How metals are forging a recovery

Global macro headwinds and lacklustre demand will put a lid on prices this year. But can China reset the cycle?

By Neha Bothra

Last Updated: Apr 28, 2023, 12:38 IST8 min

In an interaction with equity analysts in early April, the management of a leading global metal behemoth, with consolidated revenue to the tune of $28 billion, said it planned to reduce its capital expenditure by a staggering 43 percent over the next four years as it sought to conserve cash flows to mitigate the impact of economic slowdown and weak demand in North America and Europe.

The company, Hindalco Industries, India’s largest fully integrated aluminium player, cautioned in a presentation to investors, “Macro headwinds muting near-term performance." The operating metrics underline the pain in its US-subsidiary, Novelis, which contributes roughly 60 percent to the total revenue.

The KM Birla-owned company expects challenges from volatile energy costs, inflation, and interest rates to persist into FY24. However, it has indicated, as guidance, an adjusted Ebitda per tonne of $525 in Q4FY24 [versus $376 in Q3FY23] “when headwinds subside" and profit margins normalise.

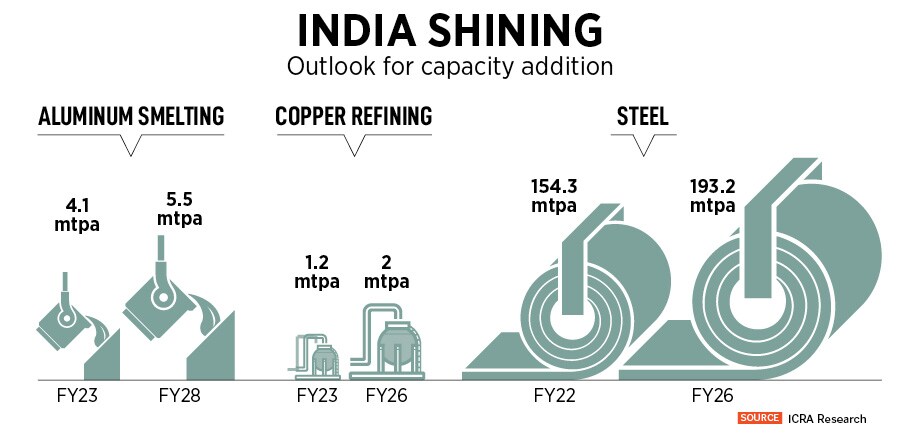

Last year, days after Russia’s invasion of Ukraine in February, aluminium prices hit a record high of $5,000 per tonne stoked by fears of supply constraints and a huge market opportunity opening up due to the growth of electric vehicles (EVs). In the next five-six years, over a million four-wheeler EVs and 13 million two-wheeler EVs are likely to be sold in India per year, according to a report by Motilal Oswal Financial Services.

Against this backdrop, Hindalco bet on the rising global demand for aluminium as it earmarked around $8 billion for expansion over five years, of which $4.7 billion was to be deployed into Novelis and $3.2 billion for domestic operations. But a year later, it cut its capex outlay to approximately $3.3 billion and $1.1 billion respectively to protect the bottom-line.

“Aluminium demand remains weak keeping the market balance in surplus [which] has led to a significant rise in inventory levels, currently at a 20-month high. We forecast aluminum prices to remain range-bound and find risk-reward unfavorable for aluminum producers," says Jatin Damania, research analyst, Kotak Securities.

If the pandemic was a black swan event, the synchronised pace of interest rate hikes by global central banks was unprecedented. Since March 2022, the US Federal Reserve lifted rates by 475 basis points to tackle record-high levels of sticky inflation. Similarly, the Reserve Bank of India increased the benchmark repo rate by 250 basis points to 6.5 percent in FY23 to rein in inflation within its upper tolerance band of 6 percent.

Besides, in a double whammy, China’s Zero Covid policy led to massive supply chain disruptions that were further compounded by the war in Ukraine and higher energy costs. These factors heavily weighed on growth and subsequently the profitability of metal companies. Collectively, the prices gave way to mounting cost pressures and waning demand as investments were put on hold in face of flailing consumption patterns and rising uncertainty.

During the previous super cycle of 2004-2007, the global economy had a compound annual growth rate (CAGR) of 5 percent. But the post-pandemic recovery of the world economy has been shallow and uneven: The IMF slashed its global growth forecast from 6 percent in 2021 to 2.8 percent in 2023 and 3 percent in 2024. In fact, advanced economies are likely to see a pronounced economic slowdown with flattish growth of 1.3 percent in the current calendar year.

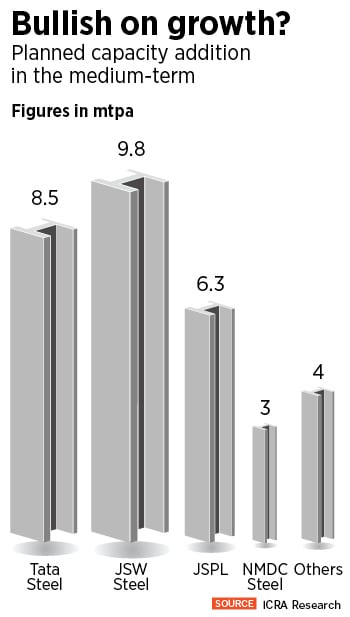

Jayanta Roy, senior vice-president and group head, corporate sector ratings, ICRA says, “The near-term growth opportunities in the overseas markets look challenging as, barring possibly China, most of the other leading steel-consuming hubs are likely to witness anaemic growth in steel consumption in CY23. Therefore, India’s finished steel exports, after an estimated 51.5 percent steep decline in FY23, are expected to witness only a modest growth of 3-4 percent y-o-y in FY24 due to muted external demand."

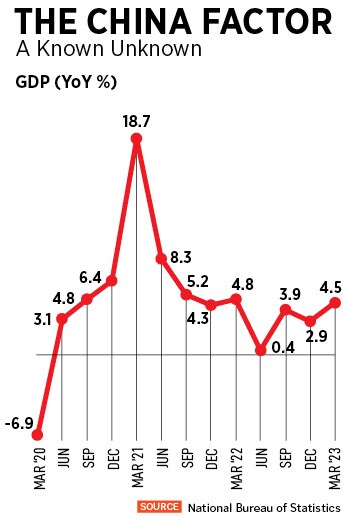

While companies are betting on domestic demand to tide through global challenges, there is a fair degree of uncertainty on how the Chinese economy will perform in the coming months. It is tough to predict with what force the economy will bounce back after it reopened this year.

“International steel prices reached a nine-month high in the second week of March 2023 as easing of Chinese lockdown restrictions led to a pick-up in economic activity for the world’s largest producing and consuming nation," ICRA’s Roy points out.

Moreover, China beat analyst forecasts as its economy grew by 4.5 percent in y-o-y versus 2.9Epercent in the December quarter. Bank of America’s Greater China Chief Economist Helen Qiao notes, “We raise our China GDP growth forecast to 6.3 percent in 2023 versus 5.5 percent previously and consensus at 5.3 percent. Besides the ongoing consumption rebound, we expect the growth driver to further expand into investment. We believe the strong credit impulse in Q1 will lift cyclical growth momentum in the next 1-2 quarters."

Moreover, China beat analyst forecasts as its economy grew by 4.5 percent in y-o-y versus 2.9Epercent in the December quarter. Bank of America’s Greater China Chief Economist Helen Qiao notes, “We raise our China GDP growth forecast to 6.3 percent in 2023 versus 5.5 percent previously and consensus at 5.3 percent. Besides the ongoing consumption rebound, we expect the growth driver to further expand into investment. We believe the strong credit impulse in Q1 will lift cyclical growth momentum in the next 1-2 quarters."

Importantly, core economic indicators were a mixed bag. While services rose to 5.4 percent year-on-year in the March quarter from 2.3 percent in the previous quarter, industrial and construction activity marginally edged down to 3.3 percent from 3.4 percent. It remains to be seen if the pent-up demand can be sustainable in the coming months.

“The pace of consumption recovery could slow down sequentially given the pent-up demand will gradually fade out and inflation stays sluggish. On the other hand, investment momentum may pick up in coming quarters, with the robust credit growth spurring capex in 2Q-3Q," Qiao adds.

The rise of the dragon also clouds the outlook for crude oil.

“Strong economic data in China will provide further cues to the oil prices. A strong data set pushes oil prices on the higher side, likely helping it scale the $90/bbl. level," say analysts at Emkay Wealth.

Moreover, many economists are sceptical of China’s might in the commodities segment over the long-term. “Whenever we have had any commodity super cycle it is always a case of the China factor because of its expansion but now I don’t think China will ever be able to grow at 10 percent rate for five continuous years. They have possibly passed the prime and will probably be growing at 5-8 percent," says Sabnavis.

***

With multiple moving parts and uncertainties, the balance is tilted towards risks that can possibly rub the sheen off metals in the coming quarters.

“It will be a reasonable assumption that after this year passes, we can say it has bottomed out. I would say we have to wait and watch because we are not quite sure of a soft landing or a hard landing and how this year will turn out to be," Sabnavis says. At best, prices are likely to remain flattish and range-bound in the near-term but the long-term trajectory of metal prices looks upbeat given the underlying growth potential of the domestic economy.

First Published: Apr 28, 2023, 12:38

Subscribe Now But, two years ago, when the world was inching back to normalcy after the outbreak of the deadly coronavirus pandemic, the shining performance of commodities, particularly industrial metals, built expectations of an upcoming super cycle as was last seen during the four-year period between 2004 and 2007. At least, that’s what the price trend indicated.

But, two years ago, when the world was inching back to normalcy after the outbreak of the deadly coronavirus pandemic, the shining performance of commodities, particularly industrial metals, built expectations of an upcoming super cycle as was last seen during the four-year period between 2004 and 2007. At least, that’s what the price trend indicated.  Despite the global slowdown, the Indian economy is the fastest growing major economy in the world. Most estimates peg India’s GDP growth around 6.5 percent in the current financial year. Many economists argue that a possible recession in western economies could lower the growth rate to around 5.5 percent.

Despite the global slowdown, the Indian economy is the fastest growing major economy in the world. Most estimates peg India’s GDP growth around 6.5 percent in the current financial year. Many economists argue that a possible recession in western economies could lower the growth rate to around 5.5 percent.