Be prepared for the worst while you are building a business at scale: Bizongo co

It's rare to miss the unicorn tag by a whisker. This is exactly what happened with Bizongo, which fell short of $20 million. As the gloomy forecast of a parched funding spell looked imminent, the prag

Sachin Agrawal, Co-founder and CEO, Bizongo

Image: Madhu Kapparath

Advertisement

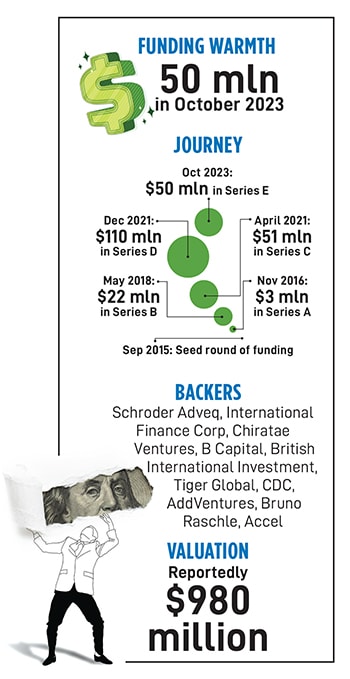

The first four letters came as easy as ABC. Have a look. Series A in November 2016, Series B in May 2018, Series C in April 2021, and Series D in December 2021. The progression of the four funding amounts was heady. Sample this. $3 million, $22 million, $51 million and $110 million. The trajectory of the first four valuations defied earth’s gravity. Check it out. Negligible, still miniscule, $130 million, and $600 million.

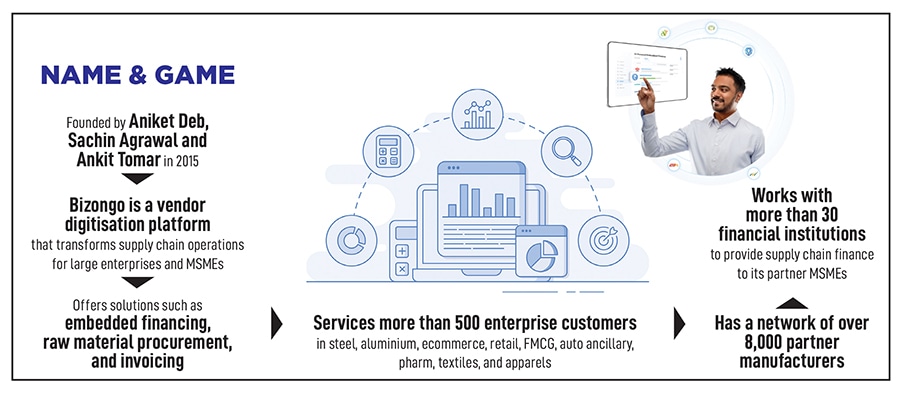

And then came Series E in 2023. And for Sachin Agrawal, ‘E’ was not easy. The letter stood for ‘evaluation’. The co-founder of Bizongo explains. “Judged on business fundamentals, I have no hesitation in accepting that we were overvalued," the CEO of the vendor digitisation platform makes a candid confession. “But that’s how growth startups are valued in a growth economy like India," he underlines. “Right," asks Agrawal who co-founded Bizongo with Aniket Deb and Ankit Tomar in 2015. “We knew we were over-valued," he says.

Agrawal is right. But he was not the only founder who lived with unrealistic valuations. From a dozen unicorns produced in India in the pandemic year, the numbers galloped to 44 in 2021, a year of funding deluge. The following year—especially the second half—the bull started to turn bearish. There were only 26 unicorns in 2022. Getting stratospheric valuations was fast becoming a thing of the past, and a funding winter proclaimed its unwelcome presence last July, when monthly funding dipped to $870 million from a high of $4.57 billion in January. When contrasted with the corresponding funding number notched up in July 2021—$4.65 billion—the forecast was definitely numbing.

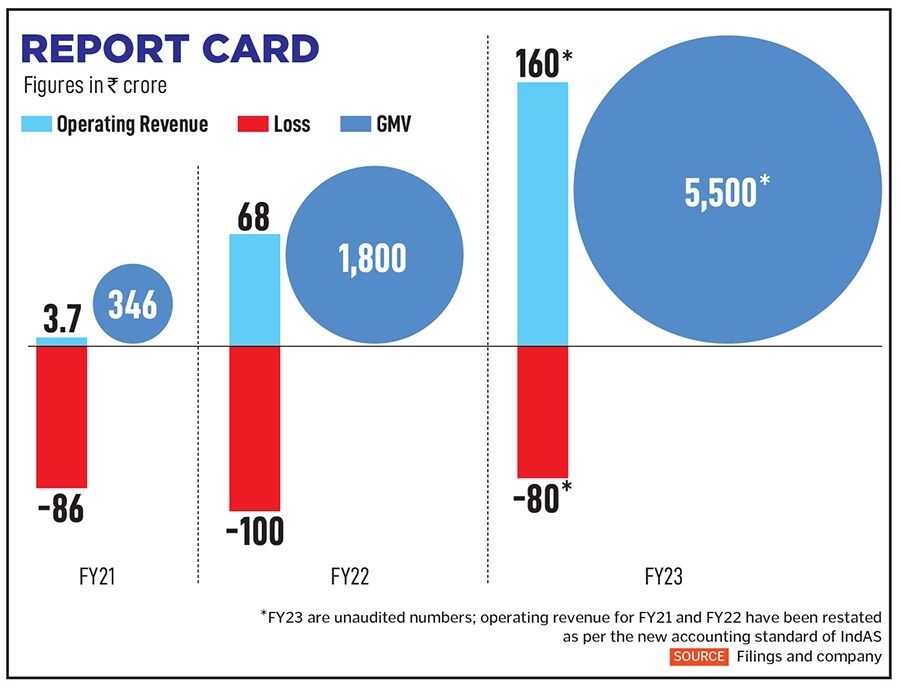

The founder, though, stayed bullish when he decided to hit the market to raise funds in October 2022. And this time his optimism was realistic, and was founded on strong performance churned out by his venture. Gross merchandise value (GMV) jumped from ₹346 crore in FY21 to ₹1,800 crore in FY22, and operating revenue during the same period leapfrogged from ₹3.7 crore to ₹68 crore. Though losses remained on the higher side—₹86 crore and ₹100 crore in FY21 and FY22, respectively—Agrawal had been running a tight ship, was confident of more than doubling the revenue and GMV, and was certain that Bizongo was on track to generate maiden free cash flow in FY23. Well, things indeed looked promising, and the mood was euphoric. “We were quite relaxed, and we went into the process with a lot of enthusiasm," he recalls. The plan was to reach out to the top 10 investors and get a few on the board.

The outcome was beyond expectations. A big global investor decided to make its India debut by taking a punt on the startup. The terms of the deal were finalised in November, and the fund confirmed that they would lead the funding round by putting in $40 million. “We were on cloud nine," recalls Agrawal.

A week later, there was a cloud burst. Silicon Valley Bank collapsed, the potential funder chickened out, and the funding applecart turned topsy-turvy. A series of more bad news started pouring in from the global tech front. The crypto market was collapsing at an alarming pace, tech stocks were getting brutally battered, and investors started looking for cover. The funding environment suddenly turned into a typical day of a cricket Test match in London, where an unexpected cloud cover engulfs the ground, the ball starts seaming and swinging menacingly, and the batters look like a bunch of sitting ducks waiting to edge the ball to the slip cordon.

Back in India, there was no let-up for Agrawal. A bunch of startups started hogging the limelight for the wrong reasons: Glaring absence of corporate governance and embezzlement of funds. The investing community turned cagey and was gripped with an exaggerated sense of fear. Every startup started to be viewed through a suspicious lens. Meanwhile, the long list of 10 investors that Agrawal had prepared came down to zero. Nobody was keen. Consequently, the founder added 40 more funds on the prospective list of investors, and started reaching out.

Things were tough. First, the growth money vanished from the market. Second, the ones who were still game wanted to come in at an old valuation. This didn’t make any sense to Agrawal for obvious reasons. And third, there was a sudden change in lens to look at startups. The founder explains the new rules of the funding game. “Everyone started looking at valuing a startup on the basis of multiples of return on capital or multiple of PBT [profit before tax]," he says.

The new order, though, had a serious issue. “If you’re applying public market multiple, then you can’t justify your existing valuation," says Agrawal, who was trying to get a premium on Bizongo’s previous valuation of $600 million. Nothing moved over the next few months, Bizongo generated ₹50 crore of free cash flow in FY23, and it became clear by the beginning of July—which meant end of the first quarter of FY24—that Bizongo will have to continue with its limited resources. Though the startup still had ample runway, the founding team decided to focus sharply on operational metrics so that there was less need of outside capital. The trade-off meant replacing ‘high growth’ with ‘sustainable growth’.

A change in strategy also brought in an interesting development. One of the venture capital (VC) funds wanted to invest but came with a unique demand: The books had to be audited by Deloitte. Bizongo, which already had EY and PwC, agreed to start the diligence process again. Later on, the startup also roped in KPMG. “We were perhaps the only startup which were working with all the big four auditing firms at the same time," smiles Agrawal, adding that if one wants to be IPO-ready over the next three to five years, one has to be stringent in compliance, norms and accounting.

The move resulted in adding an extra layer of financial structure as Bizongo shifted to a new accounting norm. As per the new accounting standard of IndAS, explains Agrawal, the operating revenue for FY21 and FY22 were restated. By the end of October, Bizongo managed to raise $50 million in Series E funding, which happened to be the toughest as well as the lengthiest. Though the valuation jumped from $600 million to $980 million, the startup missed the unicorn tag by just $20 million. “We were almost there, but don’t regret missing the unicorn tag," says Agrawal. “In fact, it was a blessing not to be a unicorn."

Anand Daniel tells us why the $50-million fund raise by Bizongo was a big feat. The Indian startup ecosystem, underlines the partner at VC firm Accel, witnessed an unprecedented dip in funding over the last 12 to 18 months. Fundraising, he stresses, has been more difficult for companies attempting to close a round north of $500-million valuation. “Despite this macro backdrop, the compelling vision of Bizongo to transform B2B supply chains was something investors were upbeat on," he says.

Across its key segments, the funder lets on, Bizongo plays in a value pool greater than $100 billion, which makes the opportunity immense. “We are excited to see the company onboard new customers and vendors," he adds. The challenge, though, would be to grow in a sustainable manner. “What will remain critical going forward is to achieve this ambition in the most capital-efficient manner," he says.

Agrawal, meanwhile, now knows the value of every penny, the flip side of chasing valuations, and the pressing need to grow sustainably. “This winter has taught me that one has to be prepared for the worst," he says. Unicorn or no unicorn, businesses have to be built the way businesses were always meant to be: Make profit. Well, Bizongo, which means ‘business on go’, can only grow if it makes money in all seasons.

Agrawal is right. But he was not the only founder who lived with unrealistic valuations. From a dozen unicorns produced in India in the pandemic year, the numbers galloped to 44 in 2021, a year of funding deluge. The following year—especially the second half—the bull started to turn bearish. There were only 26 unicorns in 2022. Getting stratospheric valuations was fast becoming a thing of the past, and a funding winter proclaimed its unwelcome presence last July, when monthly funding dipped to $870 million from a high of $4.57 billion in January. When contrasted with the corresponding funding number notched up in July 2021—$4.65 billion—the forecast was definitely numbing.

Agrawal is right. But he was not the only founder who lived with unrealistic valuations. From a dozen unicorns produced in India in the pandemic year, the numbers galloped to 44 in 2021, a year of funding deluge. The following year—especially the second half—the bull started to turn bearish. There were only 26 unicorns in 2022. Getting stratospheric valuations was fast becoming a thing of the past, and a funding winter proclaimed its unwelcome presence last July, when monthly funding dipped to $870 million from a high of $4.57 billion in January. When contrasted with the corresponding funding number notched up in July 2021—$4.65 billion—the forecast was definitely numbing.