HDFC Bank Q3FY24 earnings rock stock markets, raising some near-term concerns

Weaker margins and a high credit-to-deposit ratio spooks analysts, but medium to long term fundamentals for the bank stay strong

Last Updated: Jan 17, 2024, 17:17 IST4 min

HDFC Bank, India’s largest private lender, slid 8.97 percent intra-day on Wednesday, dragging the entire stock markets down with it, after reporting weaker than expected earnings in some matrix for its December-ended Q3FY24 earnings.

The stock contributed to over 50 percent of the fall to both the Nifty 50 and the Nifty Bank indices, while erasing over 1 lakh crore of market cap in a single day. By the end of the trading day, HDFC Bank closed down 8.16 percent at Rs1,570 at the NSE. The NSE 50 closed down 460 points or 2.09 percent at 21,571.95 and the BSE Sensex index down 1,628.02 points at 71,500.76 on Wednesday.

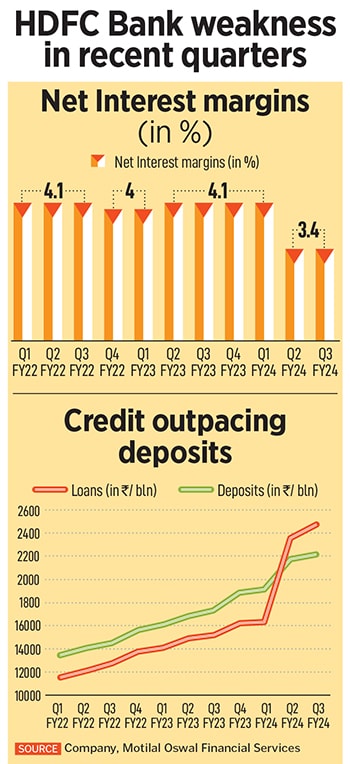

The HDFC Bank reported a year-on-year 24 percent growth in net interest income at Rs284.7 billion and net profit of Rs163.8 billion, up 34 percent, but based on successive quarters, both income and profit grew just 3.8 and 2 percent respectively.

“Margins were largely flat – and slightly below expectations – at 3.4 percent even as the bank deployed excess liquidity and significantly drew down the LCR [liquidity coverage ratio]," says Nitin Aggarwal, head-BFSI (institutional equities) at Motilal Oswal Securities said.

This is what spooked analysts as the Bank’s LCR has come down from 121 percent in the last quarter. This is the matrix which requires banks to maintain high quality liquid assets (HQLAs) to meet 30 days net outgo under stressed financial conditions.

Another area of concern was the fact that loan growth outpaced deposit growth in the period. The loan book grew 3.8 percent quarter-on-quarter to around Rs25,271 billion, while deposits rose by 1.9 percent to Rs 22,140 billion, for the corresponding period. As a result, the CD (credit to deposit) ratio for the merged entity increased to 110 percent in 3QFY24.

“The management expects loan growth to be led by retail loans versus wholesale earlier (mix of 54:46). Within Retail, home loans will remain the key focus areas, and with the unsecured loan growth picking up to high teens, it should aid margins going ahead," says Rikin Shah, banking analyst at IIF Securities.

“The overall target is to double the book in four to five years (implying an 18 percent loan CAGR), but we build slower loan growth of 16 percent CAGR over FY25-26E given the elevated CD ratio of 110 percent," Shah says in a note to clients.

The CD ratio has been on the Reserve Bank of India’s radar for several months now and it has indicated that it wants the ratio to be between 75-80 percent.

The CD ratio has been on the Reserve Bank of India’s radar for several months now and it has indicated that it wants the ratio to be between 75-80 percent.

“While the quarter’s disappointment is undeniable, we see no structural red flags in terms of profitability consciousness in loan-segment choices, CASA market share traction and operating cost control – the keys to our central thesis of net interest margin/ RoA expansion to 3.9 percent / 2 percent by FY26," says Santanu Chakrabarti of BNP Paribas Securities in India.

IIFL’s Shah is of the view that the medium term outlook for the bank appears positive. This will be driven by a pickup in the mortgage disbursements and scaling-up of higher-yielding affordable housing loans. This is a segment which has strengthened for the merged entity. Also, the opportunity to cross sell products to its retail customer is under-penetrated at the moment, estimated at just between 2 to 20 percent.

The HDFC Bank management has told analysts to expect interest margins to improve in coming quarters. “We estimate HDFC Bank to deliver faster deposit growth at 19 percent CAGR while loan growth to sustain at 17 percent CAGR over FY24-26," Motilal Oswal’s Aggarwal says. He estimates HDFC Bank to deliver an FY26E RoA/RoE of 1.9 percent / 16.7 percent.

After watching for two cycles, HDFC Bank will look to have partnerships with fintechs and also intends to do small elements of co-lending. The bank added 2.2 million customers and the customer base stood at 93 million in the December-ended quarter. It also added 150 branches, taking the total branches to 8,091, as of 3QFY24.

The bank has seen the worst of concerns behind it when in December 2020, it had told the bank to stop all launches of its upcoming digital business-generating activities and sourcing of new credit card customers. This action was taken after the bank had seen repeated outages in data. The RBI then lifted all these restrictions by March 2022.

The Q3FY24 earnings of other private lenders ICICI Bank, Axis Bank and Kotak Mahindra Bank, besides public sector giant State Bank of India, will be closely watched in coming days.

First Published: Jan 17, 2024, 17:17

Subscribe Now