Penalty on non-payment of crypto TDS: What does it mean for retail investors?

At a time when trading volumes have dropped considerably, experts say the new tax amendments on virtual digital assets will further confine the growth of the industry and lead to more investors switch

A 30 percent tax plus applicable surcharge and four percent cess was announced to be levied on profits made from crypto trading last year.

Image: Shutterstock

Advertisement

Last year during the Budget speech, Finance Minister Nirmala Sitharaman introduced crypto taxation for the first time by bringing private cryptocurrencies under virtual digital assets (VDAs). This year, however, there was no mention about crypto during the Budget speech on February 1. But some new developments were later discovered in the fine print, which indicated a change in tax deducted at source (TDS) rules that affects VDAs.

A 30 percent tax plus applicable surcharge and four percent cess was announced to be levied on profits made from crypto trading last year. Also, losses made on any particular cryptocurrencies cannot be offset against profits made on other cryptocurrencies, and one percent TDS under section 194S of the Income Tax Act was levied on crypto transactions above Rs10,000.

This year, the Finance Bill mentioned an amendment in the Income Tax Act under section 271C, which will also penalise non-payment of TDS on virtual digital assets. This would include a penalty amount equal to the unpaid TDS, which will be imposed by a joint commissioner, or a jail term for up to six months. In case of a delay in payment, this could amount to an interest rate of 15 percent per annum for late payment.

TDS is a direct tax collection mechanism in India. The Indian Income Tax Act, 1961 requires that a particular proportion of tax be deducted by the payer when making certain payments to the receiver. Tax is required to be deducted from payments such as commission, interest, salary, royalties, contract payment, brokerage, and so on. The tax deducted must be remitted with the tax authority on behalf of the receiver by the payer. In the event that a payer fails to deduct and remit the tax at source to the government, a penalty may be levied u/s 271C of the Income tax act, explains Rishabh Parakh, chartered accountant and founder of NRP Capitals.

For instance, if the investor fails to deduct Rs1 lakh as TDS from a certain transaction, or even after deducting, failed to pay to the government, there would be a penalty equal to an amount up to Rs 1 lakh, or the same amount that was not deducted or paid to the government. A jail sentence may also be imposed in specific circumstances, in addition to the interest that will be charged for the late payment.

Additionally, Section 194S states that the buyer is responsible for filing TDS if a transaction is made via peer-to-peer (P2P) crypto-to-crypto exchange rather than an exchange. “The exchanges handle TDS computation and filing on behalf of their customers when you trade on them. So, all the crypto investor needs to be careful in dealing with the TDS provisions, failure to do that can land them in jail. Because of this, one must exercise caution when investing in an asset class that is so volatile and, on top of that, has certain tax regulations that must be followed. As a result, one should exercise caution not only when investing their money but also with regard to the tax compliances," says Parakh.

TDS penalties can be imposed if an investor does not deduct TDS when he is liable to deduct the same. Earlier, the TDS on crypto-to-crypto trades was not adequately covered by the penalty provisions of Section 271C and 276B. The Budget has proposed to plug this loophole, explains Punit Agarwal, founder KoinX, a cryptocurrency taxation platform. “There has been a fear in the community since this amendment in the Budget. Investors might shift to compliant exchanges. It may also have the impact of investors leaving this asset class altogether."

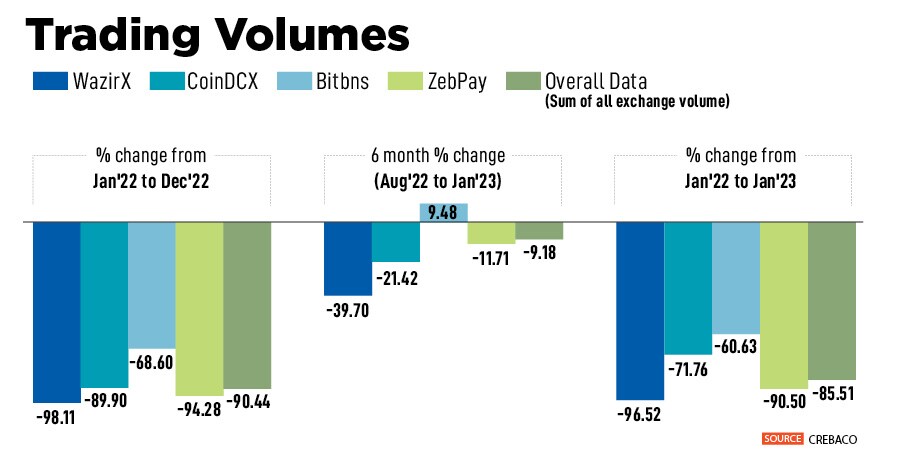

After the introduction of tax in 2022, India saw a sharp decline in crypto transactions. According to news reports, there was a shift of cumulative trade volume of around Rs32,000 crore from domestic centralised VDA exchanges to foreign ones during February-October 2022. More than 17 lakh users switched to foreign exchanges to avoid taxes. As a result, Indian exchanges lost up to 81 percent of their trading volumes in three-and-a-half months between July 1 and October 15, according to Esya Centre, a New Delhi-based technology policy think-tank, and Taxsutra, a B2B tax portal.

Industry experts have been demanding a regulatory framework and also reduction of TDS to 0.1 percent instead of one percent. “If you make the ecosystem so difficult, if we are not regulating the system on time, we are the ones who are losing because the bright minds will definitely go out and do something outstanding. The way this Budget has portrayed TDS is very difficult for the entire ecosystem. The overall Web3 ecosystem in India is not flourishing the way it should," says Sidharth Sogani, founder and CEO of Crebaco Global, a crypto and blockchain market research and ratings firm.

The trading volumes on Indian exchanges dropped considerably, the investors thought what is the point of paying 30 percent tax, and exchange volumes went down by 97 percent, says Sogani. Other than this, the crypto market was very bearish, the sentiment was bad especially after the FTX collapse. As a result, exchanges have been suffering. “Now with this penalty coming in, we observe that the government is placing crypto shoulder-to-shoulder with online gaming and betting websites. It is more towards gambling. Positioning crypto with gambling and online gaming is wrong, that should not be the criteria because they are not seeing the technology and the potential of startups that are coming in," he adds.

Gaurav Sahni, who has been investing in cryptocurrencies from over two years now, explains that taxing crypto profits is understandable but they should reduce the tax from the current 30 percent rate as this brackets investors in the category of gamblers. Also, there are still no regulations in India regarding crypto, unlike many other countries where they charge crypto gains as capital gains and are taxed in the same category, but also provide consumer protection rules. Sahni had started trading on Indian exchanges, and after last year’s Budget announcement, he moved on to trading on foreign exchanges.

“For traders to individually calculate TDS on each trade is a bit out of question, and foreign exchanges have same set of rules for Indian and customers from other parts of the world. They can"t levy TDS on Indians specifically," says Sahni, 35, who also runs his family business and deals in trading of automobile spare parts. Sahni has no plans to stop trading, he will instead find other ways to escape the TDS. “It"s not about dodging taxes. Basically if we pay one percent TDS on every trade then by the 100th trade almost 50 percent of our capital is wiped out through just TDS."

Sahni feels blockchain technology will get more adoption in future and crypto coins are a way to incentivise blockchain technology where developers get remuneration for the projects they develop. “Crypto trading is still not mainstream and majority of people in India still think of them as some kind of scam due to the extreme volatility and fluctuations in the price of the crypto coins," he says.

On February 4, Economic Affairs Secretary Ajay Seth said that the regulations around crypto assets would be brought in this year. "The technology of crypto assets like blockchain and others can be used but its use in the financial sector can have several risks. In the course of this year, measures around crypto would be brought out," he said at a post-budget press conference in Mumbai.

According to the Economic Survey 2023 released on January 31, the market valuation of crypto assets fell from $3 trillion in November 2021 to less than $1 trillion in January 2023. The survey strongly called for a common global framework to regulate crypto assets citing the high volatility of the tokens and the different approaches being taken across countries to evaluate and regulate crypto.

“Tax us, that"s not a problem. But don"t put us in shackles where we are alive but cannot grow. Either ban it completely or regulate it completely. If you are not able to regulate, it"s your problem, not ours. That doesn"t mean that you confine the growth of the industry," says Sogani of Crebaco Global.