Earlier in June, Kotak Mahindra Bank, in association with Myntra, launched a co-branded digital fashion and lifestyle co-branded card, a first of its type, with customers being boarded onto Myntra’s loyalty programme.

On August 24, HDFC Bank—seen to be the market leader of active credit cards issued in India at 1.83 crore—is set to announce a new co-branded partnership with Marriott Bonvoy, the loyalty programme of Hotel Marriott. This is seen to become India’s first co-branded hotel credit card launch.

AU Small Finance Bank too is planning to enter into partnerships for co-branded credit cards in the next one year, its credit card business head Mayank Markanday has said. Industry experts suggest there could be a possible tie-up with a jewellery-based merchant, which could be the first-of-its-type in the co-branded credit card segment.

What made it popular was that it was the first card in India to enable Amazon Prime members to earn 5 percent reward points on shopping on Amazon India. Other customers get 3 percent reward points. They also earn 2 percent reward points on spends at Amazon Pay partner merchants and 1 percent for all other spends.

Its nearest rival in terms of positioning, the Flipkart Axis Bank credit card, has been equally successful. “The card has already crossed 3 million customers a few months back, the next milestone is expected soon," Sanjeev Moghe, president and head (cards and payments) at Axis Bank told Forbes India. Flipkart is distributing the card on their platform and Axis Bank does the underwriting and KYCs, and then grants approval. The extended distribution [from Flipkart] gives the issuing bank swifter access to the customer.

HDFC Bank has also had success with its co-branded credit cards programme. “The co-branded new acquisition portfolio has grown 3X year and has crossed 3 million cards on the book and will continue to be a significant contributor to our overall portfolio in the coming years," says Parag Rao, country-head (payments business, consumer finance, technology and digital banking), at HDFC Bank.

The top-of-wallet challenge

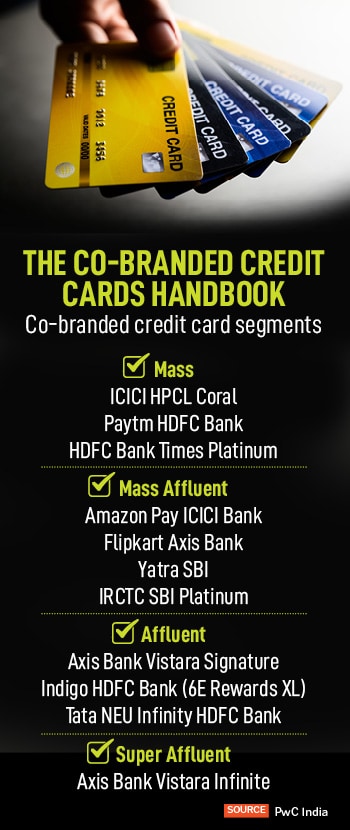

In the 1990s, banks differentiated customer profiles and rewards by issuing just Platinum, Gold or Titanium cards. Consumers did not have a choice at that time to select a card, the type of card issued was based entirely on their income. At this time, the industry was disrupted when Citibank along with Indian Oil Corporation launched India’s first co-branded credit card in 1997. The partnership launched other cards too, including one for small businesses in 2007.

![]()

In the decade gone by, banks introduced a differentiation based on reward points and cashbacks.

Co-branded credit cards offer customers different requirements in terms of reward points and benefits that they want to get by redeeming them in the manner they want to. Earlier cards simply gave generic points which customers could use on their rewards platforms online (electronics, apparel, lifestyle etc.). But these were usually over-priced for the points that the customer consumed and redeemed.

“In these focussed co-branded credit card partnerships, customers know beforehand the benefits they are getting, the value proposition and know how they can utilise their rewards better," says Nitin Aggarwal, head of BFSI research at Motilal Oswal Institutional Equities. “Spend-based points which a customer gets are a bigger driver to spend on a particular card," Aggarwal told Forbes India.

Card issuers have even introduced steep spend threshold limits—as Axis Bank announced recently with its prestigious and popular Magnus card—even as it devalued some of its reward points. The bank has the confidence that the high-net worth individual customers will be keen to spend more—in excess of Rs 2 lakh per month—to earn high rewards and other unmatched lifestyle benefits.

Similarly, even in the HDFC Bank-Marriott Bonvoy credit card, the two partners will hope the users will use the card everywhere but eventually Marriott will see that benefit because once substantial points get accrued, customers will want to use it at Marriott’s properties, because that is where the maximum value will be seen.

This is exactly what Swiggy too will hope to achieve from its new co-branded credit card. It is positioning itself as an ‘all encompassing’ card for users, across food delivery, quick commerce grocery delivery and dining out schemes. Swiggy has 20 million active users per month and more than one million orders per week across 500+ cities.

The card offers a 10 percent cashback on Swiggy spends of Rs 1,500 or more per month, 5 percent cashback on online spends for Rs 1,500 or more per month (excluding rent, utilities, fuel, insurance, EMIs, jewellery) and 1 percent cashback on spends of Rs 500.

In an emailed response, a Swiggy spokesperson says: “This move aligns with Swiggy"s customer-centric approach, enabling unparalleled convenience for its users by offering benefits not only on food and grocery deliveries, but also on various online shopping platforms."

![]() HDFC Bank’s Rao says: “Dining and grocery is an extremely critical daily spending category and we needed a strong customer proposition to complete our product offerings. As a brand, Swiggy follows a solution first approach to consumer demands that is in line with our experience that we intend to offer on our co-branded programmes."

HDFC Bank’s Rao says: “Dining and grocery is an extremely critical daily spending category and we needed a strong customer proposition to complete our product offerings. As a brand, Swiggy follows a solution first approach to consumer demands that is in line with our experience that we intend to offer on our co-branded programmes."

For a merchant as popular as Swiggy, getting customers to transact on this card will not be a concern. Mass affluent customers are going to see value but the bank needs to ensure that spends are not limited to just Swiggy orders and they need to go high-end towards other purchases. Experts say that it takes about 2-3 years to identify if a credit card is successful or not. The uptick happens in the first year but it takes 2-3 years to determine if it is making money for the bank or not.

Swiggy will also need to avoid what Zomato did, in its co-branded journey with RBL Bank. Zomato and RBL Bank had aligned to launch their co-branded card in March 2020 on the Mastercard platform but discontinued it in May 2023, without offering the rationale for the decision. It had launched ‘Classic’ and ‘Black’ variants of the card, wherein the latter offered a 10 percent cashback on every transaction and the Classic offered 5 percent cashback made on the Zomato and quick commerce Blinkit apps.

They could also get access to Zomato Pro membership, besides other benefits like airline lounge access and movie tickets. There is no clarity on how many cards were issued by the bank in the three-year period.

“Customers were not finding a value proposition and probably the customers got confused with the Zomato Gold and Pro membership programmes. They probably could not find the real benefits and then started to use a normal card. The bank found that uptick was not as expected and culled down the programme," an industry source at a research consultancy firm said on condition of anonymity.

Merchants will need to play a more proactive role with banks. “Merchants have to step up and hold the bank’s hand and give the same value proposition and benefits to the customers, so that customers keep coming back to the merchant and use the credit card, so that they have the psyche that they will keep that card as the go-to or top-of-the-wallet card," says Mihir Gandhi, partner and leader, Payments Transformation at PwC India.

Cards: Financial break-even

It is not just the value of the brands, neither the number of cards issued nor the awareness that determines the success of a co-branded credit card. The financial break-even for a card issued by a bank will be the outcome of the interchange fees (fees which a merchant will pay to the bank when a customer makes a purchase from their platform).

![]() The bank makes revenues on the card based on three modes: Interchange income—usually 1.8 percent on every transaction spend, plus fee income (annual, renewal, late or processing fees) on credit cards interest income—the money seen as revolving credit where customers will carry forward outstanding dues and not repay the entire outstanding amount. The third is EMI interest, where the bank prompts the customer to convert the amount due in a large transaction into EMIs and pay a lower percent interest to the bank.

The bank makes revenues on the card based on three modes: Interchange income—usually 1.8 percent on every transaction spend, plus fee income (annual, renewal, late or processing fees) on credit cards interest income—the money seen as revolving credit where customers will carry forward outstanding dues and not repay the entire outstanding amount. The third is EMI interest, where the bank prompts the customer to convert the amount due in a large transaction into EMIs and pay a lower percent interest to the bank.

"The bet that all banks are taking is that they can recover their costs if the same customer on the same card makes it a primary card and uses that primary card to make different types of purchases—grocery, education fees, movie ticket purchases (the bank may give a 1 percent cashback on these type of transactions but is making 1.8 percent interchange fees on the total transaction)," says PwC’s Gandhi. “The bank is unlikely to make money on merchant transactions (where there is a 5 percent cashback), unless there is a healthy amount of revolver or customers who pay annual fees or EMIs or interest, " he added.

As customers have grown more credit conscious post Covid19, for a matured credit card company, the break-up of these categories is a third each.

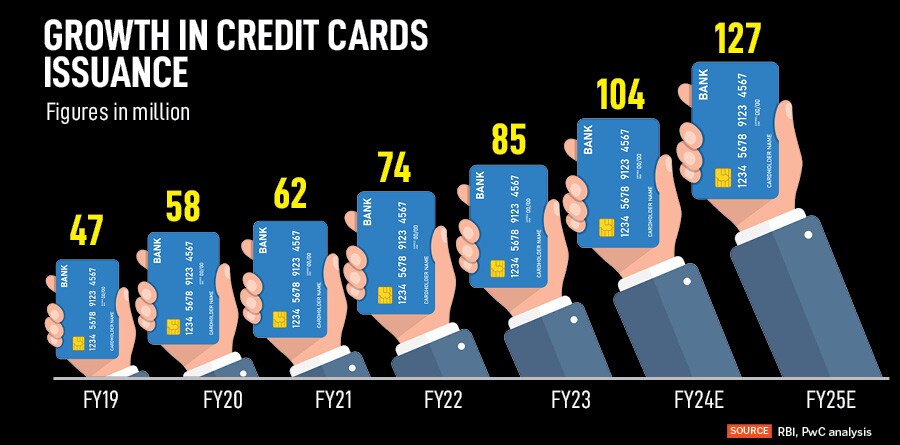

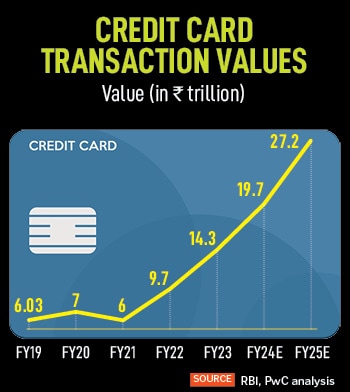

How much co-branded credit cards command as a share of the credit cards universe is unclear, ranging between 7 to 30 percent. But it has been growing sharply over the past 5-7 years and will continue to do so. “With credit lines continuing to grow and the number of eligible people for credit cards rising (a young population, spending more), the credit card penetration is still low," says Oswal’s Aggarwal. The RBI estimates around 8.5 crore active credit cards.

The revenue for all credit card issuance increased by 42 percent in FY23 compared to FY22 and is expected to grow by a CAGR of 33 percent for the next five years," PwC has estimated in its ‘The Indian Payments Handbook (20022-27)’. Reserve Bank of India data, as of June 2023, showed a 15.3 percent year-on-year growth in number of transactions (PoS and online combined) and a 26.9 percent rise in value terms for all credit cards.

Thus, data suggests (see charts) that customers will continue to find opportunities to maximise their reward points and cashbacks if they are willing to spend more. For banks, while the opportunities to issue more co-branded cards exist, the partnerships will continue to evolve from the staple airlines, fuel and ecommerce merchants to other segments. The challenge for banks will be to make specific cards the top-of-the-wallet one and encourage customers to increase spends, which will help boost profitability.

Most corporates, in the form of airlines, hotels, online shopping merchants or oil refiners, which have a large customer base, are realising that a co-branded credit card builds customer loyalty and helps them boost their spends. “Many large and iconic brands may come together to form co-branded alliances in future," an ICICI Bank spokesperson told Forbes India in an emailed response.

Most corporates, in the form of airlines, hotels, online shopping merchants or oil refiners, which have a large customer base, are realising that a co-branded credit card builds customer loyalty and helps them boost their spends. “Many large and iconic brands may come together to form co-branded alliances in future," an ICICI Bank spokesperson told Forbes India in an emailed response.

HDFC Bank’s Rao says: “Dining and grocery is an extremely critical daily spending category and we needed a strong customer proposition to complete our product offerings. As a brand, Swiggy follows a solution first approach to consumer demands that is in line with our experience that we intend to offer on our co-branded programmes."

HDFC Bank’s Rao says: “Dining and grocery is an extremely critical daily spending category and we needed a strong customer proposition to complete our product offerings. As a brand, Swiggy follows a solution first approach to consumer demands that is in line with our experience that we intend to offer on our co-branded programmes." The bank makes revenues on the card based on three modes: Interchange income—usually 1.8 percent on every transaction spend, plus fee income (annual, renewal, late or processing fees) on credit cards interest income—the money seen as revolving credit where customers will carry forward outstanding dues and not repay the entire outstanding amount. The third is EMI interest, where the bank prompts the customer to convert the amount due in a large transaction into EMIs and pay a lower percent interest to the bank.

The bank makes revenues on the card based on three modes: Interchange income—usually 1.8 percent on every transaction spend, plus fee income (annual, renewal, late or processing fees) on credit cards interest income—the money seen as revolving credit where customers will carry forward outstanding dues and not repay the entire outstanding amount. The third is EMI interest, where the bank prompts the customer to convert the amount due in a large transaction into EMIs and pay a lower percent interest to the bank.