certain consumers is reduced. “We are designed to be an independent third-party shock absorber," says Mahesh Misra, chief executive officer at IMGC.

Over the last decade IMGC has guaranteed Rs15,400 crore worth of home loans benefitting 85,200 borrowers. It now expects the scale of its operations to grow rapidly and plans to guarantee Rs10,000 crore worth of loans in the next financial year. The company counts among its shareholders the National Housing Bank, Genworth and Sagen. The business is making an operating profit but accounting rules require it to amortize revenues over the life of the loan and so it is not yet making cash profits.

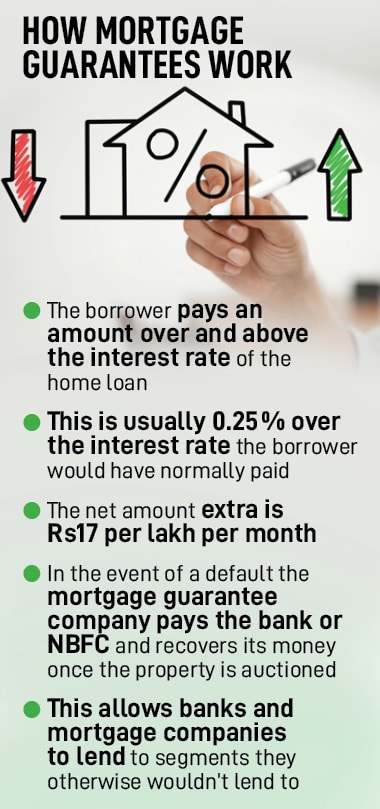

Here’s how it works. When applying for a mortgage loan a borrower who may not be in a bucket that a bank or non-banking finance company lends to is told of an option whereby for a small fee he can get either a higher loan amount or a longer tenure.

The fee typically works out to a 0.25 percent addition to the interest rate the borrower would pay. So, if the loan were to be offered at say 8.5 percent to a normal customer, for 8.75 percent this borrower could get the loan. The extra payment amounts to Rs17 per month on every Rs1 lakh borrowed. On its part IMGC receives 1.3 percent of the loan amount upfront as its fee for providing the guarantee.

The fee typically works out to a 0.25 percent addition to the interest rate the borrower would pay. So, if the loan were to be offered at say 8.5 percent to a normal customer, for 8.75 percent this borrower could get the loan. The extra payment amounts to Rs17 per month on every Rs1 lakh borrowed. On its part IMGC receives 1.3 percent of the loan amount upfront as its fee for providing the guarantee.

In the absence of this the borrower would have to either go to a lending institution that would offer a higher rate or have to accept a lower loan amount. In some markets like Canada mortgage guarantees are a compulsory product while in others like USA loans with a loan to value ratio in excess of 80 percent have to be accompanied with a mortgage guarantee. “We look at this as a social product that puts people in homes," says Stuart Take, director, IMGC.

In India once the loan goes bad i.e. no payment is made for 90 days the guarantee kicks in and IMGC makes its share of the payout. Banks on their part must continue to chase the borrower for the money before deciding if the property is to be foreclosed upon. Once the property is sold through the SARFESI or Securitization and Reconstruction of Financial Assets and Enforcement of Security Act the mortgage guarantee company is paid back its share.

In order to protect against the moral hazard of banks adopting lax underwriting practices IMGC and the bank must agree on a minimum sale price beforehand. Also, IMGC guarantees two years’ worth of the loan amount. “That is enough time for the lender to enforce their claim through SARFESI," says Misra.

But perhaps the most important function IMGC exercises is in assisting during the underwriting process. Banks and financial institutions have found it hard to develop the right credit metrics for new to credit customers as well as those without a regular income stream. Developing these models can take years and even then they are always prone to statistical errors.

IMGC is now working on developing its own credit score based on data from the dozens of lenders they work with. For instance, if a vegetable seller in Surat says he earns Rs9,000 a month then IMGC can check its database for such cases and see if the amount sounds correct. These underwriting capabilities take banks years to develop. Gruh Finance was a pioneer in this space and developed its own underwriting models. Sudhin Choksey, its former managing director, says, “We saw the mortgage guarantee as a good product but one that would be an unnecessary expense for our customers. We decided against offering it." (Gruh is part of Bandhan Bank). But for other banks that want to grow their books faster the mortgage guarantee provides a safe route. Misra plans to roll out an IMGC credit score about two years from now.

For now, IMGC has paid out 1,500 claims out of the 80,000 loans guaranteed and saw a spike in claims during the Covid outbreak. “Everyone (lending institutions) wants their loan book to look a certain way and now they can clearly see how it works for them," says Misra. Expect few more mortgage guarantee companies to set shop in India over the next few years.

First Published: Feb 10, 2023, 14:54

Subscribe Now