Now the National Payments Corporation of India (NPCI), which developed the payment system Unified Payments Interface (UPI), on October 22 has allowed One97 Communications to onboard new UPI users on their Paytm app.

Paytm has in recent months been trying to transition its core payments business from its subsidiary bank Paytm Payments India Ltd (PPBL) to four other banks (Axis Bank, HDFC Bank, SBI and Yes Bank) after regulatory action prevented PPBL from onboarding new UPI users.

The regulator Reserve Bank of India, this February, accused the company of persistent non-compliances and continued material supervisory concerns in the bank, warranting further supervisory action.

Citi analyst Vijit Jain says Paytm’s main focus going forward will be “on revitalising/recovering market share in consumer UPI payments and introducing new cross-sell opportunities into the UPI consumer Monthly Transacting Users (MTUs)."

A Paytm spokesperson said, “We see a tremendous opportunity on the consumer side with UPI and are dedicated to bringing the best in innovation for users."

With this latest development, users will be able to create new UPI IDs on the Paytm app by linking their bank account to the Paytm app for payments. Paytm will continue to offer this in partnership with leading banks, including SBI, HDFC Bank, Axis Bank and Yes Bank.

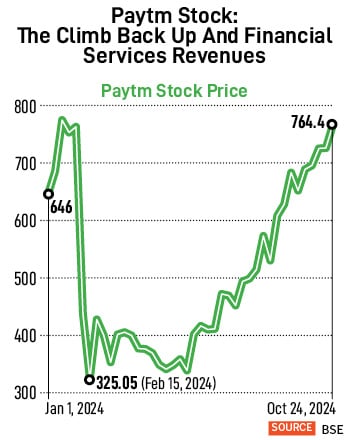

The Paytm stock price has now risen 122.7 percent to Rs 724 at the BSE on Friday, October 25, from a low of Rs 325.05 just after the regulatory action.

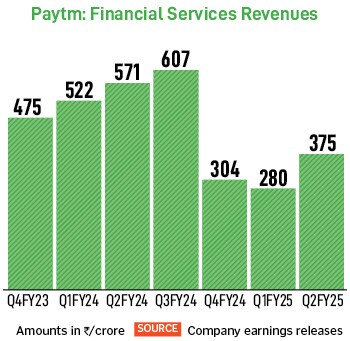

Revenues steady, betting big on DLG programme

In the September-ended quarter, the company reported an 11 percent quarter-on-quarter jump in revenues to Rs 1,660 crore, due to a 5 percent rise in gross merchandise value (GMV) at Rs 4.5 lakh crore, better realisation from devices and a 34 percent sequential quarterly increase in revenues from financial services.

![]() The company also turned profitable on a consolidated basis for the first time since listing, with a profit after tax of Rs 930 crore, but only due to a one-time exceptional gain of Rs 1,345 crore, on account of sale of entertainment ticketing business to Zomato. If this were adjusted for, the net loss stood at Rs 420 crore. In the first half of FY25, the company has posted a net loss of Rs 1,250 crore. Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Financial Services forecasts the loss to improve 43 percent year-on-year and reduce to Rs 440 crore in 2HFY25.

The company also turned profitable on a consolidated basis for the first time since listing, with a profit after tax of Rs 930 crore, but only due to a one-time exceptional gain of Rs 1,345 crore, on account of sale of entertainment ticketing business to Zomato. If this were adjusted for, the net loss stood at Rs 420 crore. In the first half of FY25, the company has posted a net loss of Rs 1,250 crore. Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Financial Services forecasts the loss to improve 43 percent year-on-year and reduce to Rs 440 crore in 2HFY25.

Citi’s Jain values Paytm at a 42x September 2026E EV/Adj Ebitda, where the multiple is over 100 percent premium to other global fintech companies. Jain assesses that Paytm’s growth and margins have a “significant upside potential" beyond FY26E.

Paytm’s founder Vijay Shekhar Sharma is betting big on the company’s default loss guarantee (DLG), also known as the first loss default guarantee (FLDG) programme to boost growth in coming quarters. The DLG model will mean Paytm guaranteeing a portion of the loans it facilitates for its lending partner in their portfolio, which analysts say will help to mitigate risks and increase the volumes of loans issued.

Paytm has already signed an agreement with SMFG India Credit, for a DLG of Rs 225 crore. “The DLG model will help to increase disbursements with the existing partners and expand partnership with new lenders for the loan distribution," a Paytm spokesperson said.

![]() In the Q2FY25 earnings call with analysts on October 22, 2024, the Paytm top management disclosed that previously the company operated at take rates between 4.5 percent and 5 percent without factoring in the DLG. Put simply, a take rate is how much money a business makes from a transaction.

In the Q2FY25 earnings call with analysts on October 22, 2024, the Paytm top management disclosed that previously the company operated at take rates between 4.5 percent and 5 percent without factoring in the DLG. Put simply, a take rate is how much money a business makes from a transaction.

Currently, DLG expenses are accounted for, and overall take rates over the life of a loan are above 5 percent, the Paytm management said in the earnings call. The overall take rate is expected to exceed 5 percent, resulting in substantial revenue.

Motilal Oswal’s Aggarwal says that “disbursements are likely to witness a healthy increase over the next few years", for Paytm. Aggarwal estimates Paytm to turn Ebitda positive by FY27 but keeps a ‘neutral’ rating for the stock, saying that estimates and ratings will be reviewed “after getting more clarity on recovery in business volumes and growth in MTUs" after the NPCI approval.

Citi’s Jain, while upgrading One97 Communications to a ‘buy’ investment call, agreed that Paytm could see an “acceleration in merchant loan disbursals post launch of [more] DLG offers to lending partners."

The unclear scenario

While Paytm’s Sharma has publicly been stating that it will be business as usual now, the business future and viability of Paytm goes beyond its quarterly financial performance.

Paytm will obviously continue to onboard more merchants and seek to cross-sell financial solutions more aggressively, but if this business model works, it could bring into contention the broader question of Paytm being acquired by a bank or a non-banking financial company (NBFC). A bank would be better placed to sell curated products and credit to the Paytm customer.

If that be the case, Sharma would be better placed to fetch a better valuation for Paytm, once it sustains growth and profitability, possibly by FY27.

The company also turned profitable on a consolidated basis for the first time since listing, with a profit after tax of Rs 930 crore, but only due to a one-time exceptional gain of Rs 1,345 crore, on account of sale of entertainment ticketing business to Zomato. If this were adjusted for, the net loss stood at Rs 420 crore. In the first half of FY25, the company has posted a net loss of Rs 1,250 crore. Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Financial Services forecasts the loss to improve 43 percent year-on-year and reduce to Rs 440 crore in 2HFY25.

The company also turned profitable on a consolidated basis for the first time since listing, with a profit after tax of Rs 930 crore, but only due to a one-time exceptional gain of Rs 1,345 crore, on account of sale of entertainment ticketing business to Zomato. If this were adjusted for, the net loss stood at Rs 420 crore. In the first half of FY25, the company has posted a net loss of Rs 1,250 crore. Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Financial Services forecasts the loss to improve 43 percent year-on-year and reduce to Rs 440 crore in 2HFY25. In the Q2FY25 earnings call with analysts on October 22, 2024, the Paytm top management disclosed that previously the company operated at take rates between 4.5 percent and 5 percent without factoring in the DLG. Put simply, a take rate is how much money a business makes from a transaction.

In the Q2FY25 earnings call with analysts on October 22, 2024, the Paytm top management disclosed that previously the company operated at take rates between 4.5 percent and 5 percent without factoring in the DLG. Put simply, a take rate is how much money a business makes from a transaction.