How GetVantage is democratising access to working capital for underserved busine

Bhavik Vasa and Amit Srivastava are betting big on the ease, speed and non-dilutive nature of revenue-based financing to give GetVantage an edge in the hyper-cluttered debt and VC world. But can they

L-R Bhavik Vasa and Amit Srivastava co-founders of GetVantage

Advertisement

Raipur, Chhattisgarh. Devkar Saheb’s official induction into the startup world started with the first season of Shark Tank India. “Pichle saal April main ek episode dekha tha YouTube pe, aur pehli baar funding aur venture capital (VC) ke baarey main pata chala (I saw an episode of Shark Tank India on YouTube last April, and got to know about funding and VC for the first time)," recounts the 32-year-old entrepreneur, who founded an ayurvedic FMCG and personal care brand Shri Chyawan Ayurveda in 2018, scaled the bootstrapped venture over the next few years, and closed FY22 with an operating revenue of Rs3 crore. “Shark pata tha, Shark Tank nahin jaanta tha (I knew about shark, but not Shark Tank)," he bursts into a loud guffaw before quickly taking us back to his muted upbringing.

Born into a family of landless agricultural workers in Chhattisgarh, Saheb dropped out of a government school after class 10, joined a Gurukul, studied and worked with the institution till 2017, and started his venture the next year. “Main business bulata tha, venture nahin. Mujhe to startup bhi nahin pata tha (I used to call it a business and not a venture. I didn’t even know the word ‘startup’)," he laughs, adding that till last year, he used to address himself as a director of the company. “Ye entrepreneur aur founder pata nahin tha (I was unaware of terms like entrepreneur or founder)," he confesses and eagerly showcases his wide range of branded products—rusk, snacks, flour, detergent, cookies, biscuits—over a Zoom call. “Even today, not many know about VCs, equity, funding and unicorn in Tier II and beyond," he reckons, underlining the grim reality of lack of access to venture capital, venture debt and angel money across large parts of India.

Is Shri Chyawan Ayurveda still a bootstrapped company? “Technically, yes and no," smiles Saheb. In one of the startup events in Delhi last year, the founder got introduced to GetVantage, and took a loan of Rs20 lakh from the revenue-based financing (RBF) platform. “I didn’t dilute any stake and got money. So, I am still bootstrapped," says the rookie founder, who suddenly starts talking like a startup pro and lists out virtues of keeping equity intact, and not diluting too early and too much. “Who would have backed a school dropout?" he asks. The big world of venture capital looks for degree and pedigree. “I had none," he says, claiming that his venture is likely to close FY23 at an operating revenue of Rs4.5 crore. “I will take my business to Rs100 crore, and then look for VC money," he says.

Meanwhile, in Delhi-NCR, a big player like BluSmart—an electric cab-hailing player which counts BP Ventures among its backers, and has a fleet of over 3,200 cars taking on Uber and Ola across Delhi-NCR and Bengaluru—too saw merit in taking the RBF route and raising Rs25 crore from GetVantage. Bhavik Vasa, founder and CEO of GetVantage, explains why companies of all shapes and sizes are hopping on to the RBF wagon.

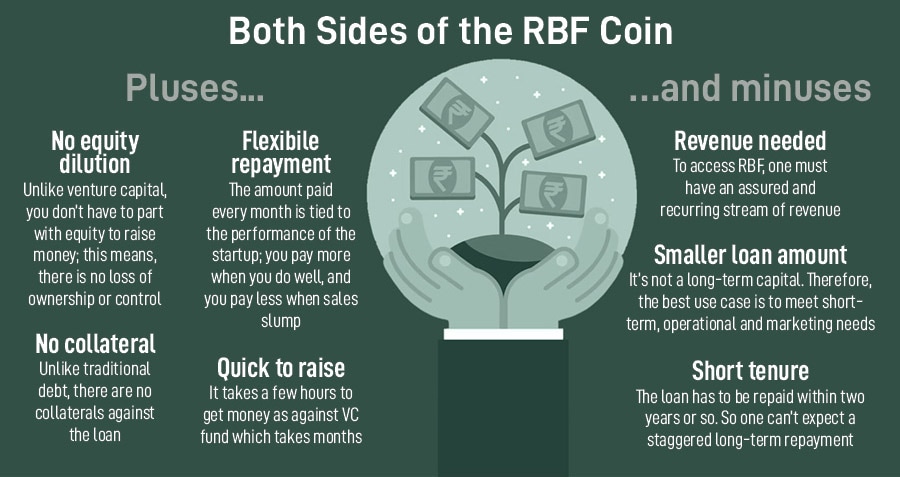

Unlike venture capital, GetVantage gives founders an opportunity to raise growth capital without giving up ownership or control of their business, he reckons. Though equity can often be one of the most expensive ways of raising working capital, many founders are also wary of the interest rates of traditional debt and the paraphernalia around it like personal guarantees or warrants. “GetVantage offers a fair, flexible, and founder-friendly alternative to raise money," he claims, adding that RBF works both complementary to and supplementary to venture capital depending on the size and stage of the businesses raising money.

The opportunity is indeed big for an alternative funding platform like RBF. While most of the startups and small businesses remain out of the radar of VCs, venture debt players only come into the picture once a startup has a VC on its cap table. And then there is a sizeable chunk of founders who lack personal or professional connection—read alumni connect of IIT, IIM, Ivy League or a fancy consulting background.

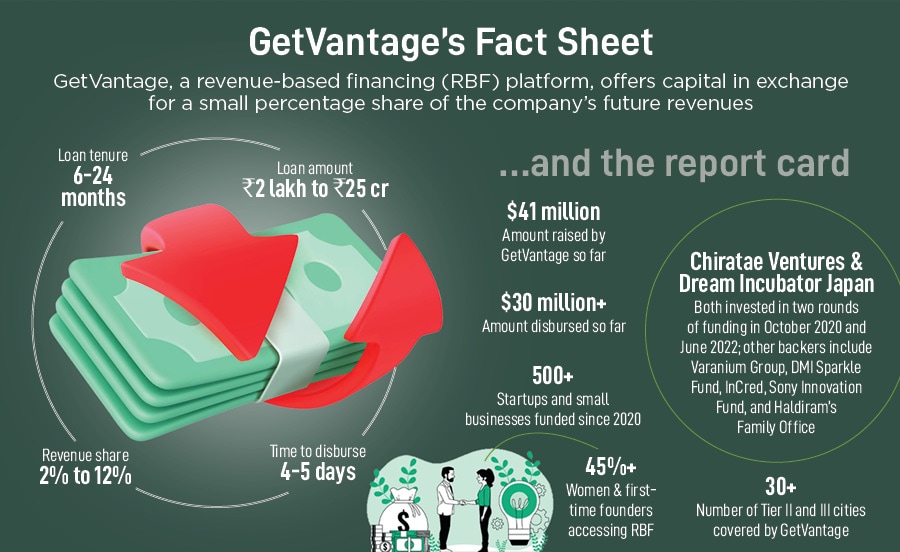

Vasa, though, points out a diversified set of problems. Most digital businesses face two major challenges: Getting quick funding for marketing and inventory, and acquiring and retaining customers. “The old world of fundraising was based on who you know," he says, adding that the new world of fundraising is based on data and business fundamentals. Depending on how sound the financials of a startup are—recurring revenue and a good cash flow—GetVantage offers tailor-made packages to the founders. “The non-dilutive financing model is a more balanced, structured and step-wise approach," contends Vasa, claiming that GetVantage is the only RBF platform in the country with an NBFC licence.

The backers of the alternative funding platform are excited with the huge untapped opportunity across India. Venkatesh Peddi explains. “The market size for RBF across India and Southeast Asia is about $3-4 billion and is projected to grow to $12-13 billion by 2025," contends the managing director of Chiratae Ventures. In multiple conversations with founders across stages and sectors, Peddi underlines that two things starkly stood out. First, equity/debt financing is vital for the growth and scalability of startups. Second, though equity/debt funding has its own share of advantages, founders are increasingly becoming wary of diluting too much or raising too much because of a slew of reasons like high cost of capital, loss of control, qualification barriers, long closure timelines and fixed payment schedules irrespective of the performance.

Given the context, revenue-based financing is fast emerging as a popular choice. It finds the middle ground between bank loans and VC funding for fast-growing small businesses who are not ready to divest shares or put a personal asset up as collateral. The business model bases its repayment plan off a business’ future revenues, without the need for warrants or personal guarantees. Additionally, there are a large number of companies that may not be well suited to raise venture/PE capital, but are eligible for RBF since they are revenue generating companies. Rough estimates, Peddi claims, show that there are over 9.5 lakh digitally-enabled SMEs, majority of them operate in Tier II or III cities, and RBF can be a prime source of financing for them.

Vasa, for his part, reckons that GetVantage is democratising access to working capital for underserved businesses, especially beyond the metros. “We are reshaping the landscape of venture finance in favour of the founders," he says, adding that for early and growth-stage founders, easier access to capital is a game changer. “The team at GetVantage is executing further on our singular vision of Bharat Capital," he says. Amit Srivastava is co-founder of GetVantage.

Though touted as a game changer for founders, does RBF has its share of challenges? Take, for example, what happens if a company sees a sudden dip in revenue or the business gets into the doldrums due to unforeseen factors and variables? Will it not lead to rise in default rates? Globally, the RBF model was the flavour of the season during the peak of the credit cycle in 2020 and 2021, and was lapped up by SaaS and ecommerce players, which have more predictability about their revenues. But as the funding cycle dries, can unsecured credit manage to stay afloat?

Vasa acknowledges the challenges. “Like every financing business, there are, of course, risks involved," he says, adding that he has a plan in place to mitigate risks. “Data and live monitoring are the new collaterals," he says, claiming that the portfolio has a loss rate of 0.7 percent. The tech and platform innovation, he claims, allows real-time monitoring of the business through the tenure, allowing for active course correction and substantially curtailing risk and NPA percentages compared to traditional lenders. Though GetVantage started with RBF, over the last few quarters, it has diversified its offering to introduce new non-dilutive capital solutions such as working capital demand loans, marketing capital, fixed-term loans, and revolving credit lines. These products, Vasa underlines, have been introduced to meet the rapidly evolving needs of thousands of emerging small businesses across India, many of which are originating from outside the metros. While there will always be cycles of growth and slowdowns, the need for working capital is only increasing in markets like India. “Our proprietary research indicates there is a current working capital requirement of over $200 billion for emerging businesses and this is expected to double over the next five years," he says, sounding bullish on his financing model.

Meanwhile, back in Raipur, Saheb reckons that RBF is set to find more takers across Bharat. Reason: Actor Gulshan Grover and the quirky new advertisement which pitches RBF as a ‘no-nonsense, no drama and a simplified funding’ option. During the second season of Shark Tank India, aired in January, GetVantage rolled out a TV commercial and social media campaign with Bollywood’s ‘badman’ Grover. “Kaunsa VC fund advertise karta hai (which VC fund advertises)?" he asks, adding that GetVantage is democratising funding. “Agar paisa kamaogey to paisey milega. No questions asked (If you have revenue, then you will get funding)," he smiles.