His decision to quit might seem odd to some it was almost decoupled from the bank he was leaving. Kotak Mahindra Bank—like most other lending institutions in India—has been seeing steadily improving profit ratios, a stronger balance sheet and years of a focussed leadership and processes. Pushkar (name changed) is clear that HDFC Bank offers “access to data and products" like no other, but also says if he had stayed on at KMB he would have acquired a similar salary package once he hit a particular grade and slab level.

With no regrets about quitting, he’s followed the adage of ‘People don’t quit bad companies, they leave bad bosses’. After all, the pressures of managing key clients and teams, scaling retail banking, cross-selling and acquiring customers is almost similar across the BFSI (banking, financial services and insurance) sector.

Controlling the attrition rate and retaining the skilled workforce often counts as one of the biggest challenges bankers face in India, particularly post the pandemic, where young employees—millennials and applicable Gen Z—believe that professions and jobs need to be flexible. Most of these would also give priority to maintaining a better work-life balance over career success.

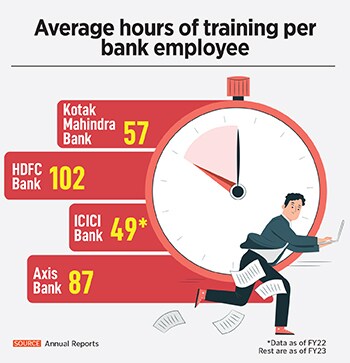

The increased global economic uncertainty has also meant that a majority of the workforce in India remains active job-seekers. And this is despite every bank having organised training and skilling programmes (see details), employee engagement and feedback programmes and incentives for junior level employees to work from the company headquarters.

![]() Add to this the fact that several private and public sector banks and small finance banks are in different stages of expansion, which would mean that they will face a tricky issue of continuing to hire human capital while trying to retain existing skilled staff.

Add to this the fact that several private and public sector banks and small finance banks are in different stages of expansion, which would mean that they will face a tricky issue of continuing to hire human capital while trying to retain existing skilled staff.

In 2022, the Reserve Bank of India (RBI) highlighted that high attrition and employee turnover pose “significant operational risks", including disruption in customer services and all ethical issues for banks. Attrition and high employee turnover lead to loss of institutional knowledge and increase recruitment costs, RBI’s then deputy governor M K Jain said.

Frontline staff attrition alarming

“Attrition should be categorised into three baskets—freshers (frontliners/management trainees), middle management (age 30-45) and top/senior management (age 50+). For the top/senior management, the salary might not be the sole criterion attrition for the industry is often in low single digits. For the middle management, factors such as recognition and better remuneration prospects are critical while for freshers it could be a range of factors," says Santosh Borkar, general manager at NKGSB Co-operative Bank, which has 104 branches spread across five states of Maharashtra, Gujarat, Madhya Pradesh, Karnataka and Goa.

Frontline branch banking and sales, whose job is to retain and acquire customers and portfolios, is the segment that sees the highest churn amongst all banks and NBFCs. The trends in BFSI indicate that post the pandemic, employee turnover has remained high.

“The frontline staff in most banks faces the pressures of having to cross-sell products aggressively. High attrition is not linked to the employer, it is seen in freshers and middle-management seeking hike in CTC and recognition respectively," Borkar told Forbes India.

Rajkamal Vempati, president & head (human resources) at Axis Bank says: “Our experience shows that 60 to 70 percent of the talent moves within the banking ecosystem, another 20 percent moves towards other industries and just five percent leaves for personal reasons."

She says there has been no heightened activity towards fintechs, particularly since funding towards them has slowed, several have scaled down and business models have pivoted.

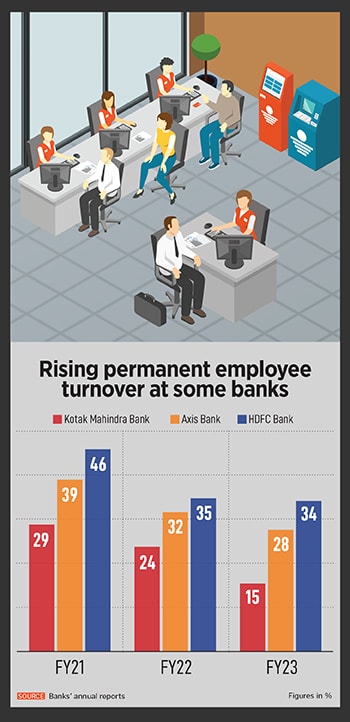

KMB has reported an employee turnover rate of 45.9 percent in the 12 months to March 2023, according to its FY23 annual report. This has only been rising since FY21 (see chart). KMB had a total workforce of 73,481 employees, which included 26 percent women, its FY23 annual report says.

HDFC Bank, the largest private sector lender by assets, faces a similar concern. In a media interaction after announcing its FY24 June-ended quarter earnings on July 18, the bank’s chief financial officer Srinivasan Vaidyanathan disclosed the bank’s average attrition rate at 30 percent.

“There are 13 levels under the CEO. The [attrition rate at] entry level is very high in the high 40-50 percent. [In] the next four levels above entry level, the attrition rate is in mid 20s-30s. We need to work on that. At the core ‘heart of the bank’, the attrition rate is in mid-single digits," HDFC Bank’s Vaidyanathan told media.

![]() HDFC Bank’s CEO Sashidhar Jagdishan in the FY23 annual report says, “The [HDFC] Bank has experienced an increase in attrition over the last financial year, a significant part of which was in the ‘non-supervisory staff’ levels (which includes Sales Officers). One reason that can be attributed towards this increase is a post-Covid phenomenon that may have prompted the younger workforce to recalibrate what they ‘want from their lives’. This has led to increased attrition across all sectors. It is a reality that all major employers are grappling with, especially in the BFSI sector."

HDFC Bank’s CEO Sashidhar Jagdishan in the FY23 annual report says, “The [HDFC] Bank has experienced an increase in attrition over the last financial year, a significant part of which was in the ‘non-supervisory staff’ levels (which includes Sales Officers). One reason that can be attributed towards this increase is a post-Covid phenomenon that may have prompted the younger workforce to recalibrate what they ‘want from their lives’. This has led to increased attrition across all sectors. It is a reality that all major employers are grappling with, especially in the BFSI sector."

HDFC Bank, which has now merged with housing finance subsidiary HDFC, effective July 1, is now seen to be better placed to improve interest income, but the focus will be on the pace of growth to garner deposits, to boost its lending capacity further. HDFC Bank had a total workforce of 173,222 people as on March-end 2023.

Axis Bank, one of the few private sector banks to have seen a rapid financial turnaround towards strong profitability in recent years, under the leadership of CEO Amitabh Chaudhry, has also not escaped the attrition bug. “Its staff attrition increased to 34.8 percent in FY2023 from 31.6 percent in FY2022," independent banking analyst Hemindra Hazari said, quoting from the bank’s FY23 annual report. The FY23 attrition rate is the second highest percentage since FY20 (of 36.6 percent), Hazari says.

Dhiren Bhanushali, who had worked with Axis Bank’s personal banking Burgundy team in 2017 offering wealth management and investment solutions to high-income individuals, quit the bank not due to any ‘push’ factor within the bank. “For me there was a pull factor, because my then regional cluster head offered me an elevated package to join IDFC First Bank, I moved." Bhanushali (name changed) worked at IDFC for a year and a half before joining ICICI Bank.

ICICI Bank, which had a total workforce of 103,010 as per its FY22 annual report, also faces the same issue of high attrition. Media reports in 2021 indicated the bank faced an overall attrition of 20 percent then, but no updated figure has been disclosed in its annual report.

In the co-operative banking segment, attrition usually stays within the co-operative banking ecosystem (for example people would move from Saraswat to SVC or Cosmos Co-operative banks or conversely etc.). Attrition in cooperative banks for freshers is just around 2-3 percent, while for the middle- and top management it is very low, Borkar says. Small might be beautiful for co-operatives, but it comes with its own disadvantages in terms of lower salary packages and incentives and growth opportunities.

Will training build trust?

An AON study on attrition in the BFSI sector, done for The Economic Times, for the nine months to December 2022 was pegged at 25 percent for the entire sector and 26.4 percent for the wealth segment. It was lower for AMCs at 16 percent.

An HR advisor working with a wealth management firm says, “Wealth packages are heftier than those on the branch banking side. Their packages not only include trail commissions but they could earn an average of Rs 15-20 lakh of incentives each year (linked to performance) while for banks it is much lower at Rs 3-4 lakh per year."

She adds, “A change in the business approach or the model or leadership changes are drivers for people leaving existing positions. If they feel their identity as a wealth manager is getting diluted or they are being made to sell products outside the boundaries they should be doing or if the company is not able to define its growth strategy or decide on which products would work for their clients at the right time, then employees start to look for stable and stronger platforms."

Amongst the private sector banks, IDFC First Bank has an overall rating of 4 (with a 70 percent recommendation to a friend) on workplace review platform Glassdoor. This was followed by Axis Bank (3.8 / 70 percent), ICICI Bank (3.7 / 68 percent), Kotak Mahindra Bank (3.7 / 67 percent) and HDFC Bank (3.5 / 58 percent).

HDFC Bank’s Vaidyanathan said: “We are recruiting people, encouraging them into the financial services system, better training to retain them. We are working on more training programmes for the employees. It is a work in process."

Rajiv Anand, deputy managing director, Axis Bank, is clear about the direction the bank will continue to take in coming years. “The fact that we have become a meritocratic, performance-oriented organisation is a reality. We are working towards becoming a bigger bank, and our ambitions are also growing. Amitabh [Chaudhry] has been able to reset ambitions in the organisation, which is converting into deliveries. [The bank"s RoE has risen to 18.84 percent in FY23 from 8.58 percent in FY19]."

“The runway for growth is very long but it will not be delivered on a platter for any of us. Each one of us will have to push ourselves to be able to deliver to the expectations of our customers, boards, regulators and other stakeholders. We want to run a consistent and predictable ‘no surprises’ business and that is what we are working towards," Anand told Forbes India.

It is not correct to pinpoint any one bank for failing to control attrition. Though every bank is involved in training and skilling the staff on enrolment, these are not the people driving the business. Experts do point out that banks should be more worried about losing people in the middle management and top management level. “In a normal environment we will expect attrition to remain in control. The sector will be able to attract the right talent and attrition should normalise in coming years," says Nitin Agarwal, banking analyst at Motilal Oswal.

Add to this the fact that several private and public sector banks and small finance banks are in different stages of expansion, which would mean that they will face a tricky issue of continuing to hire human capital while trying to retain existing skilled staff.

Add to this the fact that several private and public sector banks and small finance banks are in different stages of expansion, which would mean that they will face a tricky issue of continuing to hire human capital while trying to retain existing skilled staff. HDFC Bank’s CEO Sashidhar Jagdishan in the FY23 annual report says, “The [HDFC] Bank has experienced an increase in attrition over the last financial year, a significant part of which was in the ‘non-supervisory staff’ levels (which includes Sales Officers). One reason that can be attributed towards this increase is a post-Covid phenomenon that may have prompted the younger workforce to recalibrate what they ‘want from their lives’. This has led to increased attrition across all sectors. It is a reality that all major employers are grappling with, especially in the BFSI sector."

HDFC Bank’s CEO Sashidhar Jagdishan in the FY23 annual report says, “The [HDFC] Bank has experienced an increase in attrition over the last financial year, a significant part of which was in the ‘non-supervisory staff’ levels (which includes Sales Officers). One reason that can be attributed towards this increase is a post-Covid phenomenon that may have prompted the younger workforce to recalibrate what they ‘want from their lives’. This has led to increased attrition across all sectors. It is a reality that all major employers are grappling with, especially in the BFSI sector."