The anomaly of doing whatever it takes to revive growth

The RBI needs to focus on its mandate of inflation control, and the onus is on the government to do the bulk of the lift off to drive investments and growth as the economy grapples with multiple chall

Monetary policy needs to be normalised quickly as any delay risks even bigger rate hikes down the road and more policy uncertainty, which could be painful Illustration: Chaitanya Dinesh Surpur

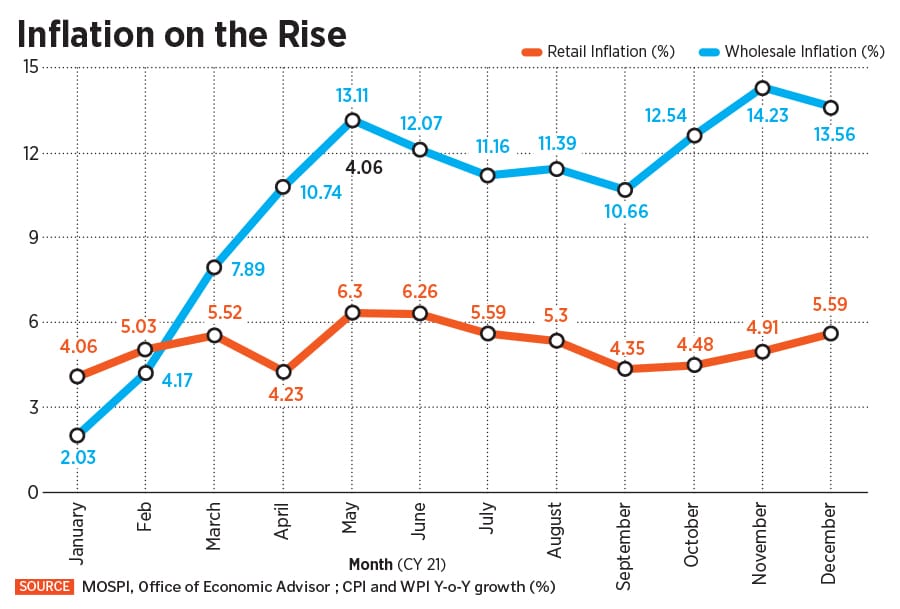

Unprecedented times call for unprecedented measures that come with untold risks. The Reserve Bank of India (RBI), like central banks worldwide, made this leap of faith as it scrambled to respond to the once-in-a-lifetime pandemic by reducing interest rates and injecting excess liquidity to cushion the economy from acute disruptions. Nearly two years later, there is a new mutation of the coronavirus inflation is disturbingly high (see chart) but economic growth is anaemic the repo rate is at an all-time low of 4 percent but consumption and investment demand are in low gear industrial production is bleak but stock markets are cheerful.

Against this backdrop, despite growing inflationary challenges, the RBI has said it will remain committed to continue its accommodative stance until there are signs of durable growth in the economy. In other words, the central bank prefers a status-quo till the time there is a clear uptick in the investment cycle.

Pranjul Bhandari, chief India economist at HSBC, argues that the pace of acceleration in investments in the economy depends on a high degree of policy certainty around macroeconomic stability. "Perhaps the RBI now needs to think differently and focus on its mandate of inflation control. That in itself adds a layer of policy stability that will drive investments over time, rather than the other way around—where it will not normalise monetary policy until investment rises," she adds.

The RBI cannot afford to focus just on growth, says Upasna Bhardwaj, senior economist, Kotak Mahindra Bank. “We need to ensure we don"t get into an inflationary environment which can choke growth," she cautions. In fact, hovering above 5 percent during the pandemic period, core inflation has been elevated long before rising global inflation rung alarm bells.

Bhandari worries inflation could be far more entrenched once food prices start rising. She says, “Monetary policy needs to be normalised quickly as any delay risks even bigger rate hikes down the road and more policy uncertainty, which could be painful."

High inflation and low growth

Economists say there are challenges to growth and inflation. "Inflation is on the rise and growth is uneven and lopsided," says Bhardwaj.

On the one hand, inflation expectations have strikingly gone up over the past two years. Nomura expects inflation to surprise on the upside and average around 6.4 percent in the first quarter of CY22 and 5.9 percent in CY22. "The third wave comes amid rising oil prices and a significant build-up of input cost pressures which will likely accentuate price pressures," notes Sonal Varma, MD and chief economist, Nomura.

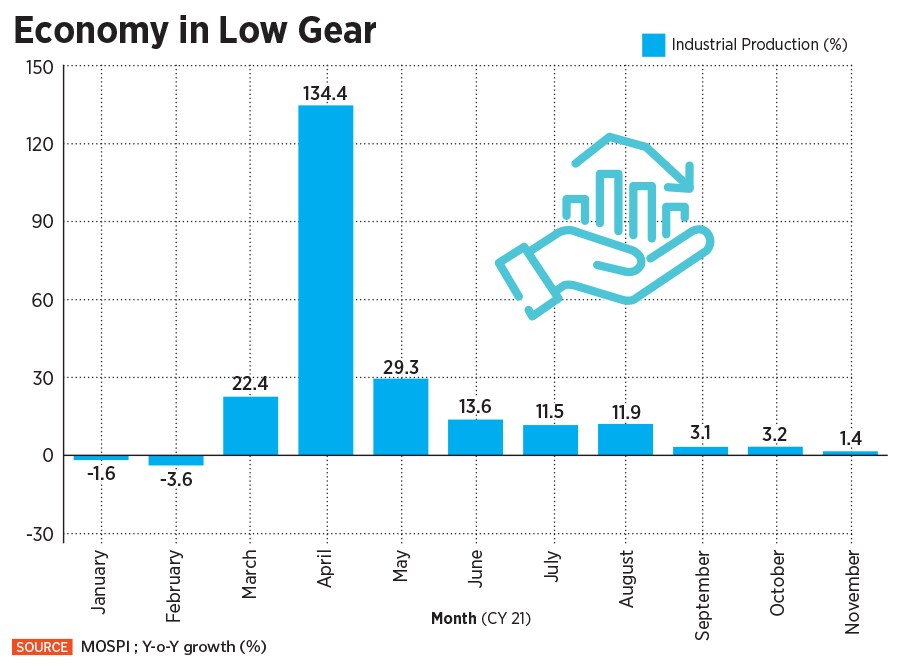

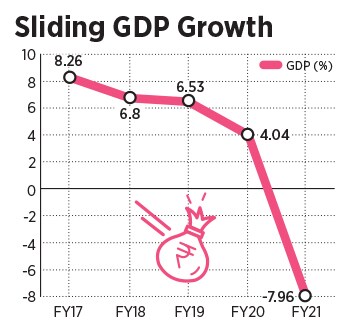

On the other hand, Bhardwaj says, the quality of growth has deteriorated and a double-digit real GDP growth next fiscal is difficult. Industrial production has steadily declined over the past several months (see chart) and reflects weak economic activity. Industrial output grew by 1.4 percent in November versus 3.2 percent in October and 11.9 percent in August.

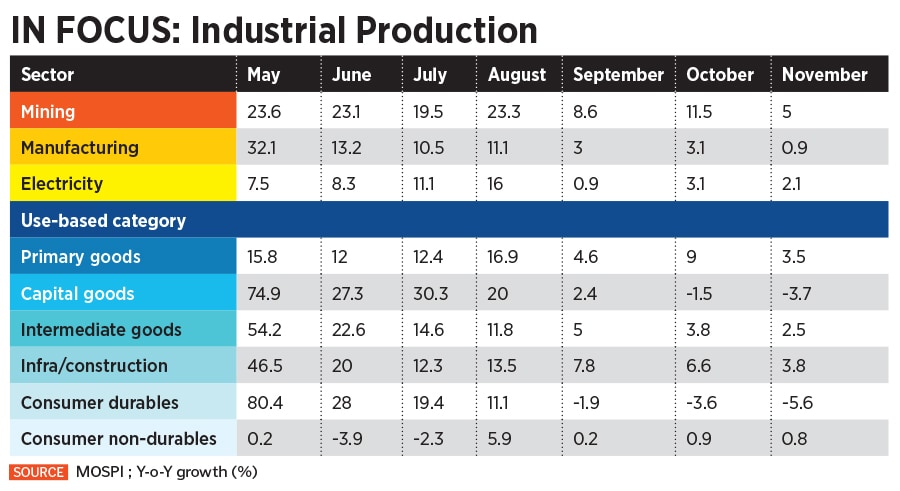

The manufacturing sector along with the categories of capital goods and consumer durables have been most sharply hurt (see chart). “Capital goods and consumer durables contracted (by 3.7 percent and 5.6 percent respectively) in November even on a low base, suggesting that the sentiment towards big ticket consumption as well as investment activity remains fragile," says ICRA’s chief economist Aditi Nayar.

With continued supply disruptions and constraints in availability of key raw materials like coal and semiconductor chips, the outlook for industrial production does not look bright in the coming months.

Moreover, a recovery in the capital goods category is unlikely if firms are hesitant to invest. Bhardwaj adds, "Capacity utilisation needs to pick up significantly to revive the private investment cycle, and for that to happen we need a strong and visible demand-side story."

The lack of strong consumer and business confidence underscores the state of the economy. "People need to start expecting that growth is going to go up," says Bhandari. She expects GDP in FY23 to be lower than Street estimates due to the uncertainty around revival of investments after pent-up demand cools off.

The investment logjam

After the third wave of Covid-19 ebbs, Bhandari expects much of the growth momentum to be led by strong pent-up demand for goods, services and housing. “But pent-up demand can only go so far and perhaps not be enough to raise capacity utilisation to levels that incentivise new investment," she adds.

After rising rapidly, goods production has indeed plateaued at about pre-pandemic levels. There is hope that services demand does better, but both goods and services demand are driven by incomes, elaborates Bhandari. “We will start to see growth slowdown in the second half of FY23 once pent-up demand has run its course and we realise we don"t have a new growth driver," she says.

When pent-up demand fizzles out, economists hope that the multiplier effect of investment will play out and boost the growth momentum. But since capacity utilisation is at low levels, it puts a lid on growth expectations. Unless consumer demand and business confidence sustain, the investment cycle cannot kickstart substantially. This is the big hurdle for policymakers to navigate.

While the twin balance sheet problem has considerably eased, the lack of clear policy direction and heightened macro risks have roiled sentiment, underlining the need for measures that secure the long-term objectives of macroeconomic stability.

Stability amidst volatility

At the heart of much of the prevailing economic pain is the deep-rooted issue of tepid consumption and demand, which have been largely stoked by the uncertainties surrounding the pandemic. Consumption is below pre-pandemic levels, and the lack of confidence on how the economic situation will pan out has hindered investment across sectors, while widening the gap between the haves and have-nots.

"The onus lies on the government to do the bulk of the lift off through clear prioritisation, and a very focussed sector-wise approach in terms of policy support," says Bhardwaj.

Economists and analysts Forbes India interacted with stress on the need for the government to implement targeted fiscal measures and policy reforms to address the ailing sectors of the economy. They also call for continuation of social welfare schemes that focus on education and migrant labourers working in cities. There is a need to boost employment to get the economy back on the high growth track.

Mark Matthews, managing director and head of Asia research at Julius Baer, says infrastructure and industry are the two sectors where the greatest fiscal attention will be paid. “Infrastructure would help create a ‘buzz’ in the investment cycle. We know the prime minister has been meeting industry leaders and there is a drive to revive manufacturing. Housing is another sector that should benefit, for social reasons", he says.

Bhandari feels Budget 2022 should continue the policy reforms articulated in the previous budget to ensure there is "stability and predictability at a time of global volatility". The government must fast track the pace of asset monetisation and divest stake in PSUs to narrow the fiscal deficit. To this end, it is imperative that the government articulates a credible five-year glide path for fiscal consolidation. The high level of government borrowing must not come in the way of monetary policy tightening.

Monetary policy needs to be normalised quickly as any delay risks even bigger rate hikes down the road and more policy uncertainty, which could be painful

Monetary policy needs to be normalised quickly as any delay risks even bigger rate hikes down the road and more policy uncertainty, which could be painful

After rising rapidly, goods production has indeed plateaued at about pre-pandemic levels. There is hope that services demand does better, but both goods and services demand are driven by incomes, elaborates Bhandari. “We will start to see growth slowdown in the second half of FY23 once pent-up demand has run its course and we realise we don"t have a new growth driver," she says.

After rising rapidly, goods production has indeed plateaued at about pre-pandemic levels. There is hope that services demand does better, but both goods and services demand are driven by incomes, elaborates Bhandari. “We will start to see growth slowdown in the second half of FY23 once pent-up demand has run its course and we realise we don"t have a new growth driver," she says.

Economists and analysts Forbes India interacted with stress on the need for the government to implement targeted fiscal measures and policy reforms to address the ailing sectors of the economy. They also call for continuation of

Economists and analysts Forbes India interacted with stress on the need for the government to implement targeted fiscal measures and policy reforms to address the ailing sectors of the economy. They also call for continuation of