Waves coming in and out: How to deal with market volatility, experts advise

A roller coaster ride is part and parcel of investing in the markets, highlighted especially since March 2020 when they have plummeted and reached all-time highs, only to tumble again thanks to Russia

The current situation, where the Nifty corrected from its all-time high of 18,477 in October 2021 to 15,863 in early March and has remained volatile since, against the backdrop of fears of a rise in oil prices, hike in interest rates, high inflation and the Russia-Ukraine crisis, has been yet another in the line of events that markets are bound to react to, and which in fact provide an entry point to investors

Illustration: Chaitanya Dinesh Surpur

Advertisement

When a friend from Kolkata called up Nilesh Shah to ask why his portfolio had not generated the returns that the Kotak Emerging Equity Fund had, the latter first thought it was because the friend was comparing the returns of his diversified portfolio—which included gold, real estate and debt—to those of a mid-cap high-risk fund. When the friend said he was talking about his equity portfolio, Shah, managing director of Kotak Mahindra Asset Management Company, decided to take up the matter with the friend’s accountant. The accountant informed him that his friend had booked his losses in equity in March 2020, at the bottom of the market, so how could it deliver the SIP kind of returns the fund had generated?

“I immediately called up my friend and he said, ‘Covid-19 tha, there was so much gloom so humne bech diya (It was Covid-19, there was so much gloom, so I sold it off). This was an informed investor who did not need any money but because he panicked, he ended up converting a notional loss to a real loss."

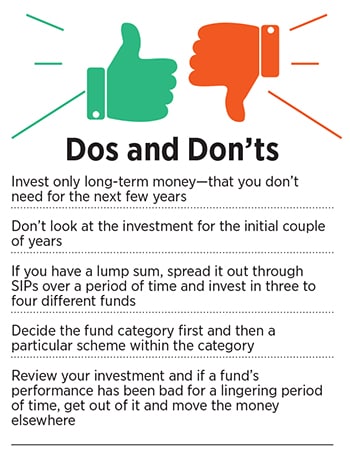

It is probably why financial advisers’ lists of dos and don’ts when dealing with the markets is mostly a list of don’ts—don’t invest money that you would need in the short term, don’t invest lump sums, don’t look at it every day, and since it is the nature of markets to be volatile, don’t panic. Instead, if you are invested for the long-term, just continue doing what you are doing, and do nothing. Or if you want to tweak your portfolio, think of what you can do to benefit from the situation.

The current situation, where the Nifty corrected from its all-time high of 18,477 in October 2021 to 15,863 in early March and has remained volatile since, against the backdrop of fears of a rise in oil prices, hike in interest rates, high inflation and the Russia-Ukraine crisis, has been yet another in the line of events that markets are bound to react to, and which in fact provide an entry point to investors.

Most people, says Shah, want certainty. “A market going down is a short-term phenomenon. How does that become uncertainty for you? If you are a child and you go to the sea, do you get worried about the waves coming in or going out? In fact, most kids will run to the sea and enjoy the waves coming in as well as going out. That is the innocence of kids which makes them accept waves naturally. Markets ka bhi utaar chadav hai (markets also fluctuate)… it is waves coming in and going out." One needs to accept that, he adds, and make adjustments to portfolio allocations “where, by and large, one remains overweight in assets that are cheaper, and underweight in assets which are expensive". This dharma, he adds, will ensure that you get your returns.

Dip in

The US monetary policy and the Ukraine-Russia tensions were both on the watchlist of financial planners’ list of things that could be spoilers in 2022. Three months into the year, both the monetary policy risk and the Ukraine one have become clear. And actions to be taken differ not just in the kind of investments in a diversified portfolio but also the kind of investors. When it comes to equities, experts point out that now that the above two risks have played out one can be more aggressive, especially since valuations, which were above fair value in the bull run last year, are now in reasonable territory after the recent fall. “While higher crude and other commodity prices will weigh into demand and margin pressure in the near-term, investors should use this market correction as an opportunity to increase allocation to equities and align it to their long-term financial goals," says Sorbh Gupta, fund manager-equity, Quantum Mutual Fund.

However, when it comes to fixed income investments, in a rising interest rate environment, one has to be careful about the type of bonds one buys and weigh the returns. If there is no major advantage, one should be in the lowest risk asset, points out Srikanth Bhagavat, managing director and principal advisor, Hexagon Wealth, an investment advisory firm.

“This year, because rising interest rates, inflation and higher government borrowing are all weighing on our minds, we have to be more careful in our approach to fixed income. For example, if I am buying a triple A corporate bond, one should ask how much more return I am getting than a government security. And if the incremental return doesn’t look all that great, one should not go for it. One should be in the safest issue of government of India bonds or public sector bonds," he says. One should also look at the tenure—short versus medium versus long term bonds—and ensure that the return is much higher than the very short term. “And that the extra carry is sufficient to absorb any risk of bond prices falling due to higher interest rates," adds Bhagavat.

Investing in Real Estate Investment Trusts (Reits) and Infrastructure Investment Trusts (InvITs) has also played out well in the past year, thanks to the fact that they have underlying assets, and they remain good bets as part of diversification of the portfolio, he says. Reits and InvITs are asset classes that allow developers to monetise revenue-generating real estate and infrastructure assets, while enabling investors or unit holders to invest in them without actually owning them.

Another element of diversification that became popular last year was investing in international stocks, and that too continues to remain important despite the fact that stock markets have corrected globally. “In fact, because India stocks have fallen only 10 percent while foreign stocks have fallen much more, maybe there are opportunities there. So that is something you can invest in," says Deepak Shenoy, founder and CEO of Capitalmind, though he adds a caveat: It’s for people who know what they are doing.

Cryptocurrency, on the other hand, has turned out to be a speculative bubble, failing to do all the things it was supposed to do—be a hedge against inflation and the printing of currency, a good place to be in in times of uncertainty, and be competition to gold. Instead, says Bhagavat, it has eroded in value in the face of all the recent uncertainties, even as gold has held its own. “Hopefully, investors have seen it for what it is and will avoid it," he says.

In a volatile market, the strategy also differs depending on whether one is a short, medium or long-term investor as well as their experience. Short-term investors should remember that markets are unpredictable on a short-term basis, says Dhirendra Kumar, CEO, Value Research. They should stay away from equities in the short term and instead invest in appropriate kind of funds—if it’s for a few days in a liquid fund, for a few months invest in an ultra-short term bond fund, and if it’s for a year or two, and if one is risk-averse, in a short term bond fund.

Medium-term investors, or those who were investors with long-term goals and a horizon of about 10 years but are now approaching that goal in in one to two years, can start taking out their money methodically and regularly, and putting it into less risky and fixed income instruments, thereby securing their capital. “Don’t wait for the last day because at that time the weather can be bad in the market and that could be a very devastating thing," says Kumar.

While for long-term investors, it’s time to buy cheap, buy in tranches or through systematic investment plans (SIP), become conservative, and stay put. “Anyone who has limited experience should still be conservative. If you came in the market in the last two-three years and started with a small cap fund, you are lucky that small caps haven’t fallen as much. Become conservative, be more diverse and have a slightly higher fixed income allocation. And an experienced investor should do nothing. If anybody has been in the market for the last five years, they would have gotten used to the ups and downs," he adds.

One of the positives this time round has been that the Indian market has been resilient despite FIIs (foreign institutional investors) pulling out money on a large scale. In just February, there was a sharp surge in FII outflows of $4.7 billion—the highest since March 2020—taking the total outflows to almost $9.5 billion in the past four months. On the other hand, domestic investors have been net buyers and have absorbed a lot of selling pressure from the FIIs. Money is finding its way into the markets through mutual funds and SIPs, the government putting in money from the Employees Provident Fund, as well as the National Pension Scheme and all these are only getting bigger, points out Kumar.

Starting point

With every market cycle and every year, a new generation and a new set of investors enter the market. While, as they say in the world of mutual funds, past performance is not an indicator of future returns, and the best funds can take a turn for the worse, while a bad fund can become good, a few ground rules help in navigating the world of investing and mutual funds, depending on age and experience.

What is important initially is to acclimatise yourself, says Kumar. “There are children who start learning cycling and they do it with supports, so that they don’t fall. It’s like that, like having a tube when you are learning swimming." You might win some and you might lose some, but it’s a good idea to start early and learn when the bets are low. “So anyone who is 30-35, earns something, saves something, invests something and loses something, it’s fine. The only thing is they should retain the learning."

There is, experts say, no point in waiting to spot or find the best fund. But broadly, pick a fund category and then zero in on a scheme. Someone in their 50s investing for the first time should start conservatively, say with an equity savings fund. While someone in their 30s and 40s could start with a balanced advantage or an aggressive hybrid fund. While those who can be a little adventurous could opt for a flexi cap fund.

Then there are also index funds, which could be another starting point. In the last month alone, according to the Association of Mutual Funds in India data, 10 new Index funds—passively managed funds that mimic popular market indices—were launched. Reasons for their popularity include the fact that they are easy to run and don’t need a fund manager. For investors, this translates into broader diversification and a low expense ratio. And while there will always be funds that will do better than index funds and others that might underperform the market, one can expect reasonable returns over a period of time from index funds. As Kumar says, “If you are investing in a multi-cap fund, do it. If you are investing in an index fund, do it. The point is that even index funds have a great chance of beating inflation." At the end of the day, that remains the basic criteria.

However, when it comes to fixed income investments, in a rising interest rate environment, one has to be careful about the type of bonds one buys and weigh the returns. If there is no major advantage, one should be in the lowest risk asset, points out Srikanth Bhagavat, managing director and principal advisor, Hexagon Wealth, an investment advisory firm.

However, when it comes to fixed income investments, in a rising interest rate environment, one has to be careful about the type of bonds one buys and weigh the returns. If there is no major advantage, one should be in the lowest risk asset, points out Srikanth Bhagavat, managing director and principal advisor, Hexagon Wealth, an investment advisory firm.