In June, VI said its promoters UK’s Vodafone Group Plc and the Aditya Birla Group were likely to infuse up to Rs9,000 crore of fresh capital into the company to revive its business.

The company, which is majority government-owned, is also expected to clear its dues of Rs2,400 crore to the Department of Telecommunications (DoT) by September, VI officials have said.

In August, VI CEO Akshaya Moondra told the DoT that VI has term sheets from several potential investors for capital infusion. He said discussions with multiple groups of investors on both equity and equity-linked instruments had progressed. …."particularly in the last one month where some of these discussions have started progressing to a level of due diligence or proposals being discussed with these investors," he told analysts at an earnings call on August 16. Moondra said he expects “to conclude these discussions in the coming quarter" [Oct-Dec].

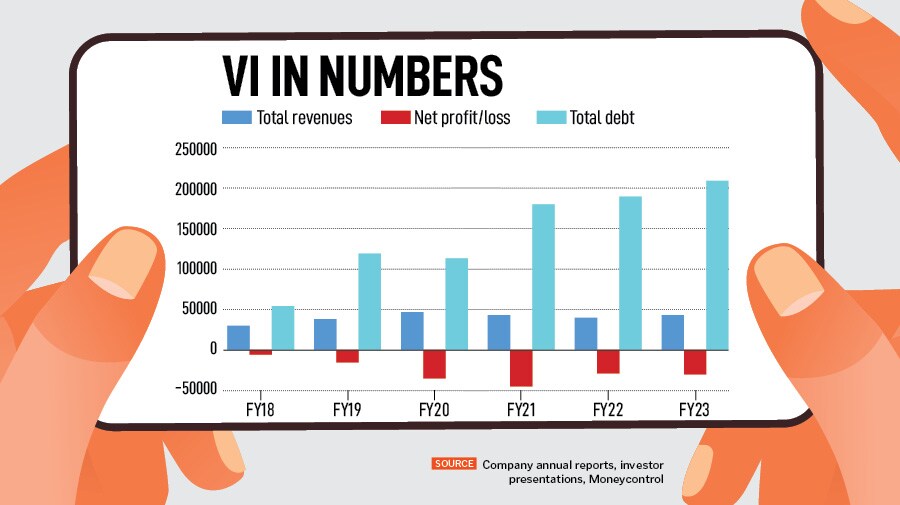

The telco has a total gross debt excluding lease liabilities and including interest accrued but not due of Rs2,117.6 billion as of June 30, 2023, VI’s CFO Murthy GVAS has said. The company owes the government Rs41,300 crore each year as regulatory payouts, from October 2025 onwards, after the four year moratorium ends.

![]()

Substantial investment required

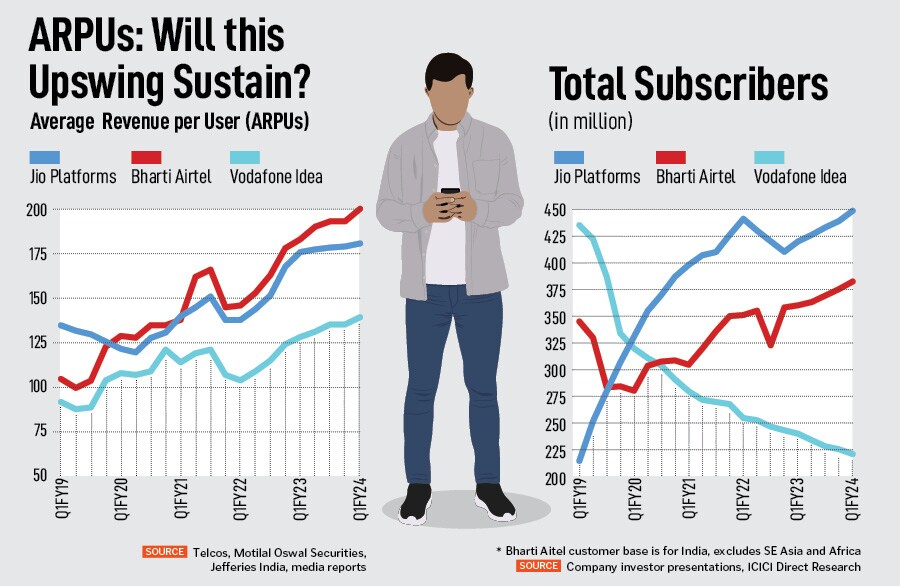

Considering that VI’s FY23 topline is barely above Rs42,000 crore, it will be very difficult for the company to cough up this type of amount due to the government, in the next two years. The possibility of a skyrocketing of revenues in coming two years appears difficult considering it is losing subscribers (see chart) and pricing, though on the rise, is slowing in pace (see chart).

VI has been losing subscribers for at least 20 successive quarters (since June 2018) and suffered losses for six straight financial years since the company was created through the merger of Vodafone India and Idea Cellular.

This is why the capital infusion is much-needed. Experts Forbes India spoke to say VI will need a substantially large investment, ranging from $4-6 billion (to start creating a change) to $10-15 billion (to be a viable No 3 player).

There is no clarity at this stage whether investors are keen to pump in that amount of equity into VI. A debt option is something the government will need to decide or allow for VI.

The government has the option to convert the principal into equity. While the conversion parameters are not known, there is a strong possibility that this could take place and result in a 60 to 70 percent ownership for the government in VI. The accrued interest portion towards AGR dues cost VI 33.1 percent, (held by the government). “What would the principal amount cost them," a telecom consultant said, declining to be named.

![]()

The government is VI’s largest shareholder with a 33.1 percent stake, followed by UK’s Vodafone Group Plc (32.3 percent), the Aditya Birla Group (18.1 percent), and the balance 16.5 percent is public shareholding.

“Even if VI does get an external funding, a significant chunk will go to paying creditors such as Indus Towers, and spectrum installments. How much will be available to rollout the 5G network is difficult to assess," says Balaji Subramanian, vice-president, institutional equities at IIFL Securities.

VI is yet to roll-out 5G network, where rivals Jio Platforms and Bharti Airtel have already marched ahead.

The quarterly capex of Reliance Jio is $2 billion and near $1 billion for rival Bharti Airtel, compared to $0.05 billion for VI. “Vodafone Idea may, thus, need an investment of $4-6 billion to start creating a meaningful change," Balaji told Forbes India.

VI did not respond to queries relating to the potential investment and the 4G rollout details.

“With the more frequent capital raising cycles and rapid technological changes, telecom companies with smaller balance sheets are finding it very difficult to cope with these changes. The third and fourth players, even across high ARPU [average revenue per unit] countries, are finding it tough to remain profitable," says former Bharti Airtel CEO Sanjay Kapoor, who is now an entrepreneur and TMT consultant advising various telecom companies.

VI is getting small chunks of money periodically, which is like good money chasing bad. Even if they get a huge chunk, they will be a distant third in an oligopoly. The third player in the market is usually struggling to make money. This has been seen in the telecom ecosystems in China, Philippines and Singapore.

Bet more on 4G?

Hari Venkatachalam, an IT professional, who resides in Mumbai, is a RedX subscriber of VI on the 4G network. His RedX 1101 plan offers him a premium postpaid experience with unlimited data and calls, 3000 SMSs, Wi-Fi calling, bundled with entertainment packages from Amazon Prime, Disney + Hotstar and Sony Liv. The plan also comes with an additional international roaming 7-day plan worth Rs2,999, once a year, offering international and domestic airport lounge access and discounts on some discounts on hotel and flight bookings from MakeMyTrip.

Venkatachalam (name changed) is a VI faithful subscriber for the past 14 years. “I have found VI to be the most reliable and suitable for me with their international roaming packages, during my business travel to Dubai, Singapore and the US," he told Forbes India. “I am satisfied with the resolution and coverage which 4G provides to me. I am not a tech buff and do not see the immediate need for high-speed analytics or video streaming," he said.

Venkatachalam, a frequent traveler and mobile user, is the type of customer VI should focus on, aiming to provide these customers with enhanced 4G network services so that they may not be tempted to switch to 5G technology, available with competition. VI’s Moondra in August told analysts that it saw a “larger churn" of subscribers in the last quarter, but considering that the ARPUs have increased and so have its 4G subscribers, the “churn is more skewed towards the lower average revenue per unit subscribers."

VI added one million 4G subscribers in the June-ended quarter, though it continued to see a net subscriber loss.

![]() The consolidation of the Indian telecom industry to a quasi-duopoly may relegate the tower companies to captive businesses.Image: Shutterstock

The consolidation of the Indian telecom industry to a quasi-duopoly may relegate the tower companies to captive businesses.Image: Shutterstock

So when Jio and Airtel are pumping in capital to expand their 5G networks, would it be sensible for VI to stay focussed on 4G? “If 5G were that big a differentiator, VI would not be able to continue to add 4G subscribers to its base," Vivekanand Subbaraman, a telecom and media analyst at Ambit had told Forbes India in June.

“VI will become more competitive in 4G because they will rollout 4G before stepping up with 5G. 5G may not have compelling use cases as we speak – but customers who are consuming unlimited data might want to go with 5G," says IIFL’s Balaji. He also suggests that VI might want to start cutting down their presence in 17 circles to a few circles, maybe even think about become regionally strong.

Also for a few years more, 4G is going to remain the meaningful contributor to revenues for these telcos. Monetising 5G technology will not only be tough but it will also take time. VI has bought 5G spectrum (mid-band 3300 MHz and high-speed mmWave) worth Rs18,799 at last year’s spectrum auction.

The 5G network will obviously need to be met—or even outpaced—by the infrastructure rollout for this network. The indoor 5G coverage for customers needs to improve. Jio and Airtel have rolled out around 2.75 lakh 5G base transceiver stations (BTSs) by July 2023, adding 1.35 lakh BTSs in the last 3 months, an Emkay Global research report said in July.

But almost half of the BTSs have been added in only six states—Maharashtra, Uttar Pradesh, Tamil Nadu, Karnataka, Gujarat and West Bengal.

Jio is estimated to command 80 percent of the BTSs at near 2.21 lakh while Airtel had the balance 20 percent, the report showed.

China is way ahead of its 5G BTS rollout compared to India. China has built 30.5 lakh 5G BTSs by July, according to a report released by its Ministry of Industry and Information Technology. Its 5G subscribers were at 695 million, accounting for 40.6 percent of the total number of mobile phone users.

The way forward

A unique situation is emerging for the Indian telecom infrastructure ecosystem. Kapoor says: “The consolidation of the Indian telecom industry to a quasi-duopoly may relegate the tower companies to captive businesses. This is absolutely against the spirit of creating tower companies which had envisaged liberal sharing of passive infrastructure for greater good of the entire eco-system and the nation."

Kapoor has been a board member of Indus Towers, a leading telecom tower company. While VI has paid up monthly instalment-based charges to Indus Towers in 2023, there is little clarity on paying up previous dues. A Kotak institutional equities report in July had pegged this at Rs9,500 crore. But these dues will substantially reduce once VI can tie up its fresh capital infusion plans. VI is believed to account for 40 percent of Indus’s revenues.

While the government’s future course of action towards VI is difficult to assess, it could also improve.

“The magic bullet for VI will come if there is a reduction in the net present value (NPV) of the liability but that does not seem to be a probability. That will cure VI of all its problems. They might want to consider the option of sharing spectrum with Bharti Airtel. In the past, players had traded or shared spectrum," says IIFL’s Balaji.

VI has a fair share of low-frequency spectrum, which Bharti might need and it could charge Airtel for it. The government will also benefit with some license fee due to spectrum sharing.

As VI gets closure to finalise an external capital infusion, their body language and communication to all stakeholders has improved and is getting more confident. Till then, of course, it will be business as usual for them: Focussing on the 4G rollout, upgrading subscribers first from 2G to 4G and then trying to move 4G subscribers to a higher plan.